Fed Day Redux: What Powell Answered and What We Want to Know

From jobs to dots, Powell offered new details on key ideas.

(Bloomberg) -- Jerome Powell gave Federal Reserve-watchers some meaningful answers on Wednesday. He also left them scratching their heads over ever-bigger questions.

The Federal Open Market Committee closed out its June meeting by raising interest rates and suggesting it’ll hike twice more this year, and the Fed chairman announced that he’ll soon start giving press conferences every -- rather than every other -- policy meeting.

Yet if one theme ruled the day, it was an optimistic uncertainty. Unemployment is low, inflation is stable, and the Fed is progressing along its rate-hike path, so policy makers are feeling good. At the same time, they’re unsure where the neutral setting on interest rates sits, how hot the job market is running, and what they’re going to do with the interest on excess reserves rate going forward.

In a reprise to our decision-day preview looking at big questions Powell could answer, here’s a run-down of which ones he did -- and what markets and economists are left wondering.

1. Hot in here?

The Fed lowered its outlook for unemployment this year to 3.6 percent -- down from 3.8 percent in the March Summary of Economic Projections -- and the median estimate now sees 3.5 percent joblessness prevailing in 2019 and 2020. That would take the U.S. to levels last seen in the late 1960s. Despite those near-term projections, policy makers still see 4.5 percent unemployment as the long-run sustainable level.

That’s a sizable overshoot, so it opened up a few key questions. How are we going to get from 3.5 percent unemployment in 2020 to 4.5 percent in the longer run? And why is the near-term moving down without a natural-rate change -- signaling that the job market is running really hot -- while inflation forecasts have barely increased?

Powell had some answers, but they were couched in uncertainty. He said that Fed might find out that longer run unemployment is below 4.5 percent, and noted that higher education levels and an aging population could be lowering the level.

“No one really knows with certainty what the level of the natural rate of unemployment is,” he said. “We can’t be too attached to these unobservable variables.”

2. Knocking on neutral?

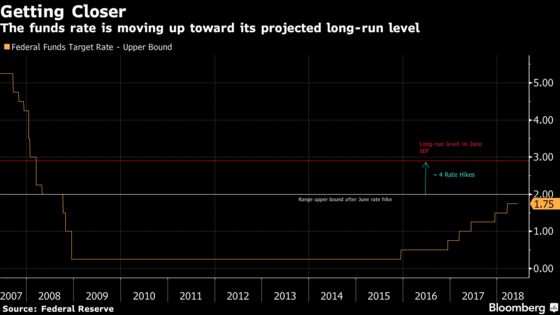

The Fed now projects that it’ll move rates higher than its projected longer-run level in 2019, a year earlier than it’d previously expected to tiptoe past that line. It’s an important barrier to cross, because that long-term estimate is often seen as an approximation of neutral -- the policy setting that neither stokes nor slows growth.

Powell was asked how he and his committee will know when we’re at that neutral level, and how they’ll decide when it’s OK to stop hiking.

“We know that we’re getting closer to that neutral level,” Powell responded. That said, he noted that there’s no “exact sense” of just what that is, emphasizing “wide uncertainty bands” and the importance of being open-minded. “We’ll be very carefully looking at incoming data on inflation, on financial readings, and on the labor market.”

3. Any guidance?

If Powell delivered clear answers in one department, this was it: Fed-watchers learned a lot about his communication plans in June. The committee removed forward-looking language that promised low-for-long interest-rate policy from its post-meeting statement, retiring a significant part of a post-crisis accommodation promise. What’s more, Powell announced that starting in January, he’ll give a press conference after every meeting. The Summary of Economic Projections will remain a quarterly document, he said.

4. Pushing limits?

The effective federal funds rate has been pushing toward the top of its range, which for years has been the level of interest on excess reserves, or IOER. As a result, the Fed on Wednesday announced that it will only move the IOER up 20 basis points -- not the usual 25.

Powell allowed that there could be more to come. “We don’t expect to have to do this often or again, but we’re not sure about that,” he said. “If we have to do it again, we’ll -- we’ll do it again.”

Still, the IOER conversation poses another query for the central bank. It’s not clear exactly what pushed the funds rate up within its range, though it may have been tied to higher Treasury bill issuance. If the move reflected reserve scarcity, it could be a sign that the Fed’s balance sheet unwind is starting to bite -- and that they won’t be able to cut their holdings by as much as they’d expected.

Powell didn’t get asked about this point, and his remarks on the balance sheet reflected the usual Fed line.

“Barring a material and unexpected weakening in the outlook, this program will proceed on schedule,” he said in his press conference opening-remarks.

To contact the reporter on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Randall Woods

©2018 Bloomberg L.P.