Rising China Economic Strain Prompts Talk of Policy Rethink

China’s economic policy could be in line for a rethink.

(Bloomberg) -- China’s economic policy could be in line for a rethink.

A slew of negative headlines from the escalating tension with the Trump administration and slowing growth to a bear market in stocks is prompting renewed focus on if and how policy makers will respond.

Whether that’s a softening in Xi Jinping’s signature anti-leverage campaign or an official shift to monetary easing to match tweaks already made, upcoming meetings of the top political leadership provide an opportunity for a change of direction -- or an affirmation of the course already set.

“We are watching closely what the Politburo meeting is going to say about the bigger environment and what is the top leadership’s assessment,” said Gao Yuwei, a researcher at Bank of China Ltd.’s Institute of International Finance in Beijing. “Will there be any policy shift or fine-tuning in the second half? Will there be any new language on hot issues such as financial risks and the property market?”

The Communist Party’s 25-member Politburo is expected to meet around the end of this month. The gathering comes at a time when academics, economists and some officials have come to question whether the leadership has overreached both domestically and internationally.

On the face of it, China’s now experiencing the most severe convergence of negative economic and financial events since the botched yuan devaluation of 2015. Stocks tumbled into a bear market last month, the yuan is heading for its sixth week of declines, and corporate defaults are running at an all-time high.

Add the unknowable effects of the trade war with the U.S. into the mix, and there would be good reason for officials to ease off on the growth-sapping debt campaign. In an interview aired on CNBC Friday evening Chinese time, Donald Trump said he’s “ready to go” with $500 billion in tariffs on Chinese imports, which is about the value of goods shipped into the U.S. from China last year.

China’s Ministry of Commerce didn’t immediately respond to a Bloomberg inquiry seeking a response to the comments out of hours.

After Xi returns from his current trip to the Middle East and Africa, he will likely also huddle with party elders in the seaside resort town Beidaihe for an annual retreat to discuss key policy decisions. The economic woes amount to one of the biggest tests for Xi since he got the party to elevate him to the ‘core’ of its leadership and abolish presidential term limits.

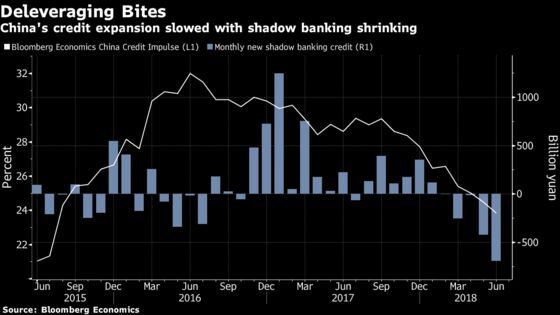

Yet Xi’s aggressive strategy to reduce financial risks in the economy is showing signs of working, with new credit as a percentage of GDP declining close to a three-year low in June, according to a Bloomberg Economics gauge. The head of the PBOC’s statistics department was cited on Friday as saying that the debt campaign was now “in a stabilization phase,” indicating that the toughest period may be over.

It’s another reason some observers think policy makers will take their foot off the brakes as signs of economic weakness emerge. Banks are being offered cash and given instructions to boost lending in a move economists say is designed to offset the impact of Xi’s de-risking campaign on growth.

Officials will have to carefully balance any easing of the credit curbs against the danger that giving up on it altogether will store up trouble down the road.

“There’s no easy solution for them,” said Michael Every, head of financial markets research at Rabobank Group in Hong Kong.

To be sure, China’s slowdown has been modest until now. The economy grew by 6.7 percent in the second quarter and key readings on exports and retail sales continue to hold up.

The current macro environment is also much better than it was in 2015 when China last experienced a market wobble, implying less need for a wide-scale policy response, according to Helen Qiao, a Hong Kong-based economist with Merrill Lynch Asia Pacific Ltd.

“Top decision makers seem to believe overall growth is fine, and there are only local problems in limited areas,” said Helen Qiao, a Hong Kong-based economist with Merrill Lynch Asia Pacific Ltd.

“Consequently, economic policies will only include surgical remedies that target those sectors, but are unlikely to include a whole-body steroid treatment yet,” said Qiao.

Still, the mood music is changing and officials in the finance ministry and central bank are debating who should take the lead on increasing support as growth slows. Xu Zhong, a PBOC official, has blasted the finance ministry for not doing enough to support the economy during the deleveraging phase.

New data on Monday showed second-quarter growth slowed and factory activity cooled more than expected. The shadow banking sector saw the biggest net monthly drop on record in June, according to Bloomberg calculations based on the central bank’s data, weighing on the supply of new credit to the real economy.

The yuan’s slump deepened Friday after the central bank weakened its daily reference rate for the currency by the most in two years, raising questions around how far it will weaken. This month was marked by one of the biggest corporate-debt defaults yet, with the downfall of a coal miner.

“It’s true that China is now in a difficult time,” said Xia Le, chief Asia economist at Banco Bilbao Vizcaya Argentaria SA in Hong Kong. “Key to breaking the cycle of bad news is for the authorities to make more progress in structural reforms. Further opening-up of the domestic market will be a good idea under the current circumstances as new foreign investment can bring new impetus to China’s growth and offset the negative impact from U.S. trade-war threat.”

--With assistance from Yinan Zhao.

To contact Bloomberg News staff for this story: Enda Curran in Hong Kong at ecurran8@bloomberg.net;Miao Han in Beijing at mhan22@bloomberg.net;Peter Martin in Beijing at pmartin138@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Reinie Booysen

©2018 Bloomberg L.P.

With assistance from Editorial Board