Kuroda’s Right-Hand Man Has Keen Eye on Side Effects of Stimulus

Kuroda’s right-hand man says benefits of BOJ policy exceed the costs so far.

(Bloomberg) -- Bank of Japan Deputy Governor Masayoshi Amamiya is paying close attention to the downside of stimulus after five years of aggressive monetary policy that’s struggling to hold inflation at even half the targeted rate.

But this doesn’t mean any policy relief is imminent for commercial lenders struggling with negative interest rates or bond traders squeezed by the BOJ’s massive purchases of Japanese government debt. Amamiya sees the BOJ as “very far off from the exit.”

“I don’t think the side effects exceed the benefits at this point, but the effects are cumulative and we’re watching this carefully,” Amamiya, 62, said on Monday in his first interview since becoming one of the BOJ’s two deputy governors in March.

The veteran of almost four decades at the central bank declined to comment on the likelihood of any policy tweaks at the next board meeting on July 30-31. Yet he did draw a clear distinction between the current inflation trend in Japan and the situation in 2016, when the last change in policy took place.

With the central bank’s benchmark inflation gauge now at 0.7 percent, Amamiya affirmed the view that "price momentum is basically being maintained." That wasn’t the case in 2016, he said, when the core index was falling. That year Governor Haruhiko Kuroda introduced negative rates and then followed up with a switch in focus from asset purchases to yield-curve control.

While inflation looks better than it did two years ago, it’s still less than halfway to Japan’s 2 percent goal. It leaves the BOJ far from rolling back its extraordinary stimulus while the U.S. Federal Reserve hikes interest rates and the European Central Bank seeks to normalize policy.

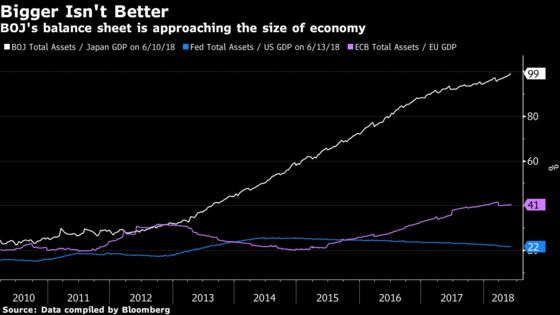

Even after easing the pace of bond purchases, the assets piling up on the BOJ’s balance sheet are likely to surpass the value of Japan’s annual economic output within months.

Despite this, Amamiya said it would be inappropriate to normalize monetary settings early to create policy room for addressing any potential crisis in the future.

He declined to say whether he was comfortable with the view of the majority of private economists that policy tightening won’t come until 2019 or later.

Amamiya indicated that none of this excludes the possibility of tweaks to settings or larger changes, if circumstances warrant, echoing the standard caveat of a central banker.

“The chance of necessary policy adjustments shouldn’t be ruled out,” Amamiya said, speaking in general and not with any particular time in mind. “We have discussions at every monetary policy meeting to make our judgment.”

The negative side effects of BOJ policy have been acutely apparent to traders in the market for Japanese government bonds, where volumes have already been crushed and on occasion 10-year notes go untraded for an entire session. Data released by the BOJ on Wednesday showed it holding 41.8 percent of JGBs at the end of March.

Read more: More quotes from Amamiya’s interview

The nation’s regional banks are also being hurt by the ultra-low interest-rate policy, which is eroding their lending margins, threatening their profitability and providing a challenge to the survival of some.

Amamiya said he’ll keep monitoring the adverse impact of policy on things such as the functioning of banks as intermediaries in the financial system and the operation of price functions in the bond market.

Looking to the July meeting, he repeated the message of Kuroda earlier this month, saying the BOJ would take a hard look at the current level of inflation.

“We always try to examine economic and price conditions at each policy meeting but we will deepen analysis and discussions once again considering price developments so far this year,” he said.

--With assistance from Russell Ward, Gareth Allan and Yuko Takeo.

To contact the reporters on this story: Toru Fujioka in Tokyo at tfujioka1@bloomberg.net;Masahiro Hidaka in Tokyo at mhidaka@bloomberg.net

To contact the editors responsible for this story: Brett Miller at bmiller30@bloomberg.net, Henry Hoenig

©2018 Bloomberg L.P.