Where Were You During the Great T-Bill Massacre of 2018?

(Bloomberg Opinion) -- Nothing scares big investors more than the notion that the U.S. could hold a bond auction and nobody showed up. After all, Treasuries are the world’s safest investment, backed by the full faith and credit of the U.S. The securities, especially Treasury bills, are as good as cash. But on Monday, investors — and the Treasury Department — got a whiff of what disaster could look like if investors decided U.S. debt wasn’t worth the paper it was printed on.

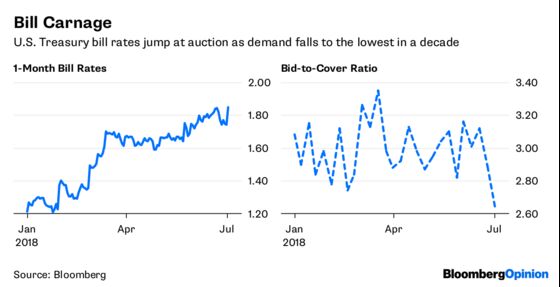

At the government’s weekly auction of four-week bills, which was moved up a day to account for the Fourth of July holiday, investors placed bids for 2.45 times the $35 billion amount offered. That’s the lowest so-called bid-to-cover ratio in a decade and far below this year’s average of 2.99 times. Rates on one-month bills shot up 10 basis points to 1.85 percent after the auction in a highly unusual move for a market that typically fluctuates only about a basis point or two a day and a sign that bond traders aren’t quite sure what to make of the poor auction. Perhaps it’s just a function of the auction’s timing, coming later on an off day in a holiday week when many A-list traders are probably out of the office. The U.S. better hope that’s the explanation, because traders have openly talked about the possibility that China might try to retaliate against tariffs imposed by the Trump administration by slowing its purchases of U.S. debt or even outright reducing its $1.18 trillion of holdings. There’s no way to prove that was at play in the four-week bill auction, but it’s also no secret the U.S. is seeking to double its borrowing this year to $1 trillion to pay for the growing budget deficit resulting from the Trump administration’s tax changes. The nonpartisan Congressional Budget Office has said the budget deficit will surpass $1 trillion by 2020, two years sooner than previously estimated.

Also on Monday, the Treasury Department auctioned $48 billion of three-month bills and $42 billion of six-month bills, with results for both coming in a bit weak. The three-month auction drew a bid-to-cover ratio of 2.62 times, the lowest since the end of 2008. Net sales of bills will amount to $272 billion this year, rising to $300 billion in 2019 and 2020, according to Morgan Stanley. Net sales were $138 billion last year, when the debt ceiling disrupted issuance.

U.S. STOCKS COMMAND A PREMIUM

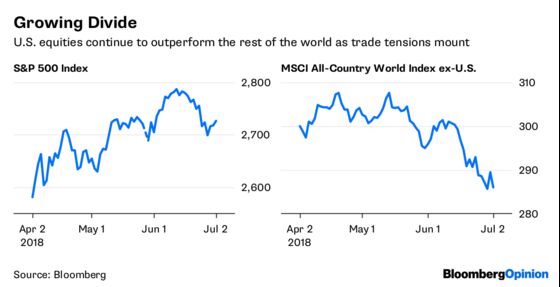

For all the talk about trade wars and their deleterious effects, equities in the U.S. are holding up quite well. The S&P 500 Index has managed to gain 1.99 percent this year, and while that doesn't sound impressive, it’s much better than the 6.37 percent decline for the MSCI All-Country World Index excluding U.S. stocks. Looked at another way, U.S. stocks trade at 16.6 times earnings estimates, a 20 percent premium to the MSCI World Index when excluding U.S. shares. That compares with the average premium of 15 percent over the past five years, according to Bloomberg Intelligence equity analysts Gina Martin Adams and Kevin Kelly. Much of that premium has to do with earnings, with earnings-per-share for American companies forecast to grow 18.1 percent on average in the year ahead, compared with 14.2 percent in all developed markets. Starting in the next few weeks, investors will get a sense of whether those forecasts are too optimistic as companies begin to report second-quarter results. At least one major constituency isn’t too confident. Spectrem Group said Monday that its monthly confidence index of affluent investors, or those with at least $500,000 to invest, dropped for a fourth consecutive month in June, falling to a level of three. That is the lowest since June 2017. The survey is based on 250 interviews.

