Panic Roils China's Peer-to-Peer Lenders

Panic Roils China's Peer-to-Peer Lenders

(Bloomberg) -- China’s savers are rushing to pull money from peer-to-peer lending platforms, accelerating a contraction of the $195 billion industry and testing the government’s ability to maintain calm as it cracks down on risky shadow-banking activities.

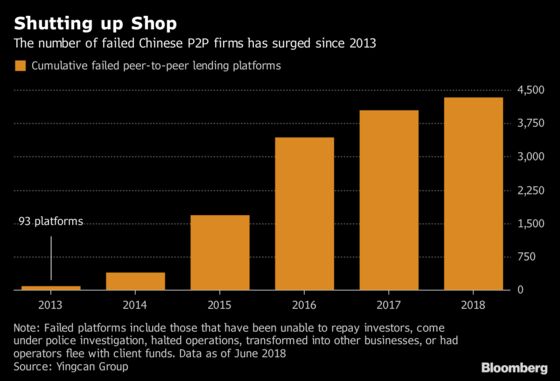

In some cases, savers are turning up at the offices of P2P operators to demand repayment, spooked by reports of defaults, sudden closures and frozen funds. At least 57 platforms have failed in the past two weeks, adding to 80 cases in June, the biggest monthly tally in two years, according to Shanghai-based Yingcan Group. The researcher defines failed platforms as those that have halted operations, come under police investigation, missed investor payments, moved into other businesses, or had operators flee with client money.

“Investors have lost confidence in the smaller platforms, because they have no idea if those companies will survive,” said Dexter Hsu, a Taipei-based analyst at Macquarie Capital. Only a handful of the 2,000 or so remaining firms are likely to endure, he said.

China’s P2P industry, the world’s largest, is one of the riskiest and least-regulated slices of the nation’s sprawling shadow-banking system. A government clampdown has weighed on P2P platforms for two years, but the pressure intensified in recent months after China’s credit markets tightened and the banking regulator issued an unusual warning to savers that they should be prepared to lose all their money in high-yield products.

The shakeout has cast doubt on the listing plans of several P2P lenders and underscores the delicate balancing act faced by China’s government as it tries to reduce moral hazard in the financial system without triggering a crisis. While there’s little sign that the P2P turmoil has spread to systemically important wealth-management products issued by banks, much of China’s $10 trillion shadow-lending system faces the same headwinds of rising defaults, slowing economic growth and official calls to end to implicit guarantees on risky investments.

The China Banking and Insurance Regulatory Commission didn’t respond to a faxed request for comment.

China’s P2P platforms have about 50 million registered users and 1.3 trillion yuan ($195 billion) of outstanding loans, most of which have short maturities. Normally, savers have to wait for loans facilitated by the platforms to mature before getting their money back. But some are now trying to exit early by selling their rights to others at a discount, or by going to the platform’s offices to demand repayment.

When P2P lender Qian88.com shut last week, it cited “spreading panic among investors” as one of the reasons. Local police were called in to ensure order as customers rushed to the company’s Shenzhen office to demand their money. Another platform, Lqgapp.com, suspended operations last week after some investors talked about difficulties securing repayment in online chatrooms, triggering a flood of withdrawal requests. The platform said it will “attempt” to repay its users over the coming three years. About 220,000 investors are owed about 5 billion yuan.

David Gao, 30, who works in the financial industry in Beijing, invested 1 million yuan of of his savings in P2P loans facilitated by a Hangzhou-based platform in November and has been unable to retrieve his principal and interest. After traveling 700 miles to the company’s office with other investors last week, he found it deserted.

“I won’t invest in P2P platforms any more, I no longer trust them,” said Gao, who had been putting money into online loans for about four years. “I have to move on no matter how upset I am, but a lot of the other investors are old and are suffering more.”

The turmoil is also hurting companies and individuals who have relied on P2P platforms for financing. They include cash-strapped small businesses seeking working capital, individuals without a credit history, and, more recently, leveraged stock market investors and home buyers in need of down-payments.

Some P2P platforms were also raising funds illegally for their own use, while others were running Ponzi schemes that collapsed when the flow of new money halted, regulators have said. That helps explain why authorities have so far been steadfast in cracking down.

The government introduced a complex registration process in December to clean up the sector, with officials in Shanghai identifying 160 problem areas such as overly high interest rates, misuse of funds and exaggerated return figures.

Last month, China Banking and Insurance Regulatory Commission Chairman Guo Shuqing warned that any savings or investment product with promised returns of more than 8 percent is likely to be “very dangerous” and that investors should be prepared to lose all their money if advertised returns exceed 10 percent. The average yield on P2P loans was 10.2 percent in the first half, official figures show. Reported default rates vary from zero on the best platforms to 35 percent on the worst, according to National Internet Finance Association of China.

Authorities have yet to publish the time frame for formally registering P2P firms, meaning the sector is operating in a kind of regulatory limbo, according to Macquarie Capital’s Hsu.

That uncertainty is reflected in the stock market, where P2P lenders have slumped and initial public offerings from the industry have dried up. The U.S.-listed shares of PPDAI Group Inc. and Yirendai Ltd., among China’s biggest P2P lenders, have tumbled 38 percent and 53 percent this year, respectively. China Rapid Finance Ltd. fell 7 percent on Monday, extending this year’s decline to 68 percent. No major Chinese fintech companies have completed IPOs in 2018, despite plans by firms including 9F Group and Weidai Hangzhou Financial Information Service Co. to raise about $8 billion, according to data compiled by Bloomberg.

Even for leading P2P players, a shrinking investor base, rising defaults and higher funding costs will pose “enormous challenges,” China International Capital Corp. analysts Yao Zeyu and Pu Han wrote in a July 13 report.

--With assistance from Crystal Tse.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Alfred Liu in Hong Kong at aliu226@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Michael Patterson

©2018 Bloomberg L.P.

With assistance from Editorial Board