Africa Reels as Rout Spreads From Egypt Stocks to Rand Bonds

Market Rout Sends African Assets From the Rand to Bonds Reeling

(Bloomberg) -- The emerging-market sell-off is taking a heavy toll on Africa.

The continent’s bonds and stocks are being hammered more than those in most other regions amid a rout that’s wiped over $1 trillion off developing nations’ equity markets this quarter and sapped confidence from Brazil to China.

Africa’s status as the world’s fast-growing continent after Asia has done little to spare it, as traders’ appetite for higher yields wanes and they rush to cut exposure to the riskiest markets. The downturn, triggered by investor concerns over a strengthening dollar and rising U.S. Treasury rates, has accelerated as tensions worsen between Washington and Beijing over trade.

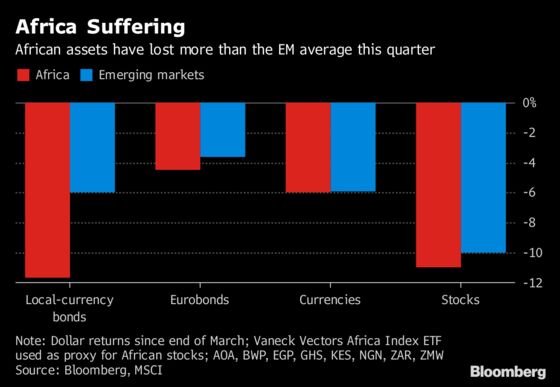

Since the end of March, African Eurobonds, local-currency debt and equities have posted worse returns than those for emerging markets as a whole. Currencies have performed in line with peers, though they’re still down more than 5 percent against the dollar.

Sovereign Debt

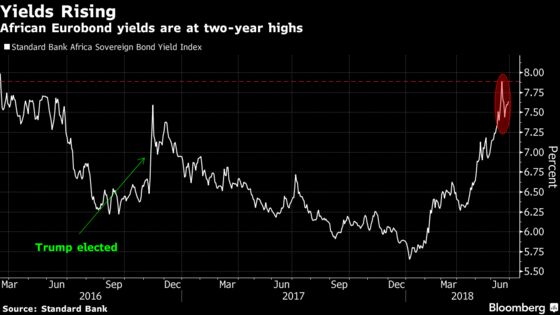

African Eurobond yields are rising more sharply than the emerging-market average. Rates on dollar notes issued by African governments have climbed to 7.6 percent, around 200 basis points above where they were in January, according to Standard Bank Group Ltd. Aside from a brief spike after U.S. President Donald Trump’s election, they’re now at two-year highs.

Oil producers Angola, Cameroon, Gabon and Nigeria have seen their average yields climb above 8 percent, despite rising crude prices. Zambia’s, meanwhile, have soared to more than 11 percent as investors fret that President Edgar Lungu won’t strike a bailout deal with the International Monetary Fund that they think is necessary to ensure his administration can pay off its debts.

Local-Currency Bonds

Global money mangers have also sold local-currency bonds. They are Africa’s worst-performing assets this quarter, with the AFMI Bloomberg African Bond Index, which includes Botswana, Egypt, Ghana, Kenya, Namibia, Nigeria, South Africa and Zambia, losing 12 percent in dollar terms.

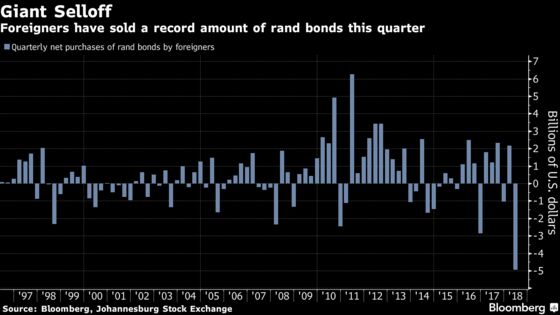

South African securities have been particularly vulnerable, with traders concerned new President Cyril Ramaphosa will struggle to boost growth and ratings companies warning that plans to allow for land expropriation without compensation would deter investment. Rand bonds are the worst-performers in emerging markets this year and foreign investors have sold a net $5 billion of them this quarter, a record amount.

