The Fed's Fight for Control of Its Key Interest Rate: QuickTake

The Federal Reserve might want to have its rudder adjusted as funds rate threatens to slip outside target range.

(Bloomberg) -- If a ship crossing a wide and placid harbor yaws so far that it almost hits the channel markers, its captain might want to have its rudder adjusted. That’s what the Federal Reserve is considering as the fed funds rate threatens to slip outside the central bank’s target range. The gap between the rate and the Fed’s upper bound has narrowed to a 7-1/2 year low, setting off alarm bells from Washington to Wall Street. It’s also prompted policy makers to discuss whether shifting tides in short-term markets mean they need to change the way they go about manipulating what is arguably the most important interest rate in the world.

1. What’s going on?

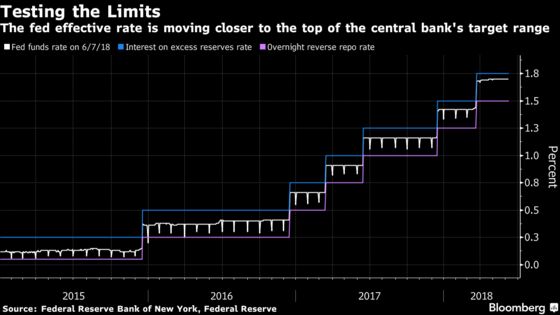

In December 2015, the Fed responded to improving economic conditions by raising interest rates that it had cut to near zero during the financial crisis. It set a target range for the fed funds rate of 0.25 percent to 0.5 percent. Since then it’s increased the range five times, to 1.50 percent to 1.75 percent currently, and is on the cusp of doing so again Wednesday. For most of that time, the effective fed funds rate -- the average of what borrowers in the market actually paid -- rested comfortably near the range’s midpoint, just like it’s supposed to. But since the beginning of the year, fed funds has been creeping higher, now sitting just five basis points below the top of the range at 1.70 percent.

2. What is the fed funds rate?

It’s the rate at which big banks make overnight loans to each other from the reserves they keep on deposit at the Fed. Because it’s the basis for everything from credit card and auto loan rates to certificate of deposit yields, officials use a range of policy tools to exert control over it and thereby influence the direction of the broader economy.

3. How does that work?

Differently than it traditionally did. Before 2008, the Fed used a playbook based on the fact that those reserves were in short supply. If policy makers wanted the fed funds rate to fall, the New York Fed’s Open Markets desk would buy government securities from depository institutions. That increased their reserves, meaning they had more to loan out, which in turn meant lower rates. If it wanted the rate to rise, the desk would sell securities, draining reserves and prompting banks to charge more to lend out what they had left.

4. What about now?

In response to the financial crisis, along with cutting rates, the Fed bought trillions of dollars of bonds in a program known as quantitative easing. It paid for the bonds by creating vast new bank reserves. With all that money on hand, banks had far less need to borrow from each other overnight, meaning that the Fed’s old tools of adding to or reducing reserves had less impact, forcing monetary authorities to come up with another way to influence the effective rate. Enter the interest on excess reserves (IOER) rate.

5. What’s the IOER?

Starting in 2008, Congress allowed the Fed to pay banks for the surplus cash they store at the central bank. As Fed officials prepared for "lift off,” they realized that IOER could be a useful tool for managing rates. In theory, if the fed funds rate were to climb above the IOER rate, firms would withdraw reserves and lend them to other financial institutions at that higher rate. But that increase in the supply of reserves available for loans would then push the fed funds rate back down to the IOER level. Since it began raising rates, the Fed has kept the top of its target range aligned with the IOER. (It created another mechanism, called the overnight reverse repurchase agreement facility, to act as an interest rate floor.)

6. Why is the fed-funds rate rising toward the top of the band?

No one is 100 percent sure. But a prevailing theory, one shared by Fed officials, is that a big burst of Treasury bill sales -- nearly $350 billion in the first quarter, partly to fund tax cuts and a surge in government spending -- flooded an already saturated short-end market, fueling a spike in bill yields. That pushed other key overnight rates higher, especially in the market for repurchase agreements. As these other short-term assets became more attractive alternatives to lending reserves to other banks, the availability of funding lessened, putting upward pressure on the Fed effective rate.

7. Why does this matter?

While the fed effective rate trading a few basis points above IOER wouldn’t be that meaningful, NatWest Markets strategist Blake Gwinn says there’s a credibility concern with the Fed missing a range that’s 25 basis points wide. Fed funds settling above IOER could erode confidence in the central bank’s ability to control interest rates just as bank reserves are beginning to decline and the Fed begins to unwind the balance sheet increases from QE. “They will need this confidence as they eventually start to shift into whatever long-run policy framework” they decide on, Gwinn said. The other issue is that higher rates may indicate that the market is already signaling a scarcity of reserves, which could hinder how much the Fed ultimately decides to shrink its balance sheet.

8. What is the Fed doing about it?

In an effort to nudge the effective rate back toward the middle of their band, officials are mulling lowering the interest on excess reserves rate relative to the upper bound of the fed target range by 5 basis points. With a rate hike all but certain at the conclusion of this week’s policy meeting, that would mean raising the IOER rate by only 20 basis points. Trading in fed funds futures suggests markets now see such a change as likely. It sets the stage for a shift in short-end pricing whether the Fed decides to pull the trigger or not.

9. Will it work?

The Fed obviously thinks so, though they acknowledged in their latest meeting minutes that additional adjustments to the IOER rate could become necessary as the central bank continues to unwind its balance sheet. Others, like Credit Suisse’s Zoltan Pozsar, aren’t so sure. They argue that because the cause of the drift is the result of a glut in short-end supply, only coordination with the Treasury can really solve the problem. Ultimately, if the fed funds rate does continue to creep higher relative to the top of the target band, officials will have to decide if a post-normalization environment requires a new policy framework, or perhaps the return to an old one.

The Reference Shelf

- The minutes of the Federal Open Market Committee’s May policy meeting.

- A roundup of analyst opinions about the Fed’s potential IOER tweak.

- Why the Treasury is responsible for the Fed losing control of overnight rates.

- A Federal Reserve Bank of St. Louis paper, "Interest Rate Control Is More Complicated Than You Thought."

--With assistance from Liz Capo McCormick.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, John O'Neil

©2018 Bloomberg L.P.