Easy Money Era Endures Even as Central Banks Unwind Stimulus

Crisis medicine being removed as Fed hikes rates, ECB halts quantitative easing.

(Bloomberg) -- Don’t declare the end of easy money just yet.

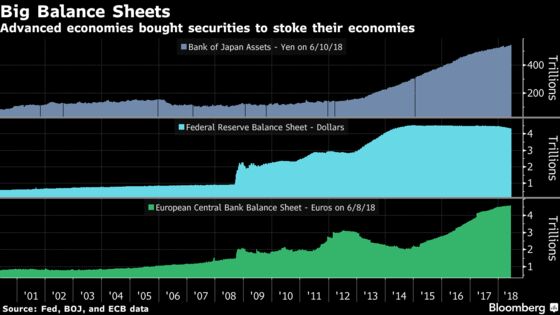

Major central banks took significant steps last week toward dismantling the emergency stimulus they’d used to lubricate financial markets and escape recession in the decade since the financial crisis. But most are clear that they’re not ready to get out of the business of supporting their economies.

After raising interest rates for the second time this year and dropping a longstanding assurance for loose policy, Chairman Jerome Powell and his colleagues described the U.S. Federal Reserve’s stance as accommodative. European Central Bank President Mario Draghi said a decision to halt bond purchases by December would still leave significant monetary stimulus beyond then, especially as euro-zone rates won’t go up before the summer of 2019.

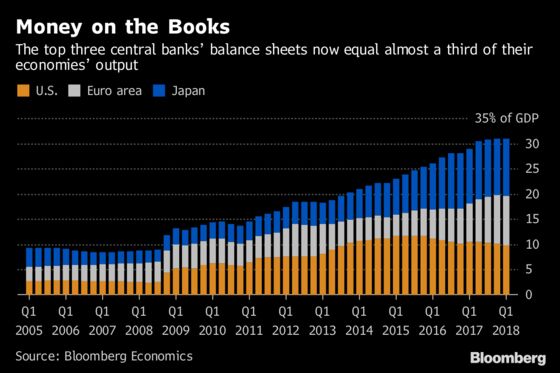

Such commitments mean the loose-money era endures. Bank of America Corp. estimates the combined balance sheet of the world’s biggest central banks is still $11.8 trillion higher than when Lehman Brothers Holdings Inc. collapsed in September 2008, and just short of a $12.3 trillion peak. JPMorgan Chase & Co. economists reckon a gauge of interest rates in the developed world is below 1 percent and won’t be above 1.5 percent a year from now.

“We have seen the peak of easy money, but that doesn’t mean we are going straight to tight money,” said Shane Oliver, head of investment strategy at AMP Capital Investors Ltd. in Sydney.

Perhaps that’s just as well. While the world economy is enjoying its strongest upswing since 2011, International Monetary Fund Managing Director Christine Lagarde warned last week that the clouds are “getting darker by the day.” Even so, Germany’s central bank said on Monday it remained confident that growth in Europe’s largest economy was set for a rebound.

The prospect of a trade war, the constant threat of populism and deteriorating security are already denting confidence, and inflation remains below, or yet to convincingly breach, the targets of leading central banks. Even so, Germany’s central bank said on Monday it remained confident that growth in Europe’s largest economy was set for a rebound.

Moreover, investors have become so used to cheap credit that even a small pullback would carry risks. Recent shifts have already dealt a blow to highly-leveraged companies and emerging markets, partly because the Fed’s decisions pushed up the dollar.

Powell and Draghi will join Bank of Japan Governor Haruhiko Kuroda and Reserve Bank of Australia Governor Philip Lowe on Wednesday in the Portuguese hilltop resort of Sintra for the ECB’s annual forum. The title for the program -- “Price and Wage-Setting in Advanced Economies” -- leaves plenty of room for discussion on how to exit ultra-loose policies.

