India’s Bad Bank Backers Are Badly Wrong

(Bloomberg Opinion) -- Bad ideas keep returning to the corridors of power in New Delhi with the unfailing regularity of migratory birds. This year is no exception. According to media reports, some kind of a state-blessed asset manager to take over the distressed assets of Indian lenders is being considered again.

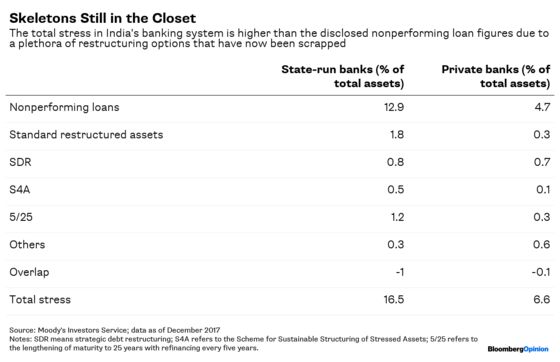

As much as 90 percent of nonperforming assets are with state-run banks. Suppose they’re asked to unload the mess into something like Sareb, the Spanish bad bank whose shareholders include Banco Santander SA and CaixaBank SA, among others. Sareb investors are set to lose 73 percent of their original investment. If the same happens to Indian lenders’ equity, taxpayers might end up paying over and above the $32 billion recapitalization for which they’re already on the hook.

The whole point of having a bad bank is to discover and recover the steady-state economic value of assets that may be currently depressed. In Sareb’s case, the task was relatively easy because boom-bust cycles in real estate – the recipient of Spain’s lending binge – are fairly predictable, certainly more so than the economics of Indian power plants. (About 12 percent of the country’s total power generation capacity is in financial distress.)

Besides, Sareb assumed the loans of savings banks after a 45.6 percent reduction in their carrying value. To compensate the proposed Indian bad bank for under-recovery risk, exposing lenders to a haircut of even 50 percent may not be adequate, according to Jefferies analysts Nilanjan Karfa and Harshit Toshniwal. Given just how capital-starved some of the 21 state-run banks are, having them book steep upfront losses on sales would necessitate immediate consolidation or, in some cases, closure. That would mean taking on powerful unions.

The maneuver makes sense only if unclogging balance sheets restores lenders’ profitability to a point where they can absorb future losses on their bad-bank investment. With a respected former central bank governor saying that confidence in state-controlled lenders is at a historic low, miracles can’t be the base-case scenario.

Besides, for a decisive turnaround, there must be parallel efforts to improve governance, risk management and underwriting standards. The urgency with which politicians and bureaucrats are looking for a solution is directly proportional to the existential threat to India’s government-dominated banking sector. Take away the hanging sword, and the pressure to reform may also ebb.

So why then a bad bank? A year has elapsed, and bankruptcy resolution, which was supposed to take no more than 270 days, has so far been successful with only two large debtors out of an original list of a dozen. Meanwhile, the central bank – the regulator – has taken away lenders’ leeway to extend and pretend. They’re now being forced to make aggressive loan-loss provisions. But where’s the money? Hardening yields are inflicting mark-to-market losses on state-run banks’ outsize holdings of government debt, crimping their ability to climb out of the hole.

A bad bank will buy some time, and give the impression something is being done. With general elections due next year, this looks like a politically expedient proposal of dubious economic merit.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.