Kashkari Says Fed Confused About What's Next After Neutral Rates

Minneapolis Fed chief says inflation data don’t support restrictive policy.

(Bloomberg) -- Federal Reserve officials are trying to figure out whether they will need to raise interest rates high enough to slow U.S. economic growth in the coming years, or if they can stop before the higher borrowing costs start to bite, Minneapolis Fed President Neel Kashkari said.

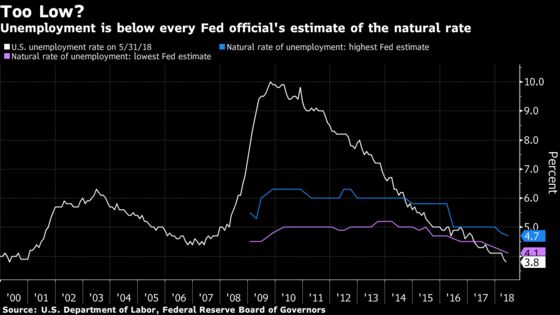

The debate about whether the current level of U.S. unemployment might be too low to keep inflation stable and therefore necessitates tight monetary policy is "a very honest assessment of the confusion" among central bankers at the moment, Kashkari said in an interview airing Thursday on Bloomberg Television.

"I would be comfortable with us moving to a neutral rate -- not stimulating the economy, but not also constraining the economy -- and once we get to neutral, let’s just wait and see how inflation evolves," Kashkari said.

The confusion reflects uncertainty over a relationship between unemployment and inflation that was posited by Milton Friedman in the 1960s and has guided central bankers ever since. The idea is that when the unemployment rate falls below its so-called natural rate, which can’t be observed directly and therefore must be estimated, inflation will accelerate until the unemployment rate goes back up to the natural rate.

It’s the central bank’s job to make the unemployment rate go back up to stabilize inflation if necessary, by raising interest rates above the so-called neutral interest rate, which also must be estimated. The uncertainty -- which has arisen because unemployment has continued to fall without putting much upward pressure on inflation -- is casting doubt on whether that will be necessary.

"Once we get to neutral, are we going to go beyond neutral, and does the data -- does the wage growth, does the inflation data -- actually support moving to a contractionary monetary policy?" Kashkari said. "So far, the data does not support that."

The Fed’s rate-setting committee, on which Kashkari sits but does not have a vote this year, seems like it still believes such tightening will be necessary. The committee raised the trading range for the benchmark federal funds rate after its meeting on June 13, to 1.75 percent to 2 percent. It also published updated projections showing the median participant thought the natural rate of unemployment was 4.5 percent, and the neutral interest rate was between 2.75 percent and 3 percent.

The U.S. unemployment rate fell to 3.8 percent last month. The projections suggest Fed officials think it will be appropriate to raise interest rates above 3 percent next year, which would halt the decline in unemployment and stabilize inflation at 2.1 percent, slightly above the central bank’s 2 percent target.

No Inflation

The Fed committee’s estimate of the natural rate of unemployment has been falling in recent years as the jobless rate has declined without stoking inflation. In January 2012, the committee estimated the natural rate was between 5 percent and 6 percent. At the time, the unemployment rate was 8.3 percent.

Part of the problem, according to Kashkari, is that the estimates may have been too high to begin with, because of how policy makers responded to the 2008-09 recession.

"In a recession, economists tend to raise the natural rate of unemployment -- they think that people get dislocated, skills are mismatched," he said. "And then, only begrudgingly do they lower it. So one conclusion that I’ve already made is, I don’t think it’s useful, in a recession, to ratchet up the natural rate of unemployment, because we’re so reluctant to then lower it, and we end up being late lowering it in recovery."

Kashkari said he’s not ready to believe the natural unemployment rate is really as low as 3.5 percent because that would mark a big departure from historical estimates. But he added that if in the current economic expansion Fed officials do ultimately determine that it is that low, they should avoid raising it when the next recession strikes. That way, they could keep interest rates lower during the subsequent recovery than they otherwise would.

To contact the reporters on this story: Matthew Boesler in New York at mboesler1@bloomberg.net;Joe Weisenthal in New York at jweisenthal@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.