Fed to Discuss When to Pause Gradual Hikes: Decision Day Guide

Fed to Discuss When to Pause Gradual Hikes: Decision Day Guide

(Bloomberg) -- Federal Reserve Chairman Jerome Powell has signaled the U.S. central bank could take a break from increasing interest rates at some point. His colleagues are now debating how quickly to consider such a pause.

The Federal Open Market Committee is almost certain to keep rates steady at the close of its two-day meeting Wednesday in Washington, and will reinforce bets on a move in September if it repeats a reference to further gradual rate hikes in the accompanying policy statement.

Pricing in federal funds futures contracts show almost zero expectation for a move at this meeting versus a probability a little above 80 percent in September.

Powell told Congress on July 17 that gradual rate moves were the plan “for now,” which is the kind of qualifier the committee could add to its statement to hint at a future breather in the tightening campaign.

“Given that there’s no visible inflation threat -- not in the data and not in the FOMC forecasts -- it makes sense to inject conditionality on future moves,” said Roberto Perli, a former Fed economist who is a partner at Washington-based consultancy Cornerstone Macro LLC. “So the ‘for now’ language seems appropriate and seems likely to make it into the statement, if not this time, soon.”

The Fed is trying to keep the U.S. economic expansion on track after growth was buoyed by strong consumer spending in the second quarter following tax cuts, and as it closes in on the central bank’s twin goals: Stable prices, which it defines as 2 percent inflation, and maximum employment.

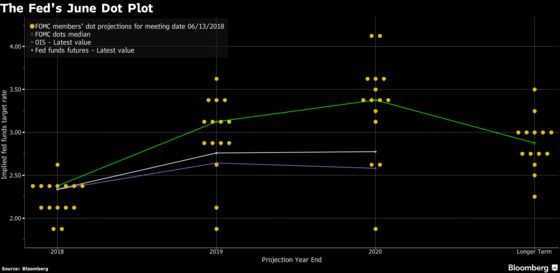

Policy makers are close on inflation after undershooting their target for years, and are arguably already past the level of long-term sustainable full employment, with the jobless rate at 4 percent in June. They’ve raised rates twice this year and have two more moves penciled in for 2018, according to forecasts that officials updated in June.

The FOMC is also considering changing its description of monetary policy from “accommodative” to something closer to neutral, the committee indicated in minutes of its June meeting. But with Powell not scheduled to brief the media on Wednesday, the easiest course would be to keep the statement’s guidance nearly identical to its June meeting.

“I don’t expect any major change in the message because Powell will not be holding a press conference to clarify it,” said Ward McCarthy, Jefferies LLC chief financial economist. “They do seem to be trying to update where they are on the policy normalization path, and that’s going to be a communications challenge.”

Powell’s next scheduled press conference will be after the FOMC meeting on Sept. 26.

What Our Economists SayThe August FOMC meeting will be a relative non-event for market participants. Policy makers will keep interest rates on hold and make minimal changes to the economic assessment to reflect recent developments. The markets broadly anticipate a September rate increase, so Fed officials will not need to materially refine their signaling about the next move.-- Carl Riccadonna and Tim Mahedy, Bloomberg Economics |

The FOMC has pegged a neutral funds rate -- the rate that neither promotes nor holds back growth -- at 2.9 percent, according to their median estimate in June. But there’s considerable uncertainty around that projection, and the Fed’s monetary policy report in July includes estimates that would suggest they’re already very close to that level.

The possibility of a pause reflects a split in the committee’s June forecasts, with eight participants favoring at least two more rate hikes this year, but seven favoring one or none.

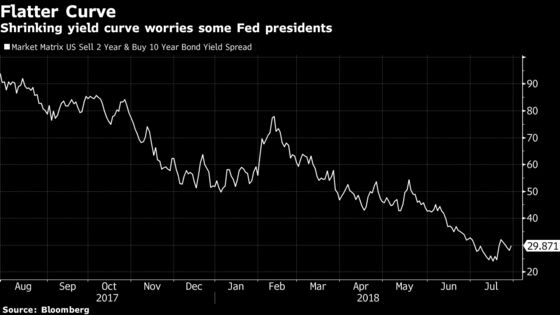

A flattening of the U.S. Treasury yield curve adds urgency to the discussion. Fed presidents James Bullard of St. Louis, Raphael Bostic of Atlanta and Neel Kashkari of Minneapolis have raised concern that being too aggressive on rate hikes could invert the curve.

That happens when yields on short-dated securities rise above long-term ones and an inverted yield curve has preceded every U.S. recession in the last 50 years.

While the FOMC updates its statement each meeting describing conditions, changes might be modest since the June statement was already upbeat, said Lindsey Piegza, chief economist at Stifel Nicolaus & Co.

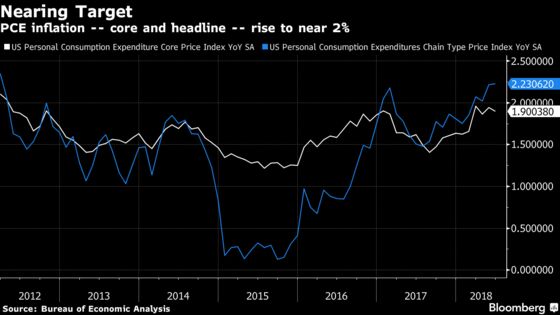

While inflation by the Fed’s preferred measure was 2.2 percent in June -- with core inflation, excluding food and energy, at 1.9 percent -- the FOMC is likely to be somewhat concerned.

Related Bloomberg Economics Analysis: FOMC to Tread Lightly Ahead of September Hike

“As inflation has fallen short of 2 percent for more than six years, inflation can also be allowed to run above the Fed’s objective for a number of years and is expected to do so by at least a number of Fed members,” Piegza said.

There will be a shift among voters this meeting. The San Francisco Fed is looking for a new president after former chief John Williams relocated in June to run the New York branch. As a result, Kansas City’s Esther George will cast San Francisco’s FOMC vote until a new leader has been installed, though interim president Mark Gould will attend the meeting and speak on its behalf.

George, one of the most hawkish FOMC participants, recently endorsed continued gradual rate hikes, while saying an inverted yield curve may not necessarily be an economic signal.

To contact the reporter on this story: Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Jeff Kearns

©2018 Bloomberg L.P.