China's Bond Traders Embrace Leverage Again on Policy Shift

China's Bond Traders Embrace Leverage Again on Shift to Stimulus

(Bloomberg) -- China’s policy shift toward economic stimulus has spurred a comeback in leveraged bond investments, just two years after authorities kicked off a campaign to curb excess borrowing.

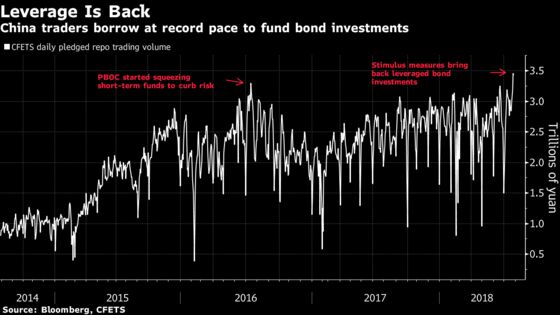

Bond traders have taken the slew of credit-boosting measures unveiled in the past week as a green light to borrow, as seen in a jump in repurchase agreements to a record high. That’s in turn helping to pull down yields in the credit market, amplifying the impact of authorities’ moves.

The repo market is mainly a cash-management resource for banks, but was a source of the buildup of financial leverage that was targeted by officials earlier this decade -- when traders would put up collateral to borrow cash and then typically reinvest in riskier assets. Renewed growth in the practice may now help ease a credit squeeze that led to a record pace of corporate defaults.

“What has become certain is monetary policy won’t tighten” with the economy under pressure, said Shen Bifan, chief strategist at Shenzhen Spruces Capital Management Co. “Credit-easing policies also convinced the market it’s bargain-hunting time for at least some corporate bonds, after a very bad first half.”

Among the steps that helped shift market sentiment:

- The People’s Bank of China’s record injection of medium-term lending facility (MLF) funds to banks Monday. On top of expanded liquidity since the start of June, it’s helped the seven-day repo rate to average just 2.66 percent the past 20 days, the lowest since March 2017.

- The PBOC’s “window guidance” to banks to use MLF funds to support credit facilities, as reported by China Business News.

- Friday’s PBOC move to soften implementation of tightened regulation of the asset management industry.

- A State Council meeting Monday urged financial institutions to meet reasonable borrowing demands from local government financing vehicles -- effectively singling out the most favorable type of credits to investors.

- The PBOC told some banks Wednesday that a capital requirement will be eased to support lending, Bloomberg News reported.

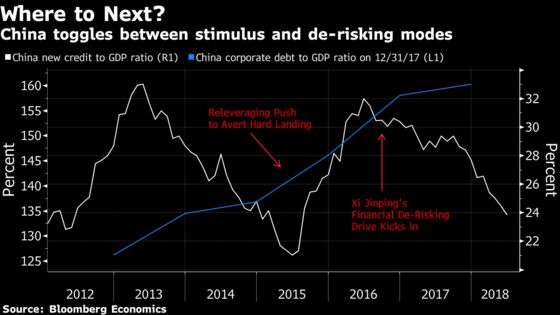

The deleveraging push wasn’t even mentioned in the cabinet’s statement Monday, which exposes the potential downside to policy makers’ about-turn: a halt to the progress made in arresting China’s buildup of debt.

“The price to pay will be a setback in the deleveraging campaign, which will increase the risks to financial stability,” Dariusz Kowalczyk, a Hong Kong-based senior emerging market strategist at Credit Agricole SA, wrote in a report on July 25. The benefit is that the supports to growth should offset any hit to exports from rising U.S. tariffs, he wrote.

China may need it -- the earliest indicators for July showed the economy slowed further this month.

Bond yields are certainly cooperating in the endeavor: yields on three-year AAA rated corporate debt have tumbled to 4.11 percent, lowest since February last year, ChinaBond data show. While lower-rated securities have only seen a small retreat in rates, the direction of travel to market players is clear. Trading volume across all types of bonds hit a record 781 billion yuan ($115 billion) Tuesday, data from National Interbank Funding Center show.

“The bullish market outlook has become an almost consensus, and that certainly will result in a re-leverage boom,” said Shi Min, credit investment director at Beijing Lerui Asset Management Co. “We don’t expect to see tightening measures until data show the economy stabilizes and aggregate financing recovers.”

--With assistance from Jing Zhao.

To contact Bloomberg News staff for this story: Helen Sun in Shanghai at hsun30@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, ;Sarah McDonald at smcdonald23@bloomberg.net, Christopher Anstey

©2018 Bloomberg L.P.

With assistance from Editorial Board