China Set for Record Defaults, and Downgrades Tip More Pain

China heading for record bond default with 66.3 billion yuan of defaulted notes outstanding at the end of May.

(Bloomberg) -- China is zooming to a record year of corporate-bond defaults, with the 2018 total already more than three-quarters of the previous high even before an expected economic slowdown bites.

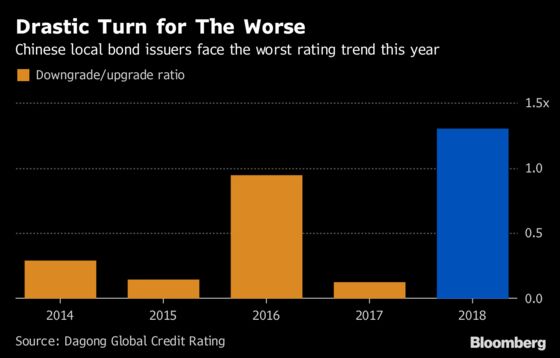

Chinese companies have reneged on about 16.5 billion yuan ($2.5 billion) of public bond payments so far this year, compared with the high of 20.7 billion yuan seen in all of 2016, according to data compiled by Bloomberg. Strains are set to get worse if the trends of credit-rating companies are anything to go by -- agencies including Dagong Global Rating Co. have been downgrading firms by an unprecedented margin.

“Corporate profits have worsened this year and are unlikely to improve against the backdrop of an economic slowdown,” Li Shi, general manager of the rating and bond-research department at China Chengxin International Credit Rating Co. “Refinancing will continue to be tough as long as the crackdown on shadow banking continues.”

The domestic corporate-debt market is almost exclusively a local affair, with foreign investors gravitating toward government-linked securities since China boosted access to its bonds in recent years. The worsening in credit quality offers little incentive to dip in now, though in time analysts see a more disciplined credit market offering diversification opportunities.

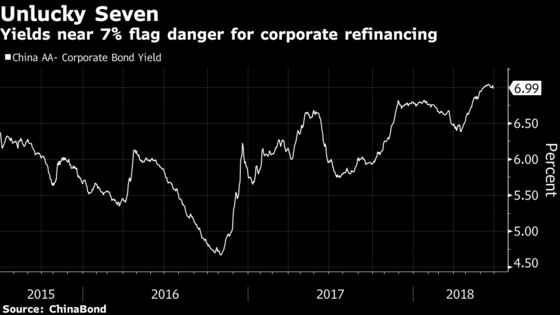

In the meantime, rising yields are set to make the refinancing of maturing debt all the tougher for private companies that lack the access to the state-dominated banking system that national behemoths enjoy. With the People’s Bank of China making only limited steps to support credit to private companies, borrowing costs show no sign of dropping.

Borrowers have missed payments on at least 20 domestic bonds so far this year, according to data compiled by Bloomberg. There was about 66.3 billion yuan of defaulted notes outstanding at the end of May, or 0.39 percent of corporate bonds outstanding, PBOC data show. While still small, that share may be poised to rise.

Dagong has reported 13 credit-rating downgrades compared with 10 upgrades so far this year, the highest such ratio on record, according to Bloomberg-compiled data. Results from Dagong peers such as China Chengxin International Credit Rating Co. and China Lianhe Credit Rating Co. show similar trends.

The silver lining is that the defaults show Chinese regulators are increasingly comfortable with allowing struggling companies to fend for themselves without official rescues. Bond defaults are good for the long-term development of Chinese markets, Pan Gongsheng, director for State Administration of Foreign Exchange, said in Hong Kong Tuesday.

‘Necessary’ Defaults

“They are necessary for better credit-risk pricing and will create a healthier bond market in the long term,” Christopher Lee, managing director of corporate ratings at S&P Global ratings in Hong Kong said of defaults. “It is unlikely there will be a wave of large-scale defaults or concentration of defaults -- any such developments will be quickly contained to prevent systemic risks from emerging.”

With rising trade tensions with the U.S. threatening to hurt corporate cash flows, the temptation to shore up credit provision may rise. Data over the weekend showed that a gauge of export orders tumbled into contraction in June.

An escalation of the trade conflict could add to defaults in China’s financial system, said Jing Ulrich, JPMorgan Chase & Co.’s vice chairman for Asia Pacific. Consumer demand and the wider economy are likely to weaken and that “may translate into worse credit quality down the road,” she said in a Friday interview in Hong Kong.

“The volume of bond defaults will most likely surpass 2016 and hit a record this year,” said Lv Pin, an analyst in Beijing at CITIC Securities. While most failures in 2016 were from state-owned firms in industries with excess capacity, the majority of defaulters this year have been private-sector firms. With a variety of industries represented, the data show the breadth of the deterioration, he said.

| Read more on China’s credit markets: |

|---|

|

--With assistance from Yuling Yang, Ling Zeng and Alfred Liu.

To contact Bloomberg News staff for this story: Lianting Tu in Hong Kong at ltu4@bloomberg.net;Jing Zhao in Beijing at jzhao231@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin, Christopher Anstey

©2018 Bloomberg L.P.

With assistance from Editorial Board