China Slowdown Has Debt Warriors Rethinking Their Targets

Politburo affirms debt campaign to continue at measured pace.

(Bloomberg) -- A slowing economy and a rumbling trade war are giving officials trying to tame China’s debt reason to be more selective about their targets, not to give up completely.

Less than two years into the broad-based drive to contain credit growth, policy makers are now placing more emphasis on curbing debt at state firms and in parts of the property market. Meanwhile, the vise-grip that’s been causing contraction in the shadow banking sector and at local governments is being eased in the hope of preventing a sudden stop in the economy.

While a meeting of the Politburo Tuesday recognized that the external environment -- read Donald Trump’s trade war -- has “significantly changed,” the nation’s top leadership under President Xi Jinping affirmed that the campaign will continue, albeit at a more measured pace. That matches the approach of the government as a whole, which has rolled out targeted policy shifts from tax breaks to bond-market support in recent weeks.

“The radical deleveraging policy is under comprehensive adjustment” and the credit environment is shifting to moderate from tightening, said Wang Yifeng, a researcher at China Minsheng Bank in Beijing. He said the policy stance will be tilted toward controlling debt “more precisely” in the future, which is a delicate and difficult act.

| China’s Trade War Policy Shift So Far... |

|---|

|

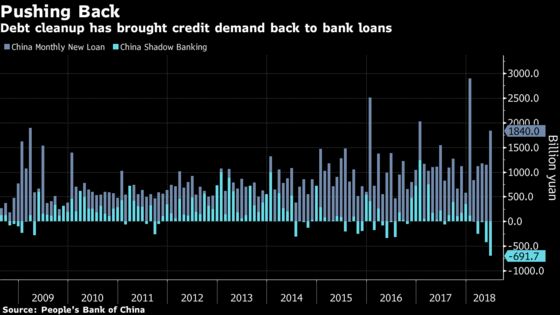

China has declared some successes in its effort to control spiraling debt. Economists see the total debt-to-gross domestic product ratio stabilizing this year, at around 260 percent. That’s a view that officials have echoed. Against that backdrop, policy makers have appeared more concerned about a sharp decline in non-traditional lending cutting off the supply of credit to small businesses -- the areas official banks have been less willing to serve.

The amount of money lent via the shadow-banking sector declined by 691.7 billion yuan in June, the biggest net monthly drop on record, according to Bloomberg calculations based on central bank data.

Amid the slew of announcements of easier policy, officials are maintaining focus on slaying zombie companies and cleaning up their debt. The appointment of Vice Premier Liu He, Xi Jinping’s top economic policy adviser, in July to a role overseeing state-enterprise reform may also be a signal in that regard.

Alongside the roll-out of stimulus policies in July, the State Council, China’s cabinet led by Premier Li Keqiang, re-committed to “resolutely clear out zombie enterprises.”

Shen Ying, an official from the nation’s state-enterprise regulator, said in January that the body has recognized 2,041 centrally-managed state firms as zombie companies or companies with special difficulty, and it is working to dispose of the companies through restructuring, bankruptcy or operational reform.

Elsewhere, an important pillar of the property market in lower-tier cities is coming under renewed scrutiny. In July, the China Development Bank announced that its head office will now review all loans for the redevelopment of shanty towns made by local branches before approval with the aim of avoiding excessive local government debt, according to a report by the Xinhua news agency. The bank has doled out more than 460 billion yuan ($67 billion) in such loans this year, a practice that has helped drive inflated prices in those urban areas.

The politburo meeting on Tuesday also pledged to “firmly curb home price gains,”

underlining resolve to keep the property market stable despite the easing stance.

A renewed focus on financial crime is becoming evident. The Financial Stability and Development Committee -- also headed by Liu He -- has been recently bolstered by the addition of law-enforcement, Ministry of Justice and Communist Party officials tasked with maintaining discipline, in a move that adds even more clout to the oversight panel.

There’s little doubt though that the overall character of the financial risk campaign is softening, at least for now. Regulators have issued softer-than-expected rules on shadow banking, the State Council has called on lenders to meet reasonable credit demand from local financing vehicles, and the People’s Bank of China is systematically easing liquidity conditions.

Old-Style Tactics

That could, for example, mean a rise in debt to finance infrastructure projects, something that recalls China’s old-style approach to growth management.

Xi’s signature supply-side reform that previously stressed cutting excessive capacity and debt will put greater emphasis on infrastructure construction as part of the efforts to repair weak links in the economy, according to the politburo meeting Tuesday.

The stress on infrastructure will lead to a rise in investment in rural development ranging from water and gas supply and sewage construction, Ming Ming, Beijing-based head of fixed income research at Citic Securities Co., wrote in a report. He said railroad and electricity investment may also be resumed.

The shift to a more targeted campaign puts policy makers in charge of managing an even more complex task than simply reducing the nation’s debt pile -- cutting some parts of it while allowing credit elsewhere to grow, all the while mindful of the pace of economic growth.

“Precise deleveraging,” or curbing debt growth in some sectors while encouraging lending in others, is a difficult task, said Larry Hu, head of China economics at Macquarie Securities Ltd. in Hong Kong. “China is still in an early stage of the easing cycle, and we expect economic growth to slide further toward the end of the year when more loosening measures will come into place.”

--With assistance from Ling Zeng and Heng Xie.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Karthikeyan Sundaram

©2018 Bloomberg L.P.

With assistance from Editorial Board