ECB's Bond Recycling Grabs Investor Attention Until Rate Liftoff

ECB's Bond Recycling Grabs Investor Attention Until Rate Liftoff

(Bloomberg) -- The European Central Bank’s next big agenda item is figuring out what it wants to achieve with its debt-recycling business.

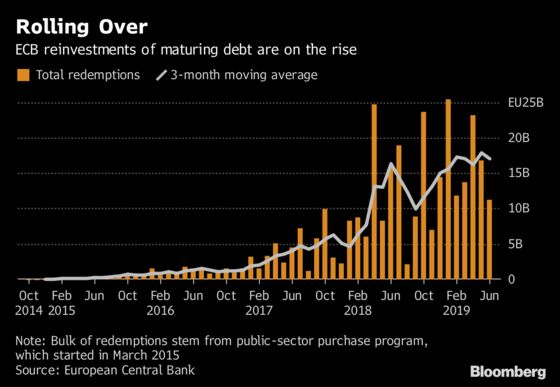

The ECB plans to stop adding to its bond-buying program by the end of this year, when holdings reach 2.6 trillion euros ($3 trillion), but it’ll keep plowing the cash from maturing debt back into the market. That reinvestment strategy will be a key focus for investors until the central bank starts raising interest rates, which President Mario Draghi says is at least a year away.

What matters is whether the process remains largely mechanical -- which could increase market volatility as monthly redemptions are highly uneven and rising -- or if the ECB opts to echo the Bank of Japan and Federal Reserve in targeting its spending to better support the economy. The Governing Council, which will meet on Thursday, hasn’t yet held formal talks on the matter.

“It’s one of the missing pieces of the puzzle,” said Richard McGuire, head of rates strategy at Rabobank International. “It’s a part of their arsenal, which they’ll wish to maintain for as long as possible in order to have that optionality should they feel the need to provide some support to the market.”

One option is to extend the window for reinvestments, currently done within three months of redemptions. That would give the ECB more flexibility to provide a steady flow of spending and smooth out the impact. Around 180 billion euros of debt will mature next year.

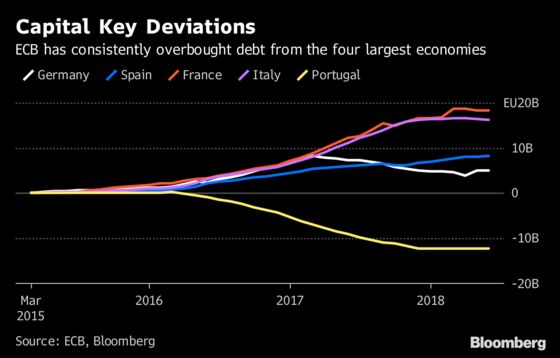

Another choice might be to use reinvestments to realign quantitative easing with the capital key, which is used to allocate purchases to national central banks -- which do most of the buying -- according to the relative size of their economies.

That guideline aims to ensure all euro-zone countries benefit equally from the program, and to combat accusations the ECB is financing governments, which is barred by European Union law. Yet holdings are currently skewed toward large economies, as some smaller nations have run into a scarcity of available debt.

The imbalance could be redressed if national central banks cooperate to reinvest across borders. Such a strategy isn’t allowed under current rules, though those only apply until the end of net asset purchases. Alternatively, the Frankfurt-based ECB could draw on its own portfolio of bonds.

Either approach could also mean that Greece, which has been excluded from QE because of its financial crisis and bailout, might still be able to benefit.

A more aggressive strategy would be to deliberately use reinvestments to influence market bond yields.

Belgium’s central-bank governor, Jan Smets, said in a newspaper interview in late May that the ECB will continue to put downward pressure on long-term market interest rates. But unless the central bank specifically focuses reinvestments on longer-dated bonds, those rates will begin to rise and tighten financial conditions as the average maturity of the QE portfolio declines.

Key officials in charge of devising the ECB’s strategy are wary of a premature erosion of stimulus, and chief economist Peter Praet signaled last October that the institution has studied efforts made by its peers.

Under its Operation Twist policy from 2011 to 2012, the Federal Reserve swapped short-term bonds with longer-dated ones to flatten the yield curve. The Bank of Japan has used asset purchases to control its curve since 2016 -- and yields surged this week on a report that policy may be tweaked.

Read more: Euro Bond Market Has Got Ahead of Itself on ECB Operation Twist

For Executive Board member Benoit Coeure, managing the maturity of the ECB’s holdings isn’t likely to be a key feature of its plans.

“I see it as a technical discussion; I don’t see it as a major aspect of our monetary policy when it comes to the maturities,” he told Bloomberg TV this month. “But the commitment to reinvest is important because it will ensure a continued market presence, which is important to maintain the degree of monetary accommodation.”

Any strategy that provides added stimulus is likely to be opposed by Germany’s Bundesbank, which has made clear that any changes to the rules shouldn’t be motivated by a desire to provide an additional monetary-policy impulse.

What Our Economists Say“A more flexible reinvestment policy cannot be a significant source of stimulus. The balance sheet rollover is simply too slow to deliver a material boost to the economy, and it happens in fits and starts. Still, the ECB owns a vast chunk of marketable debt and risks distorting some markets -- a bit more freedom to iron those out wouldn’t do any harm.”--Jamie Murray, Bloomberg Economics |

Another tool available to the ECB is increased transparency -- telling investors not just how much debt matures but where, to avoid speculation about market presence.

Most economists surveyed before Thursday’s ECB meeting foresee maturing debt being rolled over for two to three years. None expects the Governing Council to announce a fresh strategy this week.

SURVEY REPORT: The ECB Prepares for Rate Hikes in 2019

“We have the remaining net asset purchases of this year, we have the forward guidance on interest rates and we have the reinvestments of the stock of bonds that we purchased so far,” Draghi told European lawmakers this month. “It’s another important decision that we’ll take in the months ahead. I can agree with you that the certainty about this last dimension is important.”

To contact the reporters on this story: Jana Randow in Frankfurt at jrandow@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Paul Gordon, Brian Swint

©2018 Bloomberg L.P.