Markets Should Brace for a Repeat of September 2015

Markets Should Brace for a Repeat of September 2015

(Bloomberg Opinion) -- U.S. Federal Reserve Chairman Jerome Powell signaled in testimony this week before Congress that the economy is strong enough to keep raising interest rates in a gradual manner, even with concern about the adverse fallout from a budding trade war. While the positive message on the economy has supported equities and the dollar while weighing on U.S. Treasuries, investors may want to refresh themselves with the events of September 2015.

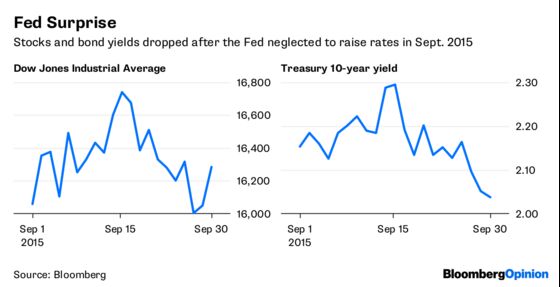

That’s when a much-heralded Fed rate increase, which would have been the first since the 2008 financial crisis, failed to materialize. Spooked by the sharp drop in Chinese equity prices and the devaluation of the Chinese renminbi that August, the Fed decided to keep rates unchanged near zero. Could it happen again this September, when the Fed is widely expected to raise interest rates for the eighth time in this current cycle? And what would it mean for financial markets?

The continuation of easy monetary conditions three years ago failed to spark a rally in financial assets. Rather, it led investors to sell equities and buy Treasuries. After all, what did the Fed know that investors didn’t that caused the central bank to unexpectedly strike a cautious tone? That episode could provide a roadmap for investors in a couple of months.

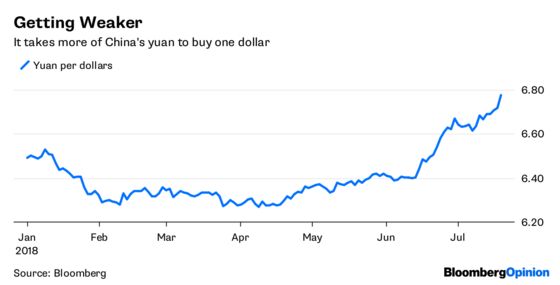

Current events are starting to look eerily similar to the developments of the summer of 2015. China’s currency has weakened sharply in the past two months as capital outflows accelerated due to fears of the adverse impact on that nation’s economy from U.S. tariffs. The renminbi depreciated beyond the crucial level of 6.70 per dollar on Thursday to its weakest level in more than a year. Some analysts believe the rate could weaken to 7 per dollar before long. At the same time, the Shanghai Stock Exchange Index has been under pressure, dropping 14 percent over the past eight weeks.

Should the renminbi’s declines become disorderly — as they did in August 2015 — it could lead to a significant correction in U.S. and European equities because the weaker currency would discourage Chinese imports, affecting the bottom line of Western companies. Investors also fear an adverse impact on the debt service costs of Chinese local governments and state-owned enterprises as a result.

Developments in China are not the only factors that the Fed has to worry about. Consumer sentiment fell to a six-month low this month due to concern about the trade tariffs, according to a University of Michigan survey released on July 13. U.S. Labor Department figures show that average weekly real earnings slowed to a crawl, from an annualized rate of 0.8 percent in June 2017 to just 0.2 percent in June 2018. Both these developments will likely lead to slower growth in consumption spending, which accounts for about 70 percent of U.S. gross domestic product.

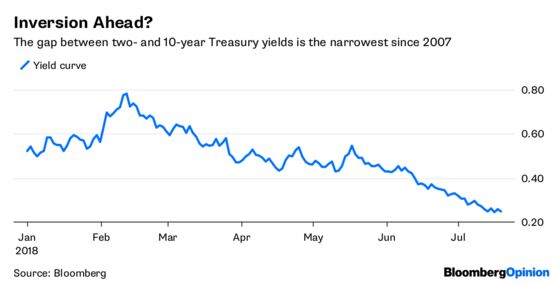

The market for Treasury securities reflects the weakness in incoming data. The difference between two- and 10-year note yields shrank to 24 basis points on July 17, the narrowest level in 11 years. The flattening of the so-called yield curve has led to growing concern that another increase in rates by the Fed could cause the spread to turn negative. Such inversions in the yield curve have been leading indicators of recessions about a year later.

It will be important for investors to watch developments on the trade front in the run-up to the crucial Fed meeting on Sept. 25 and 26. President Donald Trump shows no sign of backing off from imposing tariffs on several trade partners, and every one of those partners is expected to retaliate with their own measures. Harley-Davidson Inc. and General Motors Co., two companies that have said the tariffs would negatively impact earnings, are likely to be followed by other U.S. companies whose foreign sales are reduced by the trade war. Expect this to be reflected in the share prices in a wide range of sectors.

Even though yields on two-year Treasuries are likely to continue to increase as Powell flags further increases in the federal funds rate, a last-minute decision not to hike would cause those yields to fall sharply along with 10-year yields. And rather than produce an equity rally, a deviation of monetary policy from the Fed’s suggested path is likely to prove to be a bearish signal.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2018 Bloomberg L.P.