Foreign Funds Keep Pouring Into China Despite Yuan's Jitters

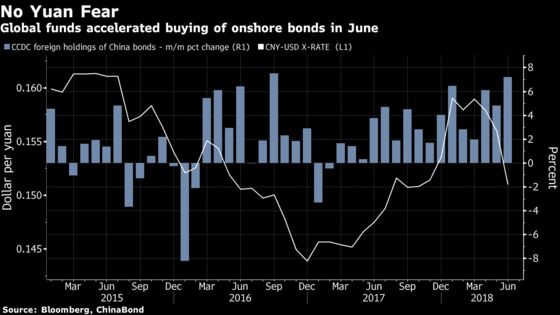

June saw the yuan’s biggest monthly drop against the dollar since 1994.

(Bloomberg) -- The sharpest decline of China’s yuan since a turbulent devaluation in 2015 hasn’t fazed international bond funds, suggesting their diversification flows will be a useful stabilizing force for the nation’s policy makers.

“The falling yuan is a concern, but as long as it’s not in a severe downtrend, it’s not the biggest consideration when we’re investing in local-currency bonds in China,” said Manu George, director of fixed income at Schroder Investment Management Ltd. in Singapore, in a view echoed by other market participants.

June saw the yuan’s biggest monthly drop against the dollar since 1994, yet overseas investors poured the most into China’s domestic bonds in almost two years. The contrast is a testament to foreign demand for exposure to the country’s $12 trillion bond market, the world’s third-largest. China has steadily opened to international investors in part to provide a balance against domestic pressures to ferret money out.

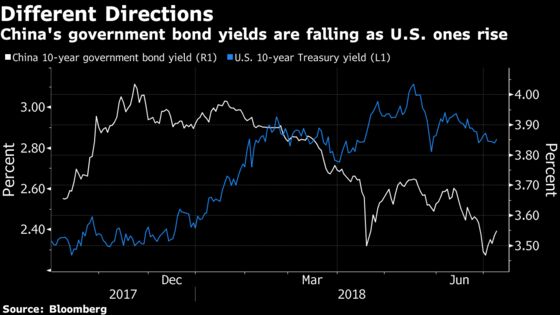

The sustained inflows are also important for China’s borrowing costs, because overseas investors have replaced domestic banks as the dominant marginal player in the government bond market this year. Their purchases have helped lower the yield on China’s 10-year notes by the most in Asia -- and among emerging markets more broadly.

Stability Pledge

While the yuan’s slide from mid-June stoked speculation China’s leadership was turning to depreciation as a weapon against U.S. President Donald Trump’s protectionist trade moves, the country’s monetary authorities have pledged a stable currency. It was little changed at 6.6148 per dollar at 3:19 p.m. in Shanghai, after jumping the most since January on Monday.

Rather than getting spooked as in 2015, when China was battling against fears of an economic hard landing, market players this time around see a weaker yuan as part of a supportive monetary stance that should prove good for bonds. And with the trade battle threatening to curb growth, Chinese policy makers also have cause to go easy on financial deleveraging, which has hammered the corporate debt market.

“Allowing yuan depreciation is part of a directed policy of easing,” said Pierre-Yves Bareau, chief investment officer for emerging-market debt at JPMorgan Chase & Co.’s asset management unit in London. “We don’t think this has parallels to the drop in 2015. Policy makers are fully in control and anchoring the situation.”

Central Banks

Ji Tianhe, a China strategist at BNP Paribas SA, went so far as to expect that “some investors would deem the depreciation a buying opportunity, as the slide creates room for future appreciation.”

Central banks have probably also been key to the inflows, said Becky Liu, the Hong Kong-based head of China macro strategy at Standard Chartered Plc. She noted that official demand takes more of a long-term view. The yuan has been rising in allocations since it won official reserve-currency status from the IMF in 2015.

Not all has been so rosy for China’s assets. Foreigners initially jumped into domestic stocks newly available in MSCI Inc.’s international indexes from the start of last month, but inflows have tailed off in the past three weeks as the yuan slid.

Net purchases via the stock connect with Hong Kong amounted to 3.2 billion yuan ($484 million) in the three weeks through July 6, compared with 48.5 billion yuan the prior three weeks, according to data compiled by Bloomberg. The CSI 300 Index has slumped 7.8 percent since June 15, in yuan terms.

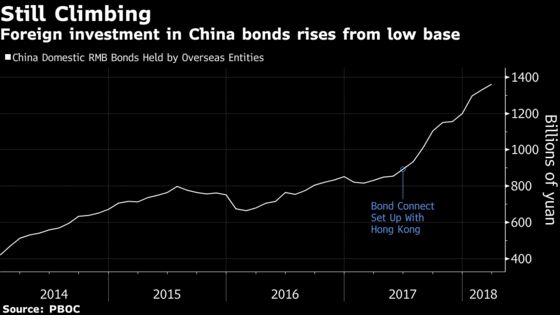

In wake of the 2015-16 capital-flight scare, Chinese authorities have been increasingly encouraging foreign-investment inflows to help balance demand for the yuan. Inclusion in international bond indexes is another objective officials continue to work on, a move that could prompt further diversification inflows.

At 1.36 trillion yuan, foreign holdings of China’s bonds are still relatively limited, People’s Bank of China data show. That amounts to little more than the equivalent of what Hong Kong holds in U.S. Treasuries alone.

“Improving market infrastructure and solving technical issues play a larger role when asset managers decide whether to invest in China” than the yuan, said Johnny Chen, a portfolio manager for Asian local-currency bonds at NN Investment Partners Ltd. in Singapore. That includes the capability for block trading, delivery versus payment settlement and more clarification on taxes, he said.

Hedging is also important, and increasingly available. Turnover of futures tied to the offshore yuan against the dollar at Hong Kong Exchanges & Clearing Ltd. surged to a record on July 3, driving the notional value to $2.2 billion, data from the bourse showed. The onshore yuan slid through 6.7 that day, spurring officials to offer their reassurance.

Among the comments, Guo Shuqing, who heads the banking regulator and serves as Communist Party chief at the central bank, said the yuan should strengthen in time.

That’s the bet of Andy Seaman, chief investment officer at Stratton Street Capital LLP. Stratton recently increased its exposure to the yuan, anticipating that rising productivity will help keep China’s current-account surplus in tact for the long haul.

--With assistance from Jeanny Yu.

To contact Bloomberg News staff for this story: Helen Sun in Shanghai at hsun30@bloomberg.net;Narae Kim in Hong Kong at nkim132@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, ;Neha D'silva at ndsilva1@bloomberg.net, Christopher Anstey, Philip Glamann

©2018 Bloomberg L.P.

With assistance from Editorial Board