DOLLAR BULLS MULTIPLY

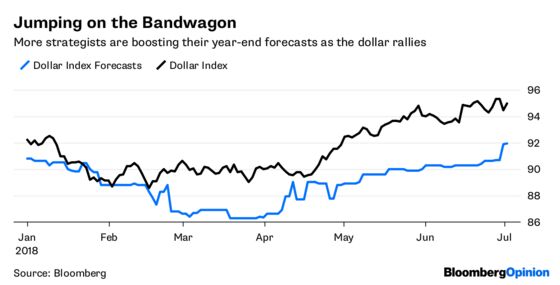

Add Bank of America Merrill Lynch to the growing list of strategists who say the dollar’s bull run is just starting. The Bloomberg Dollar Spot Index jumped as much as 0.65 percent Monday, bringing its gains since mid-April to 5.95 percent. Against the euro, the greenback has strengthened to about $1.16 from $1.2555 in February. In a report dated June 29, the foreign-exchange strategists at Bank of America wrote that they had boosted their dollar forecast to $1.12 this quarter as the U.S. economy outperforms and American companies repatriate profits held abroad in response to tax reform enacted at the end of 2017. The firm’s third-quarter forecast is much more bullish than the consensus, which shows that strategists as a whole see the dollar trading at $1.18 per euro by the end of the September. To be sure, that estimate has been getting stronger, improving from $1.25 as recently as the start of May. The upside to a stronger dollar is that it shows confidence in the U.S. and gives foreign investors an incentive to buy dollar-denominated assets, which can help keep a lid on interest rates. The downside is that it can act as a drag on exports by making U.S. goods relatively more expensive. Later this week, the government is forecast to report a trade deficit for May of $43.6 billion, based on the median estimate of economists surveyed by Bloomberg.

TRUMP HAS LITTLE SWAY OVER OIL

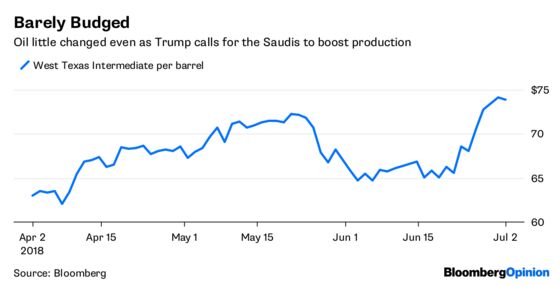

President Trump, who has expressed frustration at rising oil prices, tweeted over the weekend that Saudi King Salman bin Abdulaziz agreed to boost production to the kingdom’s maximum capacity. So it would be logical to expect oil prices to tumble on Monday. Except they didn’t. West Texas Intermediate crude was little changed at about $73.94 a barrel, up from this year’s low of about $58 in February. Oil is rising in the face of increased production from many places. Saudi Arabia boosted output by 330,000 barrels a day in June to 10.3 million a day, according to a Bloomberg News survey of analysts, oil companies and ship-tracking data. But disruptions in Libya, coupled with continuing supply losses in Venezuela and Angola, meant overall output from the Organization of the Petroleum Exporting Countries rose only 30,000 barrels a day to 31.83 million a day, according to Bloomberg News’s Grant Smith. U.S. refiners have returned from maintenance with a vengeance, processing more than 18 million barrels a day of crude and other oils for the first time in the week ended June 22, according to Bloomberg News’s Jessica Summers. As a result, gasoline stockpiles have increased 2.9 percent in June, the biggest gain for the month since 2009.

SELL ON THE RUMOR, SELL ON THE NEWS

Currency traders had weeks to prepare, but the victory by leftist candidate Andres Manuel Lopez Obrador in Mexico’s presidential election still seemed to surprise traders. The peso fell as much as 1.47 percent despite assurances from Lopez Obrador — who had been leading in the polls for a few weeks and offered up some extremely radical views, such as nationalizing Mexico's banking industry — that he will govern as a pragmatist and won’t nationalize companies. Traders are skeptical, making one-month contracts to buy the U.S. dollar against the peso the most expensive since April 26 versus contracts to buy the peso, according to Bloomberg News’s Srinivasan Sivabalan. That’s a sign traders expect the peso, which has depreciated almost 11 percent since mid-April, to fall even further. The 25-delta risk reversal, which tracks the difference in volatility between call and put options on the dollar-peso pair, rose to 1.375 percentage points. That spread was heading for the biggest three-day increase since March 2017.

TEA LEAVES

Sweden is home to this year’s worst-performing major currency, with the krona dropping 5.93 percent against the euro and 9.03 percent against the dollar. Against a basket of nine developed-market peers, the krona is down 6.39 percent, Bloomberg Correlation-Weighted Indexes show. The long-awaited start of a rebound could begin as soon as Tuesday when Sweden’s central bank releases its latest policy statement. Although the Riksbank isn’t forecast to raise interest rates, it’s widely expected to affirm plans to start lifting its key interest rate from minus 0.5 percent amid an expanding economy and signs of faster inflation, according to Bloomberg News’s Amanda Billner and Rafaela Lindeberg. To be sure, there’s plenty of room for disappointment given the potential for a trade war between the U.S. and its major trading partners that could impact the global economy.

DON'T MISS

ETF Industry Reaches Maturation Without Maturing: Jared Dillian

401(k)s Could Be a Casualty of Trump’s Trade War: Stephen Gandel

Trump's Oil Tweet Exposed His Lack of Dominance: Liam Denning

Investors Shouldn't Fear Mexican Election: Mohamed A. El-Erian

China's Foreign Investment Door Opens, Only Just: David Fickling

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.