(Bloomberg Opinion) -- Donald Trump’s shadow looms large over the world economy.

The U.S. president is presiding over an economic boom in his country that has pushed its unemployment rate to its lowest level in nearly 50 years. It’s not certain that the good times will last, and they may come at the expense of debt sustainability. What’s indisputable, though, is the toll that “Trumponomics” is already taking on other countries.

In its latest World Economic Outlook, the International Monetary Fund has cut its global growth forecast for this year and next by 0.2 percentage points to 3.7 percent. While its prediction for advanced economies was left broadly unchanged, the fund trimmed its 2019 forecast for the U.S. Most important, there was a chunky revision for emerging markets and developing economies. These are now expected to grow by 4.7 percent in 2018 and 2019, respectively 0.2 and 0.4 percentage points lower than forecast in July.

In principle, there’s nothing wrong with a slight deceleration in global growth. The world economy has enjoyed a decent run over the past few years. As central banks start to ease back on cheap money, it’s natural for consumers and companies to become a little more cautious.

The trouble is that the global slowdown looks largely induced by politics. And the prime suspect is Donald Trump and his desire to put “America first.”

The U.S. president has pursued two flagship economic policies since becoming president. One was a mammoth tax cut, which could push his country’s budget deficit to its highest point since 2012. The second is an outwardly aggressive trade policy, including steep tariffs against China and the reworking of agreements with long-standing partners such as Mexico, Canada and the EU.

The full impact on the U.S. economy from all of this will take time to assess. Washington has embarked on fiscal stimulus at a time when unemployment was already very low. While that gives the economy a sugar hit, it’s more prudent to shrink public debt when things are going well.

So far, the attacks on America’s historic friends have turned out to be more noise than meaningful change — as shown by the renegotiation of the North American Free Trade Agreement. Yet the $200 billion in tariffs on China have triggered a range of retaliatory measures, which the IMF says will damage U.S. growth. The fund estimates that U.S. output could end up a full percentage point lower than where it would have been with no new tariffs.

For the rest of the world, the economic consequences of Trump look worse. There’s no sugar rush for the rest of us, temporary or not.

Take, first of all, that fiscal stimulus. It has encouraged the U.S. Federal Reserve to raise interest rates at a steady clip. The risk is that investors will try to guess at future hikes in a disorderly manner. Last Wednesday, the yield on 10-year U.S. Treasuries rose by 12 basis points in a single day, ramping up bets that they will rise further.

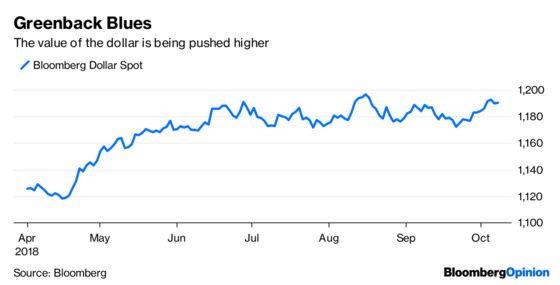

Emerging markets are already bearing the brunt. Higher U.S. rates will persuade investors to move their funds into assets denominated in dollars, which will push up the value of the greenback. The Bloomberg dollar index has risen nearly 7 percent in six months and could increase further.

Meanwhile, the IMF has found that capital flows into emerging markets have weakened significantly since the second quarter. If this rush to the exit continues, it will exert pressure on the frailest emerging markets. Argentina has already had to ask for help from the IMF. More might follow.

The other risk is trade. The economy most at risk is, of course, China itself, whose growth projection for next year has been cut by 0.2 percentage points to 6.2 percent as a result of U.S. tariffs. But the IMF fears a trade war could have a knock-on impact on other developing economies.

It’s unfair, of course, to blame Trump for the woes of specific countries. Turkey and Italy’s problems are entirely self-inflicted. President Recep Tayyip Erdogan has scared off investors by meddling with his central bank. Rome’s populist rulers have spooked markets with their promise to run higher budget deficits.

Still, where once the U.S. would have been a stabilizing force, the opposite is true now. When America comes first, everyone else really is a distant second.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2018 Bloomberg L.P.