Goodbye, China Deleveraging. Onward Belt and Road?

(Bloomberg Opinion) -- With China’s fiscal, monetary, currency and credit policies all taking a pro-growth turn, President Xi Jinping’s deleveraging campaign is clearly over. Or, at the very least, it’s going into the freezer for as long as there’s no letup in trade tensions with the U.S.

But what about Xi’s other pet idea? In Southeast Asia, the ambitious belt-and-road project witnessed a 36 percent year-on-year decline in investment commitments and construction contracts in the first half. The setback is temporary, according to Citigroup Inc., which expects Beijing will yield to its partners’ concerns for the sake of its “overarching geostrategic imperatives.”

Maintaining the region’s confidence in belt-and-road may be a crucial defense against domestic fragility. The yuan is at its weakest in more than a year; banks’ reserve ratio has been cut three times; and now, following a meeting of the State Council, authorities are vowing a “more proactive” fiscal policy. The People’s Bank of China will extend credit via a medium-term lending facility for lenders to buy corporate bonds — the funding could be twice the size of purchases if the securities are rated AA or below.

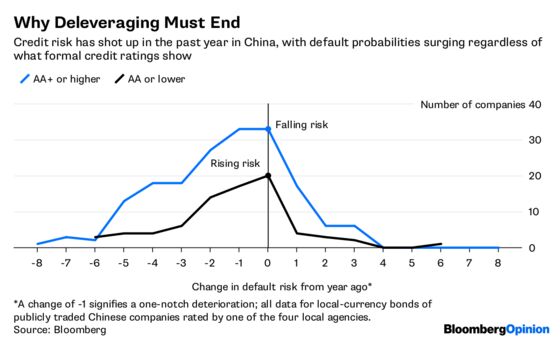

All this is clearly aimed at reining in rising distress. Including the recent cross-defaults on 13 of coal miner Wintime Energy Co.’s bonds — totaling about 10 billion yuan ($1.5 billion) — the default rate in China may now be running at 0.52 percent, higher than the 2016 peak of 0.45 percent, according to Bank of America Merrill Lynch’s calculations.

Southeast Asia and Pakistan may use the opportunity to shave a few billion dollars off interest costs. To the extent Beijing’s attention is diverted to fighting fires in the domestic economy, overseas recipients of Beijing’s infrastructure financing are bound to demand — and get — sweeter terms.

Malaysia’s new Prime Minister Mahathir Mohamad has sent an emissary to China to renegotiate loans and contracts. In Thailand, there’s nervousness about a five-year plan to redevelop the country’s eastern seaboard as a trade and transport hub — and link it with belt-and-road. There’s no guarantee the next civilian government will continue to back the $51 billion makeover, or that it won’t spend the money instead on farmers in the landlocked northeast.

A bigger and more immediate test for China, however, may arrive after Wednesday’s elections in Pakistan. Opposition leader Imran Khan, while not repudiating his country’s growing dependence on Beijing, hasn’t ruled out re-examining the loans for a $62 billion China-backed trade corridor if his party forms a government. Imports of machinery and transport equipment to set up the corridor have sunk the Pakistani rupee by 18 percent over the past year, leaving Islamabad in the unenviable position of managing its hard-currency shortfall by taking yet more loans from its regional neighbor.

With its own competitiveness under threat from U.S. President Donald Trump’s hawkish policies and posturing, China has an increasing need of its Asian allies — for everything from relocating low-cost manufacturing to sourcing chemicals, clothing and soybeans. Deleveraging at home can be allowed to be a casualty of a global trade war. But leaving marquee Chinese projects stranded overseas, with partners complaining about high debt and low returns? That simply won’t do.

Pakistan’s next prime minister should aim to show up in Beijing with a list of demands. Odds are, he won’t return empty-handed.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.