IMF Gives Downbeat View of Greek Economy at End of Bailout Era

Fund says banks may need up to 1.9 billion euros extra capital

(Bloomberg) -- The International Monetary Fund gave a glum assessment of Greece’s prospects, weeks before the country embarks on life outside the bailout programs that have dominated public life for the last eight years.

While commending the Greek government for eliminating the fiscal and current account imbalances and restoring growth, the Washington-based lender said “risks are tilted to the downside.” The country’s banks could need more capital, and some of the IMF directors questioned the long-term sustainability of Greece’s public debt and the realism of budget and growth projections, according to the fund.

The report damps the celebratory tone from some Greek and European officials as the country prepares to exit its bailout program next month after receiving more than 300 billion euros ($352 billion) in loan commitments from the euro area and IMF since 2010. While economic reforms linked to those programs have transformed the country, a quarter of the economy was wiped out in this period as unemployment soared and incomes were slashed.

“Crisis legacies and an unfinished policy reform agenda in most areas weigh on Greece’s prospects,” the IMF said in its annual so-called Article IV consultation report. “High public debt, weak bank balance sheets, reliance on capital controls and emergency liquidity assistance, and worrisome social indicators, including still-high unemployment, all weigh on growth and social cohesion.

The euro pared earlier gains following release of the report, trading little changed at $1.1705 at 5:04 p.m. Athens time, having earlier risen to $1.1746. Greek government bonds fell, with the yield on the 10-year benchmark rising 10 basis points to 3.97 percent.

The IMF ultimately refused to participate in the country’s third and last bailout program, agreed to with euro-area member states in 2015, due to lingering concerns about the country’s debt sustainability.

In June, euro-area finance ministers gave the green light to a package a measures to lighten Greece’s debt load -- the highest in the euro-area as a proportion of gross domestic product at about 180 percent. While these can facilitate market access in the medium term, it could be difficult to sustain this access in the long run without further debt relief, according to the fund.

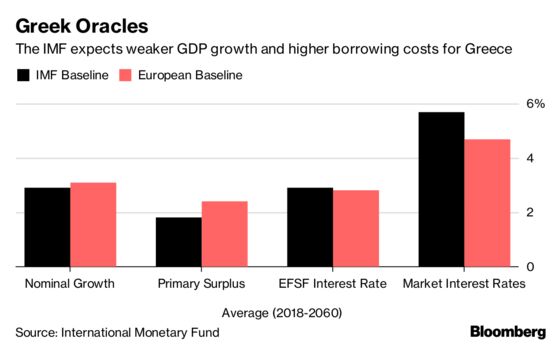

Differing underlying assumptions about the fiscal and economic prospects lie behind diverging views of the IMF and the European Commission about Greece’s debt sustainability. Whereas the Commission sees debt falling to 96.8 percent by 2060, the fund sees the debt-to-GDP ratio rising again from around 2038.

“Permanently raising growth would require a period of reform implementation that exceeds in both ambition and duration what Greece has achieved so far,” the IMF said.

In particular, the fund raised concerns at the government’s intention to reverse some labor market reforms adopted in 2011 after the end of the program, and said the balance of fiscal policy also needs to be adjusted away from taxes to support growth. Long-run trends in productivity and demographics are also poor, according to the IMF.

Bank Capital

The IMF also flagged concerns about the country’s banks, saying they should raise additional capital. While the stress test results published by the European Central Bank in May pointed to the banks’ resilience in the baseline scenario, if core capital ratios in the test’s adverse scenario had to be kept between 7.5 percent to 8 percent, the related capital shortfall would be between 1.3 billion and 1.9 billion euros, the IMF said.

The banks’ exposures to bad loans -- the highest in the European Union at almost half of total loans -- has left them with weak balance sheets as credit continues to contract, the IMF said.

The banks need to set more ambitious reduction targets, it said. Lenders so far have been able to meet the ones already agreed to with regulators in large part because those targets are backloaded, according to the fund.

--With assistance from Nikos Chrysoloras, Eleni Chrepa, Christos Ziotis, Viktoria Dendrinou and Sotiris Nikas.

To contact the reporter on this story: Marcus Bensasson in Athens at mbensasson@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Kevin Costelloe, Brian Swint

©2018 Bloomberg L.P.