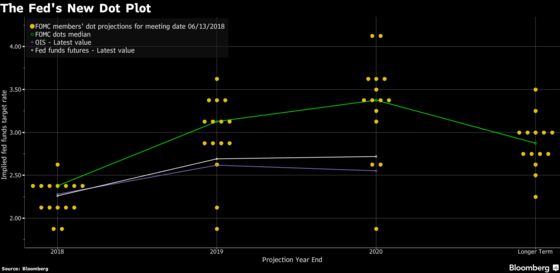

Fed policy makers bumped up their projection for total rate increases this year to four from three. They also pared back their guidance to markets by deleting language that rates were likely to remain below their long-run equilibrium level for “some time.”

Yet Powell told reporters Wednesday that officials will stick with their “patient” plan to gradually normalize policy, even as inflation rises above the 2 percent target and unemployment falls to levels that prevailed in the late 1960s. At 1.75 percent to 2 percent, the Fed’s rate target range is still below officials’ 2.9 percent estimate of the neutral rate that neither spurs nor restricts growth.

“I didn’t get the impression from the press conference that Powell is particularly eager to accelerate the pace of rate increases,” said Roberto Perli, a former Fed official who is now a partner at Cornerstone Macro LLC in Washington.

Long Way Off

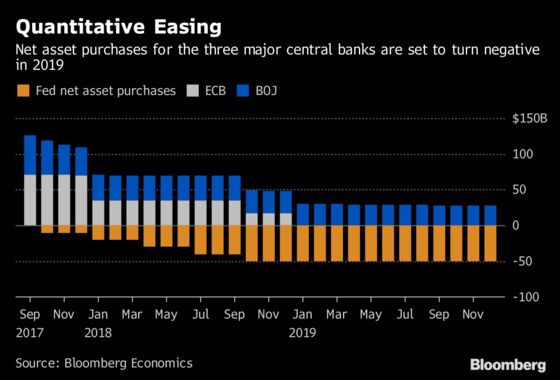

The ECB said its 2.6 trillion-euro ($3 trillion) bond-buying program will be slowed then halted in the final quarter, but surprised investors with its dovish guidance on borrowing costs. It also reminded everyone that the proceeds of maturing assets will be reinvested, meaning it’s far from ready to follow the Fed in shrinking its balance sheet.

“Tapering is certainly not exiting,” said Richard Barwell, an economist at BNP Paribas Asset Management in London. “The ECB is still a year away from raising rates and with confidence in the global growth outlook already fading there is a real risk that they never make it to the exit door.”

What Our Economists Say“The giant stockpile of assets parked on central banks’ balance sheets will provide a bigger impetus to spending as the world returns to normal and neutral interest rates go up. Rather than asset sales knocking the economic expansion off track, the risk may be that policy makers get behind the curve and financial conditions become too loose.”-- Jamie Murray, Bloomberg Economics |

The BOJ knows what it’s like to get stuck. It slipped further behind its global peers last week by leaving its stimulus program unchanged and downgrading its assessment for the current level of inflation. Kuroda said it’s appropriate for Japan to continue “powerful monetary easing persistently.”

The People’s Bank of China also held off amid signs its economy is slowing. Almost two years since the RBA’s last rate move, Lowe said last week that any tightening is far away because of weak wage growth. Russia’s central bank, on the other hand, said on Friday it would slow its transition to a looser monetary policy.

A risk for many central banks is that their rates will still be near or at zero when the next downturn hits, leaving policy makers few options but restarting the printing presses. Draghi said asset purchases will remain a “normal” monetary instrument in the future.

“The best course of action is to err on the side of caution and hike later rather than earlier,” said Gilles Moec, an economist at Bank of America Corp in London. “This also means that they won’t have any buffer if something goes wrong.”

One constraint is the surge in borrowing that has seen global debt balloon to a record $164 trillion, and global public and private debt swell to 225 percent of global gross domestic product in 2016.

“The peak of this global rate hiking cycle will be much lower than in the past,” said Robert Subbaraman, Singapore-based head of emerging markets economics at Nomura Holdings Inc. “Economies are more sensitive to higher interest rates than in the past, and so this rising cost of money may not last that long.”

--With assistance from Zoe Schneeweiss.

To contact the reporters on this story: Enda Curran in Hong Kong at ecurran8@bloomberg.net;Alessandro Speciale in Frankfurt at aspeciale@bloomberg.net;Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Paul Gordon, Alister Bull

©2018 Bloomberg L.P.