A Pyrrhic Victory for Trade Hawks

A Pyrrhic Victory for Trade Hawks

(Bloomberg Opinion) -- The recently announced trade “truce” with China didn’t last long: Unless negotiators led by Commerce Secretary Wilbur Ross reach a breakthrough in talks scheduled for this weekend, tariffs on Chinese exports are set to be finalized on June 15. That’s a victory for the administration’s trade hawks. It’s also a Pyrrhic one: As currently envisioned, the new measures would hurt the very companies they’re ostensibly trying to protect.

The tariffs have two goals -- to reduce America’s trade deficit with China, but also to undermine China’s efforts to gain an advantage in the industries of the future. While specific targets have yet to be confirmed, the administration’s draft list focused heavily on the kind of high-tech exports China is hoping to boost through its industrial policies. The idea is that making those goods and services more expensive will help preserve the competitive edge of U.S. companies -- a lead that’s being eroded by Chinese subsidies, commercial espionage and infringements on U.S. intellectual property.

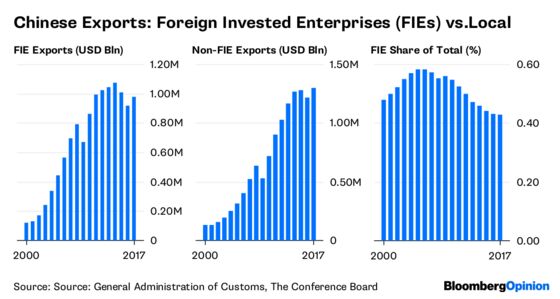

It’s important to understand two things, however. First, U.S. and other foreign companies remain heavily involved in China’s “export machine.” The value of exports produced by foreign-invested companies in China topped $979 billion in 2017 -- a decline from a couple years earlier but hardly an insubstantial sum. Foreign firms account for 43 percent of China’s exports by value and will inevitably suffer alongside their Chinese rivals from any blunt application of tariffs.

Second, while the share of exports produced by Chinese companies has grown from 42 percent in 2005 to the current 57 percent, it remains heavily skewed toward lower-end manufacturing. Chinese companies now produce more than half the country’s furniture exports, for instance -- nearly double the share in 2006. In many cases, foreign companies have moved out of these sectors, relocating factories outside the mainland in search of cheaper labor costs.

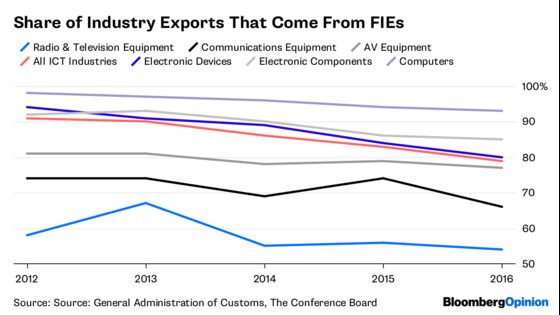

Meanwhile, foreign-invested firms continue to produce the vast majority of exports coming from China’s most cutting-edge manufacturing industries. Companies such as Apple Inc., South Korea’s Samsung Electronics Co. Ltd. and Japan’s Canon Inc. dominate Chinese exports in the information and communications technology (ICT) industry, for example. While their lead has slipped a bit in recent years, foreign companies still command a 79 percent share of the sector overall.

Their share of exports in the most sophisticated sub-sectors is even higher. Foreign-invested companies produce 80 percent of the electronic devices that China exports and 85 percent of the electronic components. They account for a stunning 93 percent of the computers exported from the mainland.

This is where the proposed U.S. tariffs get complicated. The core of the administration’s investigation of China’s trade practices focuses on the Chinese government’s support for domestic businesses in the ICT sector and other industries prioritized by its contentious “Made in China 2025” plan. By targeting exports from these high-tech sectors, the tariffs would punish the biggest players -- many of which happen to be American -- most.

The Made in China 2025 policy is unarguably mercantilist and anti-competitive, and rightly warrants a stern trade and diplomatic response from the U.S. Punishing foreign companies, however, isn’t likely to induce China’s leaders to shift policy.

There are better ways to improve the U.S. trade relationship with China than undermining American companies and firms from other nations aligned with U.S. interests. If the administration wants to respond to China in a way that makes sense, it should double down on efforts to bolster U.S. innovation and competitiveness -- investing more in research and education, attracting more skilled immigrants and seeking to sign trade deals with high-standard protections for intellectual property. It should work with its allies to confront China collectively and ensure a more level playing field for companies operating on the mainland. Above all, it should make sure its own actions don’t make life for those firms any harder than it already is.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

©2018 Bloomberg L.P.