A U.S. Recession Indicator Flashes Red for Leuthold’s Paulsen

The less-followed indicator ‘should not be ignored,’ Jim Paulsen says

(Bloomberg) -- One gauge of recession risk with a “pretty good” track record over the last half century has just raised a cautionary signal, according to the Leuthold Group.

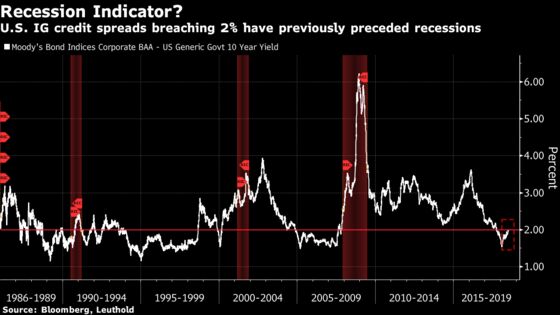

For the first time since just prior to the 2007-2009 recession, premiums on the lowest-rated tranche of investment-grade U.S. corporate bonds have risen to 2 percent after being below that level, according to data compiled by the Minneapolis-based research group. The analysis looks at the gap in yields between corporate debt rated Baa by Moody’s Investors Service and those on 10-year Treasuries.

“We are not sure why a 2 percent credit spread has been so prescient in predicting recessions since 1970,” Jim Paulsen, Leuthold’s chief investment strategist, wrote in a note to clients Monday. That happened either during or prior to six of the past seven recessions, he said.

Paulsen was quick to acknowledge that other gauges of recession risk aren’t sending the same signal. One of the more famous is an inversion in the Treasury yield curve, when two-year yields exceed those on 10-year notes, but that hasn’t happened yet. The particular investment-grade premium highlighted by Paulsen also has been well above 2 percent for practically the entire period of economic expansion since the end of the great recession.

“This less-followed indicator has a good enough relationship with recession risk during the last 50 years that it should not be ignored,” he wrote. Given that the “subpar” economic recovery has relied on unconventional monetary policy and fiscal stimulus, “would it be shocking if it ended before traditional recession indicators provided warnings,” he wrote.

Fears of accelerating inflation and a faster pace of Federal Reserve interest-rate hikes have weighed on investment-grade corporate bonds so far this year. In addition, U.S. firms are borrowing more and their interest costs are increasing.

The spread between the Moody’s Corporate Baa Bond Index and 10-year Treasuries rose to 2 percent on June 28, according to data compiled by Bloomberg. It stood at 1.96 percent on Friday.

To contact the reporter on this story: Cormac Mullen in Tokyo at cmullen9@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Adam Haigh

©2018 Bloomberg L.P.