Jackson Hole Conference Goes Virtual as the World Passes ‘Peak Central Banking’

Monetary policymakers will hold a virtual Jackson Hole conference this week that will look pale by comparison.

(Bloomberg) -- After convening every August since 1982 at the edge of Wyoming’s magnificent Teton mountain range, monetary policy makers will hold a virtual Jackson Hole conference this week that will look pale by comparison. The same could probably be said of the central banks themselves.

Yes, the Federal Reserve and other monetary authorities have gone to unprecedented lengths to combat the Covid-19 crisis, flooding the global economy with trillions of dollars in liquidity and credit, and in the process have become a towering presence in the financial markets.

But the pandemic has also exposed an unpleasant reality for the monetary mavens: After decades in which they rode high as overseers of the global economy, they no longer have the fire power to manage the business cycle on their own. They need the help of fiscal policy makers to do that –- a fact made painfully clear by the U.S. congressional stalemate over another stimulus package and the threat that poses to the nascent economic recovery.

As former U.S. Treasury Secretary Lawrence Summers provocatively put it in a Princeton University webinar earlier this year: “I sort of suspect that we’re past peak central banking.” Summers is a paid contributor to Bloomberg Television.

Root and Branch

Federal Reserve Chair Jerome Powell is well aware of the pitfalls confronting the central banks in what he described as a new normal of slow global growth, low inflation, and low interest rates at last year’s Jackson Hole symposium. That’s why he launched a root and branch review of the Fed’s policies and practices more than 1 1/2 years ago and why he’s scheduled to deliver an update of how that’s going to the conference on Thursday.

Also speaking at the Jackson Hole event are Bank of England Governor Andrew Bailey and European Central Bank chief economist Philip Lane. Economists and investors are largely expecting both central banks to announce more monetary stimulus before the end of the year, mostly like by boosting their bond-buying programs.

The Fed’s framework review, which is expected to be completed next month, is likely to result in policy makers taking a more relaxed view toward inflation. Indeed, they could well suggest that they’d welcome a temporary, modest rise in inflation above their 2% target after years in which it’s run below that.

Since the Fed introduced the objective in 2012, its preferred measure of inflation has consistently fallen short, averaging just 1.4%.

That’s a vexing problem for the central bank. Combined with low economic growth, it means interest rates have remained historically low. That’s squeezed the Fed’s ability to fight off economic downturns, threatening to make them deeper and longer.

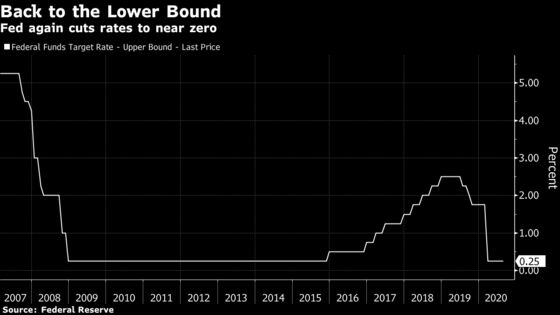

The current, pandemic-induced recession is the perfect example. The lower end of the Fed’s target range for its benchmark rate sat at a mere 1.5% when the crisis struck. Officials promptly slashed it to zero in just two moves in March, but that was nowhere near a sufficient response to the worst downturn since the Great Depression.

Once again the Fed was forced to make massive bond purchases to stabilize markets and push down real borrowing costs. It’s not clear yet how effective those measures will prove.

What’s also in question is whether the subtle changes the Fed is expected to make in targeting inflation will free up enough policy space for it to effectively combat future contractions.

‘Weak Tea’

Former Fed official David Wilcox doubts they will. Calling the likely shifts “pretty weak tea,” the Peterson Institute for International Economics senior fellow said the central bank is “still going to be boxed in” by how far it will be able to lower rates.

Another ex Fed official, Roberto Perli, argued that, if anything, the coronavirus crisis -- and its aftermath -- could make things worse for the central bank. That’s because it will likely prompt households to save more to protect themselves against the economic ravages of another Covid-19-like pandemic. That in turn will put downward pressure on interest rates, leaving the Fed less room to cut them in a recession.

Demographics are also working against the Fed’s effort to carve out more policy space for itself, as an aging population saves more for retirement and a slower-growing work force holds back economic growth.

“The forces holding down interest rates are long-run factors,” said Nomura Chief U.S. Economist Lewis Alexander. “I’m not particularly optimistic those things are going to reverse.”

Turning Japanese

The result, said Perli, who is now a partner at Cornerstone Macro LLC, is that the U.S. could end up looking a lot like Japan. The Bank of Japan has held short-term interest rates around or below zero for more than 11 years. Yet the country is still saddled with a sluggish economy more prone to tipping into a recession and a too-low inflation rate that periodically threatens to morph into deflation.

To fight against that, U.S. fiscal policy makers probably will need to do more to counter declines in the economy. And that was certainly the case early in the Covid-19 crisis, as Democratic and Republican lawmakers –- and President Donald Trump –- agreed on $3 trillion in support for embattled businesses and households.

However, talks on a further stimulus package that economists generally believe is critical for the economy have stalled. Trump has taken action on his own to create an extra $300 per week in unemployment benefits using disaster relief funds, but that may prove difficult to implement and is expected to run out in a matter of weeks.

The theme for this week’s Jackson Hole conference sponsored by the Federal Reserve Bank of Kansas City is “Navigating the Decade Ahead: Implications for Monetary Policy.”

What may well be crucial though is what happens with budgetary policy. If it doesn’t play a bigger role when the economy runs into trouble, “we could look back 10 years from now and find that we’ve been mired in something that looks a lot like Japan,” Wilcox said.

©2020 Bloomberg L.P.