Central Banks Told Not to Be Afraid of Shaking Markets a Little

Central Banks Told Not to Be Afraid of Shaking Markets a Little

(Bloomberg) -- Central banks should accept that reversing crisis-era monetary policy will be “bumpy” and shouldn’t delay doing so just for fear of upsetting financial markets, according to the Bank for International Settlements.

Claudio Borio, who heads the institution’s economics department, urged policy makers to press ahead, both to address financial stability risks and to insulate their economies against the next downturn. The BIS is effectively a bank for central banks.

“We need to normalize policy and we need to do so with a steady hand,” he said in an interview accompanying the publication of the BIS Annual Report. “By steady hand I mean, in particular, not being afraid of increases in volatility as long as they remain contained: given the initial conditions, volatility spikes are likely to occur along the way.”

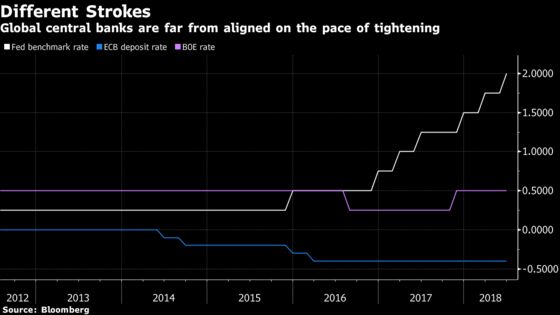

The remarks from Borio, who is known for steering against mainstream thinking, come as the world’s major monetary authorities edge toward more normal policy settings at wildly different paces. The Federal Reserve has raised interest rates seven times since late 2015, the Bank of England once, and the ECB has only just announced it’ll stop bond buying this year, with no rate hikes until after summer 2019. The Bank of Japan is still adding stimulus.

Borio’s view contrasts with comments a week ago by U.S. Treasury Secretary Lawrence Summers, who said central banks should be wary of raising interest rates just to control inflation. In a speech at an ECB conference in Portugal, where he noted his differences with the BIS, Summers said the consequences of another recession any time soon would “massively exceed” the problems of prices running slightly hot.

Read more

|

After venturing into uncharted terrain with trillions of dollars of stimulus -- and in some cases sub-zero interest rates -- to fight the global financial crisis, central banks are in another uncertain situation as they go into reverse.

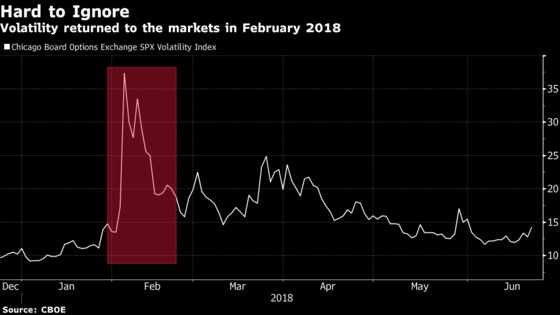

One flashpoint this year was the surge in U.S. yields and spike in volatility in February, sparked by concerns about inflation and faster Fed tightening. The BIS has previously warned about froth in markets from excessive valuations. For Borio, as long as bouts of volatility are contained, they shouldn’t block the path to the exit.

“It is important not to become distracted from the normalization path as long as those wobbles remain contained and don’t have an impact on the real economy,” he said.

Borio has previously questioned the evidence for Summers’ theory of secular stagnation, in which the economy is in a protracted phase of weak growth that would explain low interest rates. The BIS economist has called for an overhaul of thinking on inflation and interest rate-setting in the wake of globalization and digitalization, saying the ability of central banks to fine-tune inflation may have been overestimated.

The BIS, under new leadership since Agustin Carstens became General Manager in December, did acknowledge a “delicate balance” between moving too slowly and too fast. It even noted reasons to support a “very patient strategy,” including high global debt levels and questions over how economies will actually respond to the end of ultra-low rates.

According to Carstens, previously head of the Bank of Mexico, it’s not fair to say central banks brought the challenge on themselves. They were forced into a dramatic post-crisis response because they were “left alone to deal with the problems,” he said.

More from the BIS Annual Economic Report:

|

A decade on, it’s time for change, according to the BIS. Monetary-policy normalization must continue, governments must reduce debt, the financial system must be strengthened more, and structural reforms are needed to support growth without undue inflation pressures.

“The fragility that we see today, on the financial side in particular, is to a considerable extent the result of an economic recovery that has been far too dependent on central banks,” Borio said. “That’s why going forward we need a change in the policy mix.”

To contact the reporter on this story: Catherine Bosley in Zurich at cbosley1@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Paul Gordon

©2018 Bloomberg L.P.