‘Wall of New Money’ Flees Negative Rates for American Credit

U.S. borrowers took advantage of robust demand Monday, issuing $6.75 billion of investment-grade bonds across seven deals.

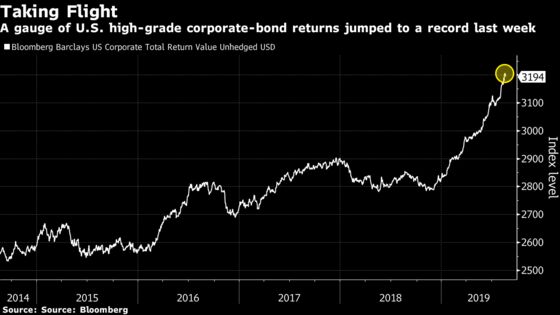

(Bloomberg) -- Blue-chip U.S. companies are likely to see a surge in demand for their bonds as the rising amount of negative-yielding debt globally forces more overseas investors to seek higher returns in dollar assets, according to Bank of America Corp.

Record low yields on global non-dollar investment-grade debt and over $16 trillion of fixed-income assets paying less than 0% should fuel an increase in demand for U.S. credit, strategists led by Hans Mikkelsen wrote in an Aug. 16 note to clients. Attractive currency-hedging costs are helping to offset recent yield compression as offshore investors weigh allocations, according to the report.

“There is a wall of new money being forced into the global corporate bond market,” the analysts wrote. “Given the near extinction of non-USD IG yield, foreign investors are forced to take more risk.”

The average yield on about $27.8 trillion of global non-dollar denominated high-grade debt has plunged to just 11 basis points, while non-dollar sovereign yields are now negative on average for the first time, paying -3 basis points, according to the report.

Read more: CREDIT DAYBOOK: Risk-On Tone Opens Rare Funding Window

U.S. borrowers took advantage of robust demand Monday, issuing $6.75 billion of investment-grade bonds across seven deals in an unusually busy mid-August session. Volume has already passed the low end of dealer estimates projecting $5 billion to $10 billion of new supply this week, led by 3M Co.’s $3.25 billion, four-part offering.

“There’s sizable demand for new issues and the over-subscription level is very notable despite the decline in yields,” said Scott Kimball, a portfolio manager at BMO Global Asset Management. “If you’re looking for generous concessions in new issue investment-grade you’re not going to get it.”

For investors concerned about a U.S. recession, the front-end of the U.S. credit curve is the “best place to hide,” the Bank of America strategists wrote in the report. Still, they noted that they disagree with the market’s recent pricing of a much higher recession probability, and that they prefer to take credit risk further out the curve.

--With assistance from James Crombie and Rizal Tupaz.

To contact the reporter on this story: Caleb Mutua in New York at dmutua@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Boris Korby, Dan Wilchins

©2019 Bloomberg L.P.