Fed Presidents Seek Powell Put to Prevent Inverted Yield Curve

Powell is now under pressure to adopt what would amount to a put of his own.

(Bloomberg) -- When Alan Greenspan ruled the Federal Reserve, investors became convinced the central bank could be counted on to prevent a stock market collapse -- the so-called Greenspan put. Now, Chairman Jerome Powell is under pressure to adopt what would amount to a put of his own, except this time it would be tied to the bond market.

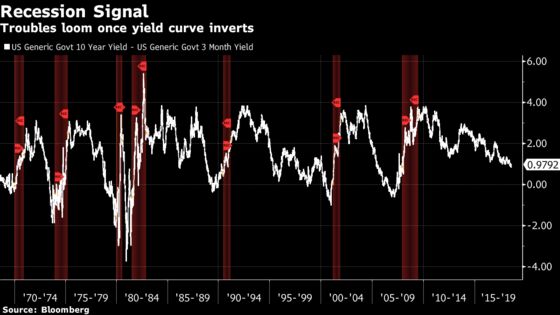

Some Fed regional bank presidents want the central bank to be cautious in raising interest rates to prevent short-term Treasury yields from rising above long-term ones -- providing a kind of comfort that Greenspan gave equity investors. Those policy makers argue that such a yield-curve inversion has proven to be a reliable harbinger of past recessions.

While sounding sympathetic to their worries, Powell doesn’t seem inclined to go along with the idea of running monetary policy to avoid flipping the curve.

“He’s acknowledged but not embraced” their concerns, said Lou Crandall, chief economist for Wrightson ICAP LLC.

Under the Greenspan put -- which the then chairman denied ever existed -- investors expected the Fed to cut interest rates if the stock market showed signs of cracking. A Powell put would operate in much the same way in the bond market. If the yield curve inverted the Fed would be expected to cut rates, thus pushing up prices of shorter-dated Treasury debt and lowering their yields.

Powell and his Fed colleagues meet on July 31 to Aug. 1 to map monetary strategy in the wake of a fusillade of criticism from President Donald Trump about their rate increases. While investors expect the Fed to hold policy steady next week, they see a better-than-even chance it will increase rates twice in the second half of 2018, in spite of Trump’s attacks.

As investors have become more convinced this year that the Fed will keep raising rates, the yield curve has flattened, with short-term yields rising more than long-term ones. That trend has been interrupted in recent days by Trump’s disparagement of the Fed and by speculation that the Bank of Japan will scale back its support of the Japanese and global bond markets.

Fed presidents have used this year’s flattening curve to argue that the central bank should tread warily in raising rates all that much further so as to avoid an inversion. History is on their side: Over the past 50 years, the U.S. has always tumbled into recession within a year or two of the curve flipping.

“Given tame U.S. inflation expectations, it is unnecessary to push monetary policy normalization to such an extent that the yield curve inverts,” St. Louis Fed President James Bullard said in Glasgow, Kentucky, on July 20.

Powell sought to shift the focus away from just the curve per se in congressional testimony last week. He said it was clear why short-term yields have climbed: The Fed is increasing rates. What’s important is “what’s going on with longer-term rates” and what that says about the stance of monetary policy.

In raising its federal funds rate target to a range of 1.75 percent to 2 percent in June, the Fed described its policy as accommodative and continuing to support the economy.

Federal Open Market Committee participants pegged the neutral funds rate -- the rate that neither promotes nor holds back growth -- at 2.9 percent, according to their median projection released in June.

Higher Neutral

Former Fed official and Cornerstone Macro LLC partner Roberto Perli said the markets seem to place the neutral rate somewhat higher, at around 3.25 percent.

On its face, that would imply that the Fed could raise rates and invert the curve -- the yield on the 10-year Treasury notes is now around 2.95 percent -- without needing to worry about overly restricting the economy.

“A yield curve that is flat or inverted now doesn’t mean that policy is tight so much as it means we are getting near neutral,” said Yale University professor William English, who stepped down as a special adviser to the Fed board last year.

Fed Governor Lael Brainard suggested in a May that an inverted curve may not be as much of concern today. That’s because long-term rates are “very low” by historical standards so it wouldn’t take much to flip the curve.

Asset Purchases

Massive bond purchases by the Fed and other central banks have held down longer-term yields. Those purchases have turned the term premium -- the amount of extra compensation investors demand to hold longer-term debt -- negative, according to calculations by some Fed economists.

While a flip in the yield curve has been a dependable precursor of past recessions, it’s not completely clear why that’s the case.

Perhaps the best explanation is that it squeezes banks, which borrow money at short-term rates to lend it out longer-term. When short rates rise above long ones, that strategy is no longer profitable, so banks scale back lending to businesses and households.

“You get a slowdown of credit growth with a time lag,” said Joachim Fels, global economic adviser at Pacific Investment Management Co. That in turn “contributes to an economic slowdown or a recession.”

Powell suggested to reporters in March that it was an open question whether an inverted curve affected the provision of credit to the economy. “It’s hard to find it in the data,” he said.

Today’s debate over the significance of the yield curve recalls a similar discussion ahead of the last recession.

A month after taking over as Fed chairman in February 2006, Ben Bernanke played down the gap’s importance.

“I would not interpret the currently very flat yield curve as indicating a significant economic slowdown to come,” he said in a speech in New York.

Twenty-one months later, the economy fell into its worst downturn since the Great Depression.

--With assistance from Craig Torres and Steve Matthews.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.