Economists Have Lost the Trust of Politicians

Economists Have Lost the Trust of Politicians

(Bloomberg Markets) -- Not so long ago, politicians had “favorite” economists. Margaret Thatcher’s was Milton Friedman. John F. Kennedy’s was probably John Kenneth Galbraith. President Bill Clinton had a Nobel Prize-winning economist, Joseph Stiglitz, in residence at the White House for his entire first term and was said to light up at the mention of John Maynard Keynes.

You don’t hear of many favorite economists today. Political leaders still have economists around, but it’s difficult to remember the last time one publicly and proudly followed their advice. Donald Trump, as ever, is the extreme case. He seems to take some pride in doing the exact opposite of what mainstream economists would prescribe—on the wisdom of trade wars, say. But if the economics profession were being honest with itself, it would have to admit that the problem goes deeper than the gleefully heterodox President Trump.

If politicians in the advanced economies aren’t spending much time listening to economic gurus anymore, that’s partly because economists haven’t had very useful solutions to the big problems politicians are being asked to fix. Most failed to predict the global financial crisis, and the core macroeconomic models taught for decades have been coming up short ever since. Economists don’t even have answers to the challenges facing central bankers, which for many today includes getting the inflation rate back to 2 percent.

I saw the failures of traditional economic prescriptions firsthand in 2016 while chairing a commission on inclusive growth sponsored by the 30 largest cities in the U.K. The first public hearing was in the city of Sheffield, in the north of England, just six days after the referendum on the U.K.’s membership in the European Union. Sheffield had been an unemployment black spot throughout the 1980s and 1990s, following the collapse of its steel and coal industries. Local leaders had dedicated themselves to following the modern recipe for economic revival, redeveloping the city center and expanding the universities to give it one of the greatest concentrations of students in the U.K.

On paper, the results were impressive. In 2016, a record-high proportion of the population was employed and the unemployment rate was around 6 percent, less than half its early-1990s level. But public services had been squeezed by fiscal austerity. The poorest parts of the city still suffered from most of the social problems they had when unemployment was three times higher. As one local social worker told us: “The problem usually isn’t finding a job. It’s having to find two or three.”

This is one reason that 80 percent of the wider Sheffield area disregarded the advice of every leading local politician and voted for Brexit. At the commission’s hearing, the city council chief executive, John Mothersole, was still in shock. “For years we’ve gone along with a dominant economic narrative, which said any growth was good growth,” he said. “Now we’re seeing the consequences.”

The dynamics of the Brexit vote were complicated. It wasn’t determined by economics alone. One could say the same about the election of Donald Trump. But one lesson from the populist upsets of the past few years is that it’s not just the quantity of growth and jobs that matters to voters, it’s also the quality.

In the U.S. and the U.K., around half of households classified as living in poverty contain at least one working adult. That’s been a wake-up call for generations of policymakers who were told that the best answer to poverty was creating jobs.

Wages matter a lot. But so, it turns out, do less tangible factors such as job satisfaction, the potential for advancement, self-worth and—most slippery of all—a sense of community. These aren’t well-captured by traditional economic statistics, and until recently economists haven’t had much to say about them. Nor have most economists wanted to get into debates about the distribution of economic and political power—even if these have profound consequences for the broader economy.

Of course, we do have wage data in most economies. But most of the timely data are national. For local policymakers such as Mothersole, it’s almost impossible to know whether rapid employment growth is actually delivering quality jobs in his city.

Immigration exposes another painful divide between standard economic advice and real-life politics. For years economists showed, categorically, the benefits of immigration to the receiving country. Successive U.S. presidents, both Republican and Democrat, stuck to the mantra. So did mainstream politicians in Europe. Large-scale legal immigration was good for the country and the economy, they said. Economists backed them up by finding only isolated cases in which immigrants hurt wages or employment for native workers.

But economists missed something that mattered more than the numbers. Rightly or wrongly, some voters felt that, thanks to immigration, their towns and cities were no longer “theirs,” that it was harder to find a job or a school for their children. Politicians in the U.S. and U.K. who grasped this early have capitalized on that disconnect between the elite and ordinary voters. Economists are left on the sidelines, counting the economic costs of the backlash.

