As Fed Loses Control of Overnight Rates, Blame Shifts to T-Bills

Surging Treasury-bill issuance is curbing the Federal Reserve’s ability to control short-end interest rates.

(Bloomberg) -- Surging Treasury-bill issuance is curbing the Federal Reserve’s ability to control short-end interest rates, limiting its capacity to keep the effective fed funds rate within the central bank’s target range, according to Credit Suisse Group AG analyst Zoltan Pozsar.

The Treasury’s nearly $350 billion of bill sales in the first quarter flooded a market already awash in substitutes, from Federal Home Loan Bank discount notes to an expanded foreign repurchase agreement pool and synthetic T-bills via FX swaps, the former U.S. Treasury adviser wrote in a note Wednesday.

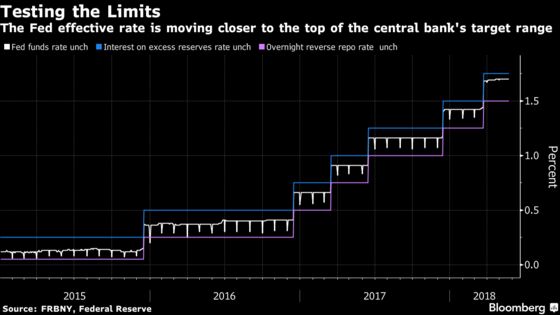

That helped fuel a spike in bill yields, which effectively pushed key overnight rates higher as well. Some are already trading above the Fed’s target range -- currently 1.50 percent to 1.75 percent. The fed funds rate appears poised to follow suit, currently sitting at 1.70 percent.

In an effort to nudge the effective rate back toward the middle of the band, Fed officials are mulling lowering the interest on excess reserves rate relative to the upper bound of the fed funds target range. Pozsar said tweaking the IOER rate, which is currently pegged to the top of the target range, won’t work, and in fact will only hasten a fed funds breakout.

“The Fed should not be doing anything at the moment to cap rates, for the source of the problem is not an insufficient amount of interbank liquidity, but an excessive amount of bills which are being issued in an environment where the world no longer needs them,” Pozsar wrote in the 14th note of a widely followed series he’s published on global money markets.

The diminished appetite for T-bills went unrealized in 2017 because the Treasury was constrained by the debt ceiling. This limited how much the government could issue in short-term securities. Congress passed a debt-ceiling suspension in February that paved the way for the supply deluge.

The glut pushed usage of the Fed’s overnight reverse repo facility to record lows, while T-bills became the effective floor for overnight rates, Pozsar wrote. The rise in bill yields boosted overnight tri-party repo rates to just under the IOER rate, and general collateral financing repo rates outside the target range.

Now that repo rates are trading above the fed funds rate, fed funds volumes are declining, driving the uptick in the Fed effective rate toward the central bank’s upper bound.

No matter the caps the Fed imposes, policy makers may not be able to fix the distortions in short-term rates, according to Pozsar.

“Only the U.S. Treasury can fix this, not the Fed,” he wrote.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Greg Chang

©2018 Bloomberg L.P.