Greece's Creditors Agree to Debt Deal as Payments Eased

The extension will be accompanied by a 10-year grace period in interest and amortization payments on the same loans.

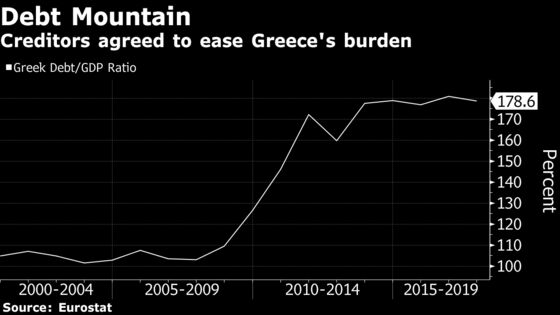

(Bloomberg) -- Greece’s euro-area creditors struck a landmark deal to ease repayment terms on some of the nation’s mountain of debt, clearing the way for the country to exit the lifeline that’s kept it afloat since 2010.

The debt compromise reached in Luxembourg by the bloc’s finance ministers comes after months of acrimonious talks and just as the Mediterranean nation is set to leave its bailout program in August. A deal to ease Greek debt has long been seen as a key ingredient in the country’s successful return to economic health and foray back into financial markets.

An accord was reached in the early hours of the morning as attempts to find a compromise repeatedly hit a wall. The biggest holdout was Germany, which resisted granting Athens more money. In the final compromise, Berlin signed off on a longer maturity extension but managed to limit the tranche of bailout money.

“The deal is good news for Greece and on the optimistic side of what was expected,” said Athanasios Vamvakidis, a strategist at Bank of America Merrill Lynch in London. “Greece buys more time and the debt becomes sustainable, at least on paper. The deal also includes a clear post-program monitoring framework to make sure Greece sticks to the targets. Markets are reassured for now. But it is up to Greece to succeed. Growth is the key.”

Greek bonds rose following the Eurogroup decision, with the yield on its 10-year debt falling 23 basis points to 4.01 percent. The spread over comparable German bonds narrowed to 375 basis points.

Grace Period

Under the agreed debt-relief plan, maturities on 96.6 billion euros ($112 billion) of loans Greece has received from its second bailout would be pushed out by 10 years. The extension will be accompanied by a 10-year grace period in interest and amortization payments on the same loans.

Both these steps are part of a broader package of measures aimed to ensure that Greece will be able to service its debt over the next decades.

“We believe that the debt is now viable, we can have access to the markets now and in a context of surveillance and by continuing our reforms we can pursue this,” Greek Finance Minister Euclid Tsakalotos said after the meeting.

The creditors also agreed to a final disbursement of 15 billion euros, aimed to help Greece repay arrears, finance maturing debt and build up a cash buffer of 24.1 billion euros that will help it access financial markets. Some of that cash could be used to buy back debt it owes to the International Monetary Fund or the European Central Bank, which is more expensive and matures sooner.

In the longer term, euro-area creditors said they could consider measures such as further re-profiling or longer grace periods of loans if needed if economic conditions are unexpectedly worse than anticipated.

Debt Sustainability

“We welcome the Eurogroup’s readiness to consider further debt measures in the long term in case adverse economic developments were to materialize,” European Central Bank President Mario Draghi said. “We believe that the adoption of the set of debt measures agreed by the Eurogroup will improve debt sustainability in the medium term.”

Other agreed debt measures include the return to Athens of some 4 billion euros in profits the euro-area central bank made on their Greek bond holdings and the abolition of a 220 million-euro annual penalty attached to some of the country’s loans.

These measures will be linked to Greece’s performance after the end of its bailout, and will be disbursed in slices over the next four years as long as the country doesn’t stray from its pre-agreed reforms and budget path. As part of the debt deal, Greece is foreseen to maintain a primary surplus -- which excludes interest payments -- worth 2.2 percent of gross domestic product from 2023 until 2060.

Close Monitoring

This means Athens is set to remain under close monitoring by its former bailout auditors, in order to ensure it continues implementing reforms in a small set of areas such as privatizations and the reduction of bad loans.

“We will continue to look at whether the reforms are sticking,” Dutch Finance Minister Wopke Hoekstra said on Friday.

Concerns remain about whether these measures will be enough to revive Greece’s cratered economy, which shrank almost by a quarter during the crisis.

“Under these conditions, Greece is unlikely to achieve fast growth, and therefore will be unable to pay back its debt in full despite a 10-year postponement of maturities granted by the EU,” said Nicholas Economides, professor of Economics at the Stern School of Business at New York University.

Another cause for investor concern may come from the fact that the IMF did not activate its planned lifeline for Greece. The Washington-based fund had repeatedly said it would do so once the country’s euro-area creditors took sufficient steps to ensure its debt remained sustainable in the long term.

Still, the IMF gave its blessing to the debt agreement.

“There is no doubt in our mind that Greece will be in a position to access financial markets,” IMF Managing Director Christine Lagarde said, adding that for the medium term, the agreed measures would ensure Greek debt remained sustainable. “As far as the longer term is concerned, we have reservations.”

--With assistance from Radoslav Tomek, Alessandro Speciale, Sotiris Nikas, Birgit Jennen, Joao Lima, Neil Chatterjee, Richard Bravo and Alexander Weber.

To contact the reporters on this story: Viktoria Dendrinou in Brussels at vdendrinou@bloomberg.net;Nikos Chrysoloras in Brussels at nchrysoloras@bloomberg.net

To contact the editors responsible for this story: Alan Crawford at acrawford6@bloomberg.net, Alessandra Migliaccio, Vidya Root

©2018 Bloomberg L.P.