Yuan's Rapid Selloff Puts China's Market-Anchor Role in Danger

China’s role as a market anchor at risk with rapid yuan slide.

(Bloomberg) -- An accelerating slump in China’s yuan is stoking fear that policy makers are less willing to temper the currency’s decline as the economy slows and a trade battle with the U.S. worsens.

The yuan is in the unusual position of leading Asian currency declines Wednesday, with a 0.5 percent drop against the dollar. While the People’s Bank of China set the daily onshore reference rate slightly stronger than expected, there was little sign of official moves to halt the slide. The offshore yuan is matching its longest string of daily declines on record.

Just a few weeks ago, the yuan was in effect serving as an anchor for emerging economies facing rising global interest rates and a strengthening dollar. The sharp turnaround has evoked parallels for some to the deliberate devaluation of 2015 that roiled global markets -- though China watchers discount the idea of depreciation being used as a trade-policy tool.

“The yuan now is a source of volatility, not stability,” said Michael Every, head of financial markets research at Rabobank Group in Hong Kong. Further weakness in China’s currency would be expected to “hit the whole emerging-market complex, and to wallop commodity prices,” he said.

The recent sell-off started June 15, a day after a set of soft economic data from China, and deepened along with President Donald Trump’s threat to keep escalating tariff hikes until a potential $450 billion of Chinese shipments are targeted. The onshore rate slumped 0.45 percent to 6.6084 per dollar as of 10:50 a.m. in Shanghai.

“There’s some risk now the depreciation of the yuan may feed back into other dollar-Asia” exchange rates, said Cliff Tan, Hong Kong-based East Asian head of global markets research at MUFG Bank Ltd.

There are fundamental reasons for the yuan’s retreat. Monthly economic data for May showed an unexpectedly sharp slowdown in the world’s No. 2 economy, days after a separate release showed a big drop-off in credit growth. The PBOC also has shifted gears, injecting more liquidity in the economy.

So it’s not clear that the yuan’s drop is down to government direction, according to Zhang Zhiwei, chief China economist at Deutsche Bank AG in Hong Kong.

Self-Harm

"It seems the central bank is willing to let the currency become flexible, but I don’t think they want to have a big devaluation," Zhang said. "China wouldn’t use depreciation actively -- say, guiding the currency lower, or using a one-off devaluation -- as a weapon in the trade war, because it would hurt China as well."

Unlike reciprocal tariff hikes on the U.S. or regulatory moves against American companies operating in China, outright devaluation would be a blunt and multilateral tool that affects all of the nation’s trading partners. The move also could reprise fears of continuous yuan depreciation and capital outflows that were triggered by the abrupt lowering of the yuan’s exchange rate in August 2015. After that episode, policy makers ultimately spent $1 trillion of the country’s foreign-exchange reserves and had to tighten capital controls to stabilize the currency.

The MSCI ACWI Index of global stocks slumped about 12 percent by the end of September 2015, and oil prices halved by early 2016, in part thanks to deepening fears of a China hard landing. President Xi Jinping’s team got an earful of concern about its policies at the time from the global community, from figures including IMF Managing Director Christine Lagarde.

Lesson Learned

“They have learned their lesson,” said Jean-Charles Sambor, deputy head of emerging market debt at BNP Paribas Asset Management in London. “There could be some downward pressure on the RMB, but not a massive depreciation risk, because they know it could change sentiment toward the RMB and trigger additional outflows again,” he said, referring to the renminbi, the official name for China’s currency.

For now the yuan’s resilience is waning compared with its trading partners. The Bloomberg replica of the CFETS RMB Index, which tracks the yuan against a basket of 24 peers, slumped 1.5 percent over the past week. Sue Trinh, head of Asia foreign-exchange strategy at Royal Bank of Canada in Hong Kong, calculates that the drop over the past month reached a two standard-deviation depreciation event -- for only the fourth time since the 2015 devaluation -- earlier this week.

China would be more likely to put a floor under the yuan if talks with the U.S. progress on trade, Trinh says. “In the short term, the yuan’s moves will depend on the trade negotiations,” she said. “In the long term, the depreciation will continue due to slower growth and the policy divergence between China and the U.S.”

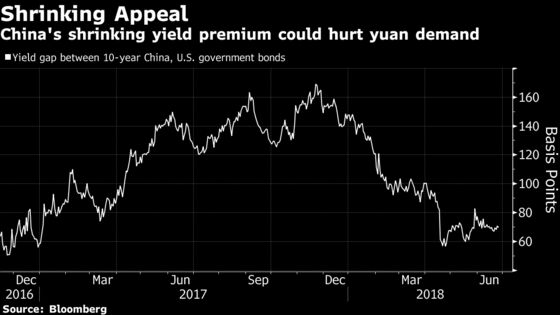

China has some fundamentals in its favor, including a current-account surplus. The largest emerging market is also seeing increasing interest in its domestic securities, now that they are more accessible with inclusion for some of its stocks in MSCI international indexes and the ability of foreign investors to buy bonds via Hong Kong.

Rabobank’s Every sees modest further depreciation this year, with the yuan reaching 6.75 by the end of December -- a drop of a little more than 2 percent. But the latest slide has stoked fears of worse.

Ex-U.S. Treasury official Brad Setser tweeted this week that what worries him is if China decided “it wants a weaker currency to offset the impact of U.S. tariffs on its export and on its economy. And further dollar strength in turn destabilizes other emerging markets.”

--With assistance from Eric Lam.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, ;Richard Frost at rfrost4@bloomberg.net, ;Malcolm Scott at mscott23@bloomberg.net, Jeffrey Black

©2018 Bloomberg L.P.