China's $11 Trillion Bond Market Tested by Rising Defaults

China’s efforts to connect the bond market with the international financial system are hitting dual headwinds.

(Bloomberg) -- China’s efforts to connect the world’s third-biggest bond market with the international financial system are hitting dual headwinds -- a climb in global borrowing costs, and the country’s own campaign to reduce financial leverage.

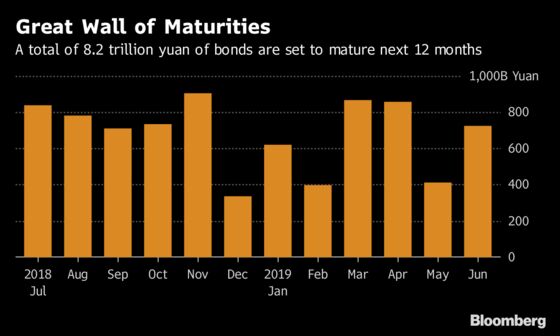

The dynamics have contributed to defaults by 12 bond issuers in 2018 through June 4, after 18 for the whole of 2017, according to Fitch Ratings. Firms from JPMorgan Chase & Co. to Fidelity International are warning to prepare for more. But with about 8.2 trillion yuan ($1.3 trillion) of domestic corporate and local-government securities due to mature in the coming 12 months, it’s an open question whether China is prepared to let chips fall where they may.

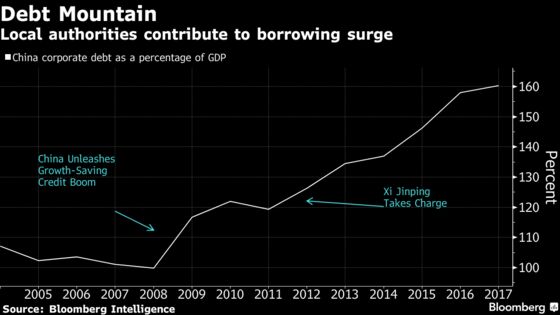

Authorities started shifting away from the old model of implicit guarantees for practically all debt securities in 2014, allowing defaults for the first time. The idea: tap market discipline to punish inefficient companies and encourage a more productive capital allocation. Given the massive size of the market -- now more than $11 trillion, with a further half trillion or so in dollar bonds -- it was always going to be a delicate transition. Where would the lines be drawn on who goes bust? A global-standard credit-ratings industry could hardly be engineered overnight. And who would staff credit-research teams and risk-control desks? Not to mention creating a derivatives market to hedge risks.

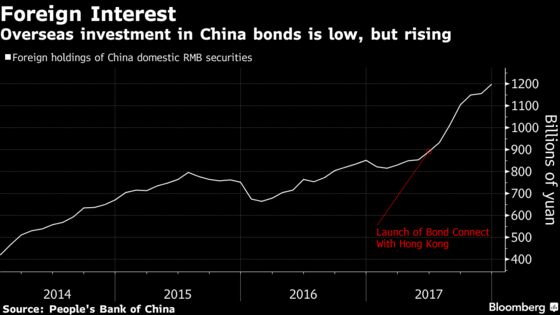

And with China’s door at its most open yet to overseas investors, the global spotlight is shining like never before on these securities.

"The pace is so much faster today, that’s one of the things that’s missed from many investors" looking at China’s capital markets, said Brendan Ahern, chief investment officer at Krane Funds Advisors, which is expanding its line of fixed income products as China’s bond market opens. "If you have to take your eye off China, it moves so quickly that it’s way ahead of you."

As the U.S. Federal Reserve keeps raising interest rates, and China’s monetary overseers pursue a separate campaign to rein in shadow banking, the coming year may prove decisive in shifting investors away from relying on assumptions of state support -- instead forcing them to value bonds based on how likely they are to get their money back.

And about time too, says Ashley Perrott, the Singapore-based head of pan-Asia fixed income at UBS Asset Management. Better differentiation between borrowers based on their risk has been long absent in China.

"It had to happen if they’re going to become a more mature market," Perrott said. Despite its size, the near-absence of defaults in China’s market until relatively recently was one quirk that kept it out of sync with the rest of the world. There are many more that have made it idiosyncratic.

| Read more about China’s bond market: |

|---|

|

Of the defaults so far in 2018, 11 have come from privately owned companies, while one was a state-owned enterprise, Fitch records show. Some investors have been girding for the first-ever delinquency from a local government financing vehicle; LGFVs played a major part in China’s record run-up in debt in the wake of the global financial crisis.

Discerning between companies with explicit guarantees from the government and those with only assumed backing is further complicated by the relative inexperience of many covering it.

"You don’t have the slate of experienced analysts -- you have people with three to five years of experience," said Jamie Grant, head of Asia fixed income at First State Investments in Hong Kong. "There are good credit analysts, but they haven’t been through the Asian credit cycle."

Structural issues with the market have also encompassed concerns about adequate back-office staff to vet trading.

While President Xi Jinping’s administration has made clear the priority of reining in financial leverage -- with moves ranging from pressing financial companies to bring more of their assets on their balance sheets to restricting some of the promises asset managers make to their investors -- policy makers have also been alert to systemic risks.

China in recent months has reduced the amount of cash banks must hold in reserve, and delayed a planned strengthening in oversight of Chinese asset managers. Last week, the central bank said it would accept lower-rated bonds as collateral for one of its lending programs.

Ratings Worries

As for those ratings, though, overseas investors -- who have become increasingly active in the onshore market -- are encountering a system that bears only loose resemblance to the grading structure found elsewhere. Among domestic corporate issuers in China, almost 30 percent have the highest AAA rating, according to data compiled by Bloomberg. That compares with 2.2 percent for bonds in the U.S. covered by the three big global ratings agencies.

Officials have signaled recognition of the discrepancy, last year moving to allow foreign-owned ratings companies to set up their own units in China. Fitch has sold its minority stake in one joint venture. S&P Global Ratings has said it will establish a local subsidiary, while Moody’s Investors Service has yet to announce a formal plan to dive into the domestic Chinese market.

Regulators have also moved on other fronts, including opening the door wider to foreign investors. After allowing qualified institutional investors access in the 2000s, a broader channel opened in July 2017 with the establishment of a "bond connect" with Hong Kong. Moves to include Chinese bonds in international indexes have also put China’s bonds on global radar screens.

Foreign investors say there’s still plenty more architecture to work on, such as expanding access to onshore derivatives, which would let them better hedge interest-rate and currency risks. That would help level the playing field, said Perrott at UBS Asset Management.

Meantime, investors in Chinese borrowers’ dollar bonds are learning some of the particular risks in that market. The latest coming to light is questions about the durability of so-called keepwell provisions -- a commitment to maintain an issuer’s solvency that stops short of a payment guarantee from its parent. Another is use of leverage from as unexpected a place as a provincial toll-road operator that’s taken a page out of hedge funds’ playbook.

With China overhauling its financial overseers earlier this year, prospects may be the best yet for coordinated reforms by the central bank, banking and securities regulators to increase transparency in the country’s debt markets.

"Removing some of these hurdles, so that if you’re a foreign investor you’re dealing with a system that you’re familiar with, then hopefully that will increase the interest," said David Yim, head of debt capital markets in Hong Kong for greater China at Standard Chartered Plc. "It’s going in the right direction, as more and more investors sign up and start trading and buying onshore bonds."

--With assistance from Allen Yan and Eric Lam.

To contact the reporters on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net;Narae Kim in Hong Kong at nkim132@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net;Neha D'silva at ndsilva1@bloomberg.net

©2018 Bloomberg L.P.