$1 Trillion Task at BOE Is Daunting Ambition for Bailey Era

$1 Trillion Task at BOE Is Daunting Ambition for Era of Bailey

(Bloomberg) -- Andrew Bailey is wagering that the Bank of England can eventually achieve a stimulus withdrawal that neither his predecessors nor his counterparts ever really dreamed was possible.

Only 100 days in office this week, the new governor has already set out a daunting ambition reminiscent of the bold declarations of his predecessor, Mark Carney, by suggesting the institution should ultimately prioritize shrinking its balance sheet before raising interest rates. If that policy ever materializes, it won’t be easy.

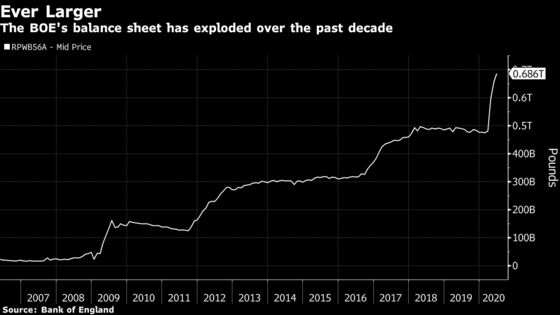

In the BOE’s case, it could mean reverse-engineering a hoard of at least 820 billion pounds ($1 trillion) in loans and assets, mostly U.K. government bonds accumulated through quantitative easing. While Bailey’s concern is that the financial system is relying too much on central-bank funding, the prospect of offloading such debt previously caused policy makers to shirk.

It’s also territory where monetary officials from the euro zone to Japan haven’t ventured, while the Federal Reserve only started to wind down its balance sheet once it was well into a hiking cycle a few years ago, before it ceased shrinking in October.

“This is definitely a departure from what the BOE has guided us toward in the past -- and really how just about every central bank that has engaged in QE or large-scale asset purchases has thought about their exit strategy,” James Athey, Investment Director at Aberdeen Standard Investments, told Bloomberg Television. “It’s going to be very tricky.”

Bailey, writing for Bloomberg Opinion, argued that shrinking the balance sheet would give officials more firepower for a future crisis, while seeking to address the risk that illiquid money-market funds pose to the financial system.

Any move to tighten could be years away if the fallout from the coronavirus crisis keeps the BOE locked into stimulus mode. Like his predecessors, the governor is confronting the challenges posed by exit strategies well in advance, extending a discussion that began almost as soon as the BOE started emergency measures during the global financial crisis.

Exactly a decade ago this month, then-Governor Mervyn King stated that rate hikes would likely come first before gilt sales. Other policy makers musing on the matter since then tended to agree.

Here to Stay

King’s successor, Carney, tended not to shirk from aggressive aims such as achieving “escape velocity” in economic growth or beating the forecasting records of his predecessors. But he too adopted that view, declaring the BOE would bring the benchmark up to 1.5% before offloading assets. Just after he finished his term, the key rate fell to a record-low 0.1%.

In a sign of the times, Andrew Hauser, the bank’s executive director for markets, even acknowledged last year that big central-bank balance sheets are here to stay.

With the economy just coming through the coronavirus slump, and a fresh round of quantitative easing on the way, Bailey will probably have to move backward before going forward with his plan.

The BOE’s own projections foresee inflation remaining well below its 2% goal for the rest of this year, and a return to target in future depends on how the uncertainty surrounding the economy weighs on demand. IHS Markit’s composite Purchasing Managers Index published Tuesday showed economic activity in June rebounded by the most since the survey began in 1998, though it still shrank.

“Bailey will probably never get a chance to tighten himself,” said David Blanchflower, a former BOE policy maker from the era of the financial crisis, who is a professor at Dartmouth College. “The argument that you should be thinking about tightening when there’s no inflation seems bizarre.”

What Bloomberg’s Economists Say...

“It looks like a response to accusations of monetary financing, rather than a switch in the Bank’s favored policy tool. If that’s right, we would expect an early and slow unwind, with rate hikes still on the table when the time comes.”

Dan Hanson and Jamie Rush. Read their BOE INSIGHT

Whereas lifting the benchmark rate boosts yields on bonds of both short and long maturities, unwinding quantitative easing would increase rates on longer-term securities, former BOE policy maker Ian McCafferty speculated in 2017. That could make it more make it more expensive for the government to raise money on debt markets, with political consequences.

Once inflation is strong enough to warrant tightening, selling bonds may have a different impact than simply raising interest rates, he said.

In the Fed’s experience, winding down QE can also create unwanted volatility. In 2013, yields shot higher when authorities said they were considering slowing the pace of purchases. Officials didn’t start reducing the stock of bonds until 2017, and have now had to expand the balance sheet again.

For Bailey, one big concern is the perception that the BOE is doing the government’s bidding as borrowing surges. The bank’s plans to offload debt when the time is right means that won’t happen, the governor stressed in his article.

Doing it gently could take a long time. Citigroup Inc. strategists including Aman Bansal estimate unwinding the amount of extra gilts purchased in 2020 could take as long as eight years if those in its portfolio are simply allowed to mature.

“The governor appears to be making a show of independence relative to both the appetites of the government and the private sector,” Krishna Guha and Ernie Tedeschi, analysts at Evercore ISI, wrote in a report. “But his comments now – when other central banks are emphasizing their intent to stay the course with easing – could lead market participants to question the bank’s staying power.”

©2020 Bloomberg L.P.