Kuroda Pushes Through Changes to Stay the Course for Longer Haul

The Bank of Japan will apply negative interest rates on fewer bank reserves to cushion the impact on commercial lenders.

(Bloomberg) -- Bank of Japan Governor Haruhiko Kuroda revamped his massive monetary stimulus program for the long haul while taking steps to reduce its side effects.

Facing down market speculation that he would make broader changes, Kuroda on Tuesday committed to “continuous powerful monetary easing” that leaves him at odds with counterparts such as the U.S. Federal Reserve which are tightening policy. The open-ended plan pledged to keep interest rates at extremely low levels for an "extended period".

At the same time, the central bank delivered a range of adjustments designed to alleviate strains from negative rates and asset-buying on commercial banks and reduce market distortions.

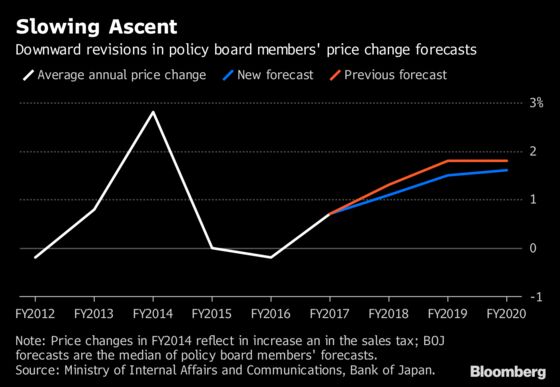

Kuroda’s now equipped for a more drawn-out campaign to generate 2 percent price gains, a goal the central bank forecasts will take even longer than it previously thought to achieve.

"The BOJ is now more engaged and prepared to fight a long-run battle against deflation or disinflation," said Shigeto Nagai, Head of Japan Economics at Oxford Economics.

Read more: Kuroda Dusts Off Bernanke’s Playbook on Forward Guidance

Japan’s benchmark 10-year yield, which the central bank will now allow to trade as much as 0.2 percent above or below its zero percent target, sank four basis points to 0.062 percent. That’s the lowest in more than a week. Yields had been testing 0.1. percent for days and some investors expected more hawkish change from the BOJ.

The yen fell 0.4 percent to 111.49 per dollar, the weakest in more than a week. The Topix stock index sank 0.8 percent to the lowest in a week on the biggest decrease in almost four weeks. Japan’s currency had strengthened leading into the meeting.

Key Points

- Negative interest rate of -0.1 percent maintained, but will apply to fewer reserves to cushion the impact on commercial banks.

- Target yield for 10-year bonds remains 0 percent while BOJ will now tolerate deviation from this by as much as 0.2 percent.

- Forward guidance added to these policy rates, with a commitment to keep the current extremely low levels for short- and long-term interest rates for an "extended period of time".

- Overall purchases of exchange-traded funds are kept at 6 trillion yen ($54 billion) but those linked to the Topix will increase to 4.2 trillion yen, from 2.7 trillion yen, further reducing the weighting of the narrower Nikkei 225.

As the side effects of its policies piled up, the central bank faced pointed questions about how long it could keep them in place. Inflation remains less than halfway to the target after more than five years of extraordinary stimulus.

The BOJ added language to its bond buying program stating that "the yields may move upward and downward to some extent mainly depending on developments in economic activity and prices."

Some observers saw Tuesday’s developments as a precursor to policy normalization some time in the future.

"It seems to me this is a ‘tour de force’: allowing a wider range for bond yields is probably a necessary precondition for the BOJ to remove itself from the bond and equity markets, in which sense this is a (baby) step towards normalization, and one that hasn’t even caused a slight wobble in other markets," said Kit Juckes, a London-based strategist at Societe Generale SA.

Societe Generale now doesn’t expect a change in policy before the second half of 2020.

Read more: Forward Guidance Is Windfall for Bonds, Pain for Banks

Speculation that policy tweaks were afoot increased as traders awaited the announcement, which finally came at 1:03 pm in Tokyo -- the latest since the yield-curve control program was introduced in September 2016.

Inflation Outlook

The central bank now sees core consumer prices rising just 1.1 percent in the current fiscal year through March, down from 1.3 percent projected previously. The estimate for fiscal 2019 was cut to 1.5 percent, from 1.8 percent, while fiscal 2020 was trimmed to 1.6 percent, from 1.8 percent.

The new forecasts show the BOJ’s struggle to stoke inflation. Meanwhile, the Fed last month raised rates for a sixth time in 18 months and set a steeper rate-hike trajectory, while the European Central Bank has plotted the end of its asset purchases this year.

"They tried their best to avoid the perception of tapering or normalization by introducing the forward guidance," said Nagai. "The guidance is vague but gives some assurance that the current easing measures will continued at least into fiscal 2020, after checking the side effects of the planned consumption tax hike."

What Our Economist Says ... |

The introduction of forward guidance is likely to increase the predictability of further policy adjustments, Bloomberg Economics’ Yuki Masujima wrote. "Our first take is that the BOJ’s next move is likely to be an incremental boost to its yield-curve targets. The move, however, is unlikely to happen by the end of this year, given the introduction of forward guidance to maintain the current extremely low yields for an extended period, and more flexible bond purchase operations to allow a wider range of yield curve changes." |

The BOJ released a detailed report on Tuesday analyzing why inflation hadn’t risen as expected. It cited factors such as rising numbers of women and seniors entering the workplace, which has weighed on wages.

Kuroda has consistently emphasized the need to stay the course with stimulus. At a press conference on Tuesday he said reaching the inflation target will take more time than expected, and that the BOJ will adjust policy as needed to maintain price momentum.

“The BOJ never had, and under Kuroda probably never will have, any intention of turning hawkish,” said Roberto Perli, a partner at Cornerstone Macro LLC in Washington and a former Fed economist. “Kuroda is serious about doing all he can to bring inflation up to acceptable levels on a sustained basis.”

--With assistance from Paul Jackson, Kazunori Takada, Gearoid Reidy, Go Onomitsu, Russell Ward, Shoko Oda, Emi Urabe, Connor Cislo, Takashi Nakamichi, Jason Clenfield, Junko Hayashi, Kyoko Shimodoi, Takashi Amano, Takashi Hirokawa, Hiroshi Miyazaki and Yoshiaki Nohara.

To contact the reporters on this story: Yuko Takeo in Tokyo at ytakeo2@bloomberg.net;Masahiro Hidaka in Tokyo at mhidaka@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Brett Miller at bmiller30@bloomberg.net, Henry Hoenig

©2018 Bloomberg L.P.