Forget the Yield Curve. The Debt-Market Action Is in Fed Funds

The job of Federal Reserve officials is about to get harder.

(Bloomberg) -- With all the focus on the shape of the U.S. yield curve recently, fixed-income traders could be forgiven for not concentrating so much on the growing tumult in the fed funds rate.

Not anymore.

Rising money-market rates have forced Federal Reserve officials to take unprecedented steps to maintain control over their key policy benchmark -- and the job is about to get harder. With the Treasury continuing to ramp up bill issuance and the central bank’s balance sheet unwind accelerating, the front-end is poised to take center stage in the second half of the year.

From further policy-tool adjustments, to the outlook for balance-sheet normalization, to America’s debt-management strategy, the influence of short-term rates is set to reverberate through the financial system. It’s forcing traders to focus on funding markets once again, just months after Libor’s surge brought the usually sleepy corner of the fixed-income world roaring to the fore.

“The fed funds rate is starting to become exciting,” said Gennadiy Goldberg, a strategist at TD Securities in New York. “The money-market space is going to be squeezing the fed funds rate higher, and then you have the Fed balance sheet” runoff ramping up.

While many Fed officials have publicly expressed their angst about a possible inversion of the yield curve -- and what that would signal -- trouble in the money markets is also clearly on their minds.

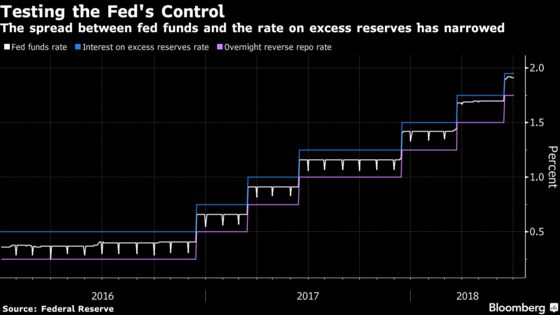

Last month, in an effort to maintain control of an effective rate that climbed to within just five basis points of their target band’s ceiling, policy makers took the unprecedented step of reducing how much they pay on excess reserves that deposit banks keep at the Fed (the IOER rate) relative to the upper bound of the range.

For a QuickTake explainer on the IOER rate, click here.

Chairman Jerome Powell, at the conclusion of the Federal Open Market Committee’s June policy meeting, acknowledged that a burst in bill issuance to plug swelling budget deficits was likely at least partly to blame for fed funds becoming unhinged.

The surge in supply pushed key overnight rates higher, especially in the market for repurchase agreements. As these other short-term assets became more attractive alternatives to lending reserves to other banks, the availability of interbank funding lessened, putting upward pressure on the policy rate.

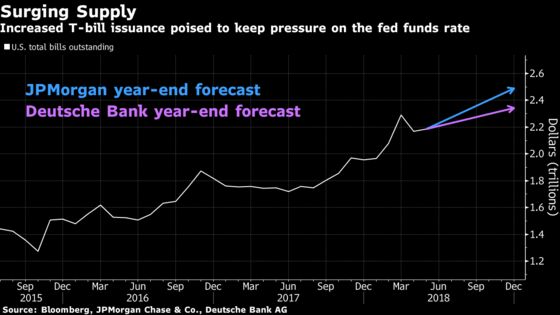

As the second half of the year gets underway, T-bill supply is poised to expand by another $290 billion, according to JPMorgan Chase & Co. estimates. Deutsche Bank AG expects an additional $185 billion of net bill sales, most of it arriving in the fourth quarter. That’s after about $200 billion of net issuance in the first six months of 2018.

The prospect of increased supply has some saying further tweaks to the central bank’s policy-setting tool will be necessary.

“While no one knows exactly where the funds rate will set, there are reasons to think that it may continue to rise, in which case another adjustment to IOER would be warranted,” said Brian Sack, director of global economics for the D.E. Shaw Group and former head of the New York Fed’s markets desk.

TD’s Goldberg expects the Fed to adjust the IOER rate again as soon as its September meeting, and sees fed funds converging with IOER by the end of the year. Minutes of officials’ June 12-13 gathering, due Thursday, may offer traders and strategists further clues.

Fed Futility

Others argue such policy action will prove futile.

Because the cause of the drift is the result of a glut in short-end supply, only coordination with the Treasury can solve the problem, according to Credit Suisse Group AG analyst Zoltan Pozsar.

“When the Fed’s floor is getting higher, the solution is not to lower the ceiling too, because then markets are going to suffocate and start punching holes in the ceiling, Pozsar said. “I find it odd that the Fed’s response to rising rates is to lower IOER when the issue is about Treasury issuing more bills.”

It’s been less than three weeks since policy makers cut by five basis points the rate they pay on excess reserves relative to the top of their official target range, and the effective funds rate has already crept higher once again. On a number of days last month it settled just three basis points from the IOER rate and eight basis points from the central bank’s upper band. The gap was four basis points on Monday.

The culprits, according to Wrightson ICAP, are likely domestic banks that have ramped up their bidding for fed funds. U.S.-based firms took 23 percent of the market share in March, up from an average of 17 percent in 2017, according to economist Lou Crandall, based on the Fed’s expanded summary of selected money-market rates. The surge in bidding likely contributed to the repricing of fed funds in mid-March, he said, and signs point to similar demand last month.

Liquidity Problem

Still others see the increasingly scarce cash balances that banks hold in reserve accounts at the Fed as the primary cause of the effective rate’s glide higher. And if the central bank’s balance-sheet unwind is already fueling a dearth of liquidity, the problem is only set to get worse.

The Fed is scheduled to shrink its holdings of Treasury and agency debt by as much as $40 billion a month beginning in July. The figure is scheduled to climb to $50 billion starting in October.

As a result of the upward drift in the fed funds rate, several analysts have already begun to re-calibrate expectations for when the runoff will end, especially given stringent post-crisis regulatory requirements that are prompting banks to increasingly hang onto their reserves.

| Maximum Monthly Reduction in Fed Holdings of Treasuries | Maximum Monthly Reduction in Fed Holdings of Agency Debt | |

|---|---|---|

| 4Q 2017 | $6 billion | $4 billion |

| 1Q 2018 | $12 billion | $8 billion |

| 2Q 2018 | $18 billion | $12 billion |

| 3Q 2018 | $24 billion | $16 billion |

| 4Q 2018 onward | $30 billion | $20 billion |

“The liquidity coverage ratio and many other regulations suggest a very high demand, and a very fluctuating demand, for reserves,” said Darrell Duffie, a finance professor at Stanford University. “For the Fed to know exactly how much excess reserves are needed to really calibrate the fed effective rate has become very hard in the new regulatory environment.”

Duffie says the era of the small balance sheet has passed. “There is too much demand for reserves now for the Fed to go back.”

Slower Unwind

Sack sees the central bank ultimately slowing the pace of its unwind and maintaining a balance sheet of no less than $3 trillion, from about $4.3 trillion currently.

It sets the stage for a tumultuous second half of the year, one in which market participants are still going to have to navigate additional rate increases, the continued effects of corporate repatriation flows, and ongoing benchmark reforms, the same issues that influenced the short-end in the first half of the year.

“The first quarter of the year was a lot of moving parts,” Credit Suisse’s Pozsar said. “And the rest of the year there is going to be a lot of moving parts, as the Fed is playing around with IOER, there’s tapering and Treasury issuance.”

--With assistance from Matthew Boesler.

To contact the reporters on this story: Alexandra Harris in New York at aharris48@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2018 Bloomberg L.P.