Crumbling Curve, Bill Deluge Mean Mnuchin Makes Fed's Job Harder

Crumbling Curve, Bill Deluge Mean Mnuchin Makes Fed's Job Harder

(Bloomberg) -- U.S. debt-management policy is creating ripple effects in financial markets that are complicating the Federal Reserve’s efforts to set interest rates.

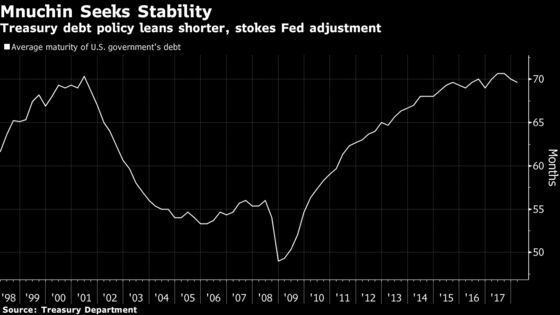

As Treasury Secretary Steven Mnuchin increases issuance to plug swelling budget deficits, the department’s choice of maturities has had some unintended consequences. America’s fiscal stewards have chosen to lean short, ramping up sales of bills and short-dated notes. The approach has created distortions in funding markets that have curbed the Fed’s ability to control its key rate and influenced the debate over the size of its balance sheet.

Bond traders got confirmation of the spillover effect Wednesday, when the central bank tweaked how it engineers rate changes. But the impact goes further: Treasury’s dependence on shorter maturities is speeding the yield curve’s march toward inversion, a phenomenon that has signaled economic downturns. Some investors have speculated the Fed may need to slow the pace of rate hikes to keep that from happening, even as inflation shows signs of accelerating.

“The Fed is having to look at Treasury issuance probably more closely now than they’ve ever had to look at it before,” said Jeff Caughron, chief executive officer at Oklahoma City-based Baker Group, which advises community banks. “They have to be cognizant of the additional complications of issuance. ”

Seeking Stability

The deluge of bills, which peaked last quarter, reverberated worldwide. It buoyed the dollar and pushed central banks from several emerging economies to raise rates or intervene to bolster their currencies. That pressure could re-emerge later this year should Treasury boost bill sales again, as many strategists predict.

Federal deficits, resulting in part from tax cuts and increased spending under President Donald Trump, are driving the issuance needs. But Treasury officials have also decided to stabilize the maturity of the nation’s debt load.

This year, Treasury will likely boost coupon auction sizes for maturities of five years and less by triple the amount of longer maturities, according to JPMorgan Chase & Co. Meanwhile, net sales of bills will amount to $272 billion, rising to $300 billion in 2019 and 2020, according to Morgan Stanley. The tally was $138 billion last year, when the debt ceiling disrupted issuance.

“The last thing we need is more Treasury bills,” said Zoltan Pozsar, an analyst at Credit Suisse Group AG. “Treasury should be stepping away from the bill market,” and funding more with coupon securities, as money markets have struggled to digest the supply.

Here is a breakdown of how the market fallout is making the Fed’s job more difficult:

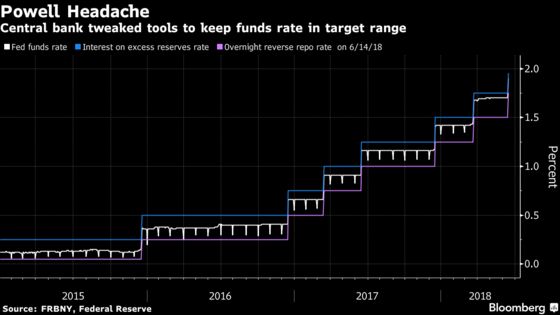

Target Struggle

This week, the Fed raised the upper bound for its benchmark rate by a quarter point, but only increased the rate it pays banks on cash held with it overnight, the IOER, by 0.20 percentage point. Previously, it had lifted the two in lockstep. The intention of the change was to keep the effective funds rate from rising above its target range.

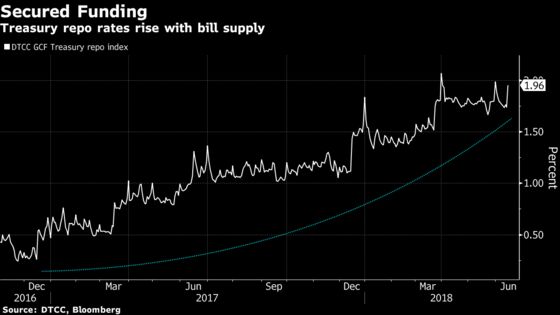

The burst in bill issuance is the prevailing explanation for why the funds rate became unhinged. It pushed key overnight rates higher, especially in the market for repurchase agreements. The rate dealers pay to finance Treasury debt in the repo market rose to 2.07 percent in March, from 1.84 percent at the end of 2017, according to Depository Trust & Clearing Corp. data.

As competing short-term assets became more attractive than lending reserves to other banks, the availability of funding shrank, putting upward pressure on the funds rate. That theory got some buy-in from Fed Chairman Jerome Powell on Wednesday.

“There is a lot of probability just on the idea of high bill supply -- leads to higher repo costs, higher money market rates generally, and the arbitrage pulls up federal funds rate towards IOER,” he told reporters.

In a sign that the Fed’s tweak to IOER was proving effective, the fed funds rate rose to 1.90 percent Thursday, leaving it closer to the midpoint of the target range.

Curve Debate

Measures of the yield curve flattened this week to levels last seen in 2007 after the Fed hiked rates and signaled a faster pace of tightening ahead. The Treasury’s move this year to favor shorter maturities has only stoked the trend, which has dominated the bond market for months.

“Treasury’s decision to fund a little further in on the yield curve may also have limited some of the rise in longer-term interest rates that had been anticipated as a result of the Fed normalizing its balance sheet,” said Michael Feroli, chief U.S. economist at JPMorgan. “I assume Treasury, when they altered issuance, knew it would have some relative effects on markets.”

The recession signal conveyed by the shape of the curve is vexing some officials -- Atlanta Fed President Raphael Bostic said last month that it was his “job” to prevent inversion. Some investors are even pondering the risk that Fed tightening may end the economic recovery sooner than policy makers intend.

“We are going to continue to be talking about” the yield curve, Powell said Wednesday. “Ultimately, what we really care about is what is the appropriate stance of policy and there maybe a signal in the long-term rate on what is the neutral rate. I think that’s why people are paying attention to the yield curve.”

Global Force

If Wall Street is right, the Treasury is going to rev up bill sales again in the second half of the year to finance government operations and account for the Fed’s balance-sheet unwind.

That means global funding markets had better be on notice. Exploding bill issuance was behind the surge in Libor rates to the highest since 2008 in May, which forced some central banks to lift borrowing costs to prevent capital flight.

“The Federal Reserve’s rate hikes this year really only accounted for about 50 percent of the increase we saw in Libor,” said Victoria Fernandez, chief market strategist at Crossmark Global Investments Inc., which manages about $5 billion. “The rest was as a result of the Treasury increasing bill supply.”

So that means monetary policy makers from Riyadh to Sydney have a lot riding on the Treasury’s borrowing deliberations in the months ahead, just as Powell does.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Boris Korby

©2018 Bloomberg L.P.