India's Life-Saving Plan for IDBI Makes No Sense

New proposal is for LIC to take roughly half of government’s 81 percent stake to become the majority shareholder.

(Bloomberg Opinion) -- Rescuing a dying bank with taxpayers’ money is often the only way to prevent a costlier contagion. But nursing a deposit-taking institution by tapping life-insurance premiums of policyholders? That’s like allowing a localized infection to spread all over, hoping the natural immunity of an otherwise healthy body will help beat back the germs.

India’s plan to sell a majority stake in IDBI Bank Ltd. to Life Insurance Corp. of India is not modern medicine. It’s bureaucratic quackery. New Delhi hasn't found a genuine private-sector buyer for the ailing IDBI for more than two years. Hence, the stage is being cleared for state-owned LIC, the government’s preferred buyer of stuff nobody wants.

If LIC cares about its fiduciary responsibility to policyholders, it will pass this one up. But then, it can never say no to New Delhi. LIC already owns about 11 percent of IDBI, thanks to its previous participation in rescue missions. The new proposal is for it to take roughly half of the government’s 81 percent interest to become the majority shareholder. It could cost LIC around $3 billion to pay the government and top up IDBI’s capital for one year.

That’s money down the drain.

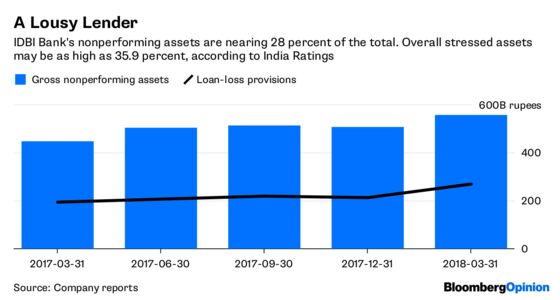

At more than $8 billion, the bank’s gross nonperforming assets are nearing 28 percent of the total. If all IDBI’s distressed loans currently classified as standard assets have to be marked down, NPAs would rise to almost 36 percent, in India Ratings & Research Pvt.’s assessment.

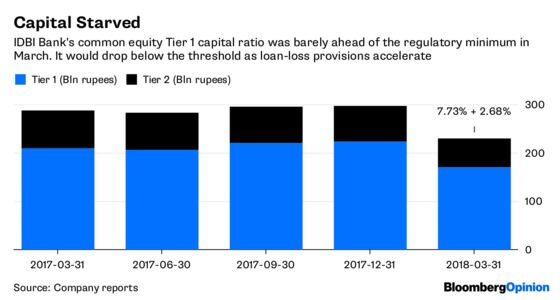

Suppose NPAs do go up, but only to the halfway mark of 32 percent. The math is still stark: A 70 percent loss on 32 percent of the bank’s $29 billion loan book would translate to a $6.5 billion hit, of which only about $4 billion could be absorbed by existing loan-loss provisions. The remaining $2.5 billion would wipe out IDBI’s Tier 1 capital. Whatever price LIC pays for IDBI shares would be too much. Instead of buying from the government, LIC could purchase new stock in IDBI. However, that would dilute minority investors while generating zero cash for the government’s stretched budget.

It’s hard to see how the transaction could bolster the reputation of any of India’s three financial regulators.

Under pressure from the government, the insurance regulator would have to relax the 15 percent cap on a single investment by an insurer; doing so makes sense only when there’s a strong commercial logic. In this case, there is none.

The stock-market regulator would have to exempt LIC from making an open offer to minority shareholders — something it has done before when it allowed state-owned Oil & Natural Gas Corp. to buy New Delhi’s 51 percent interest in Hindustan Petroleum Corp. But overdoing such side deals will make special situations in listed state firms worthless for minority investors, reducing the value of future privatization transactions.

The Reserve Bank of India, the banking regulator, would worry about transmitting the strain of $210 billion in soured corporate loans to the insurance industry’s biggest player. The central bank would also fret about moral hazard.

Alongside IDBI, 10 more Indian state-run banks (out of 21) are facing lending restrictions under the RBI’s so-called “prompt and corrective action” framework; more lenders will likely be forced to shrink. Can all of them hope to be bailed out by LIC? And if after a few decades of growth, demand for life insurance in India declines as it has in the U.S., an eager-to-please LIC might itself need state funds.

It’s doubtful whether IDBI is even worth saving.

The government plowed $1.8 billion of taxpayers’ money into the bank last fiscal year. Yet the lender’s capital position is hovering alarmingly close to the minimum requirement of 7.375 percent. With losses accelerating, IDBI will need plenty more capital just to go on from one day to next. Rather than throw more good money after bad, the central bank should have been allowed to wind up IDBI. If nothing else, it would have set a good precedent. LIC’s customers signed up to protect their own lives — not that of a dying financial institution.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.