Currencies

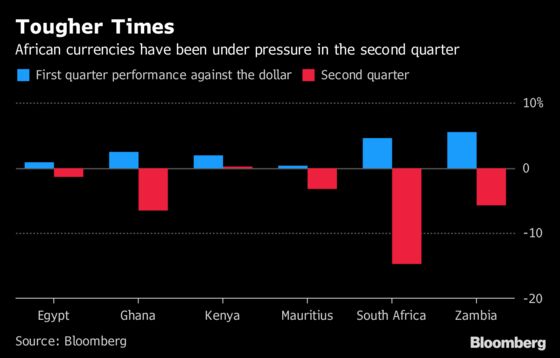

The rand itself has been under pressure too. It’s weakened 14 percent against the dollar since March, more than any other major currency tracked by Bloomberg, and is heading for its worst quarter since September 2011.

It’s far from the only African unit to be suffering. Ghana’s cedi and Zambia’s kwacha are both down more than 5 percent, with the former dropping to a record low this week. Even currencies that are holding up better, such as the Mauritian rupee and Egyptian pound, have pared or reversed gains from the first three months of the year.

Equities

Stocks across the continent have been hit. While none of the major bourses is in a bear market, unlike China’s, which entered one this week, they are heading in that direction. Those in Egypt, Kenya, Morocco, Nigeria and South Africa have all experienced technical corrections, meaning they’re down 10 percent from their 2018 peaks. They’ll be in bear markets if the fall extends to 20 percent.

The only U.S. exchange-traded fund solely tracking Nigerian equities, the Global X MSCI Nigeria ETF, has shed 25 percent of its market capitalization this quarter. The fund hasn’t seen any inflows since Jan. 24 and outflows since then have totaled $25 million. ETF investors are similarly wary of Egypt. The market value of the New York-listed VanEck Vectors Egypt Index ETF has dropped almost 40 percent since mid-April.

The African sell-off may accelerate if growth slows. That may already be happening, according to London-based Capital Economics Ltd.

Some of the biggest economies, including South Africa, Nigeria, Angola, Kenya and Ivory Coast, “stumbled in the first part of the year,” Capital Economics analysts Neil Shearing and John Ashbourne said in a note to clients on June 27. While they expect an improvement later in 2018, “the risks to our growth forecasts now lie to the downside.”

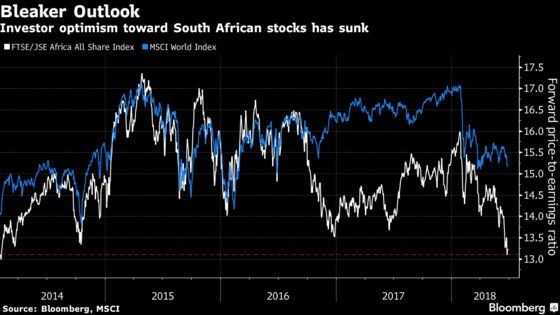

The outlook, for South African equities at least, is significantly bleaker than at the start of the year. The forward price-to-earnings ratio, based on estimates for the next 12 months, of shares on Johannesburg’s main index has fallen to a four-year low of 13.3 from 16 in January. That’s increased the discount investors are demanding versus the MSCI World Index of stocks.

Things could get worse over the next three months if the U.S. and China don’t resolve their dispute, according to Michele Santangelo, director for equity research at Independent Securities in Johannesburg.

“It really does depend on what trajectory those trade discussions go into,” Santangelo said. “I’m hoping it’s a better quarter because it’s been a very difficult year if you look at the numbers across the board.”

--With assistance from Thembisile Dzonzi.

To contact the reporter on this story: Paul Wallace in Lagos at pwallace25@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Robert Brand

©2018 Bloomberg L.P.