You might say that it doesn’t matter whether economists can explain voters’ complicated feelings about immigration, community, and the rest if those economic gurus can still deliver on the basics. The trouble is, they can’t.

Collectively, the world’s leading central banks did apply classic economic recipes to prevent the world slipping into another Great Depression in 2007-09. It was lucky that the Fed chairman at that time, Ben Bernanke, had literally written the book on 1930s economic policy. But as economists Larry Summers and Olivier Blanchard have pointed out, output per person of working age in the U.S. in the 12 years after 2007 is likely to be no higher than in the 12 years after 1929. In many countries, including the U.K., the cumulative loss of gross domestic product has been significantly higher than in the 1930s.

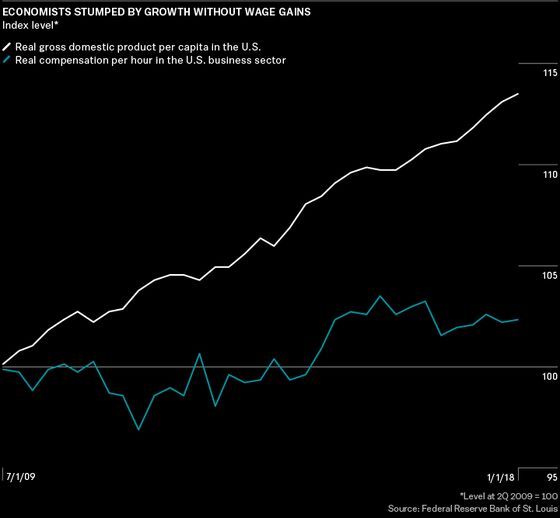

These mighty central bankers have not yet produced a global recovery capable of thriving without a sea of cheap money. Nor have they found a solution to the riddle of low productivity and low wages.

The European Central Bank’s Forum on Central Banking this year in the Portuguese resort of Sintra was devoted to understanding why wage growth and inflation have been so feeble. Over two days the assembled economists and central bankers listened to contributions from some of the finest minds in the profession—culminating in a final panel that featured the heads of the central banks of the U.S., Japan, the euro zone, and Australia. None of these central bankers currently has wage growth in their home economy that is high enough to ensure that they achieve their inflation target for a prolonged period or deliver decent growth in real incomes for the median worker.

In 2009 there were six unemployed workers for every job vacancy in the U.S. Today that ratio is slightly less than 1 to 1. The cautious consensus at Sintra was that it was only a matter of time before wages finally started to respond to a tightening labor market. But no one was willing to make that prediction with any great confidence. Indeed, the experience of Philip Lowe, the governor of Australia’s central bank, suggests that a tighter market could be a long wait. Annual wage growth is barely 2 percent in Australia now, despite 27 years of uninterrupted economic growth.

The Organization for Economic Cooperation and Development confirms this in its latest survey of employment prospects across the advanced economies: Wage growth is “missing in action”—and the wage growth that we’ve seen hasn’t been evenly distributed. Across the OECD’s members, real labor incomes of the top 1 percent of earners have increased much faster than incomes of median full-time workers in recent years.

These are basic facts of modern macroeconomic life that economists cannot hope to tackle without coming to grips with the political and institutional changes that have reduced the bargaining power of workers and tilted the playing field toward capital. The most interesting economists in the world today are doing just that.

Jason Furman and Peter Orszag, two former Obama administration economists, have a theory that reduced competition and dynamism in key sectors have produced both the slowdown in productivity in the U.S. and the rise in income inequality. Richard Baldwin, professor of economics at the Graduate Institute of International and Development Studies in Geneva, has written a cogent account of the latest stage of globalization that describes, in plain English, why governments should stop focusing on footloose companies and capital in their efforts to boost national competitiveness and instead focus on arming people and places to compete.

We’re also hearing mainstream economists talk more loudly about the possibility of shifting the balance back toward labor with wealth taxes and reduced taxes on earned income. That’s a big shift for a profession that seemed to think until recently that reducing the tax on capital was always and everywhere a good thing. It will be interesting to see how long it takes for an elected politician to decide that any of this advice is worth listening to.

Stephanie Flanders is senior executive editor for Bloomberg Economics in London.

To contact the editor responsible for this story: Christine Harper at charper@bloomberg.net

©2018 Bloomberg L.P.