(Bloomberg Opinion) -- The Federal Reserve is lending a lot of companies a lot of money. This week the central bank began buying individual corporate bonds, in addition to the bond exchange-traded funds it has bought already. Meanwhile, its Main Street Lending program has begun buying loans that banks make to small and medium-sized businesses at the Fed’s behest. These are in addition to a variety of other lending programs, all designed to keep corporate America afloat until the coronavirus pandemic passes. And there’s evidence that these programs are having the intended effect: there has been no large wave of commercial bankruptcies so far.

But there’s a growing worry in some quarters that all of this lending will create a wave of zombie companies. Zombies are businesses that have to borrow to survive and don’t make enough profit to cover debt-service costs. The number of such companies has been increasing steadily in developed nations during the past 20 years. The reason, presumably, is low interest rates, which allow zombies to sustain themselves on borrowed money rather than exit the market.

Zombies are a problem for two related reasons. First, they tend to be less productive. A company that can survive by borrowing instead of finding ways to increase profits can become complacent and inefficient. A team of economists found in 2018 that as French manufacturers borrowed on increasingly lax terms, they became less productive.

This might not be a problem if other, more efficient companies could pick up the slack. But zombies tend to consume scarce resources -- personnel, office buildings and capital -- and thus leave less for healthy companies. Another research team found in 2018 that in countries with more zombies, the healthy companies grew more slowly.

The most famous site of a zombie outbreak was Japan, where unprofitable companies famously became prevalent after a financial crisis in 1990. A well-known analysis by economists Ricardo Caballero, Takeo Hoshi and Anil Kashyap found that Japanese banks engaged in so-called evergreening of past-due loans to underperforming companies. As expected, industries that experienced more zombification had lower productivity growth, and at the same time financial capital was diverted away from healthy businesses. Other research confirmed the finding.

Now many worry that the U.S., which has already seen creeping zombification, will fall victim to a plague of the corporate living dead in the aftermath of the coronavirus. In a recent interview, for example, Deutsche Bank Chief Economist Torsten Slok acknowledged that the Fed’s lending programs were economically necessary, but worried that they would interfere with the process of creative destruction.

In a healthy economy, bad companies die and good companies replace them and new industries rise while old ones fade. But if the Fed keeps all of the bad companies on life support, neither of those necessary processes can happen. If the moratorium on creative destruction lasts only a year, until Covid-19 is eliminated by treatments or vaccines, the amount of resource misallocation will probably not be too bad. The danger is if unprofitable companies are supported for years.

The pandemic probably will increase the need for creative destruction. Lockdowns and supply-chain disruption will create long-lasting shifts in both consumer and corporate demand that render some businesses and even entire industries unviable. The minute the Fed cuts off the spigot of cheap money, those companies and industries will shed workers and reduce investment, putting the economy in danger. There will be strong political pressure from both elected officials and from the general public to keep corporate borrowing rates low forever.

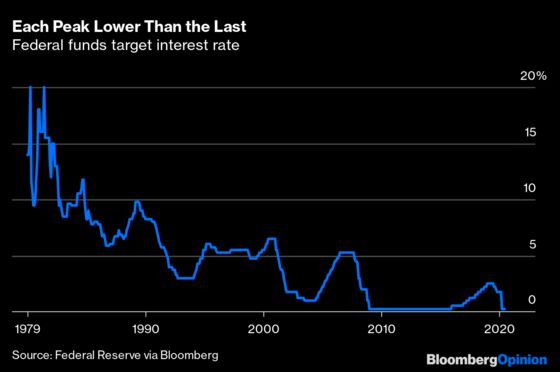

Central bankers might believe that the Fed is strong and independent enough to resist such pressure. In our recent conversation, for example, former Fed chair Ben Bernanke expressed confidence that the end of the pandemic would see the central bank step back and let the market take over. The reality might not prove so easy. Interest rates, for example, have been in decline since the early 1980s, with each peak lower than the last:

That might reflect a slowdown in the economy’s natural rate of interest, but it might also reflect Fed reluctance to cause a new recession by raising rates to the level that preceded the previous downturn. A long-term continuation of the Fed’s pandemic lending programs might, therefore, be seen as a continuation of the long-term reduction in interest rates.

Standard economic theory holds that if the Fed keeps monetary policy too easy for too long, inflation will result. But if easy money reduces productivity growth substantially, that would reduce the natural rate of interest, meaning that continued Fed targeting of low corporate borrowing rates might not cause inflation. The result would then be a new slow-growth equilibrium -- unproductive legacy companies kept afloat on cheap debt provided by a Fed more concerned with short-term politics than long-term productivity.

At this point, all of this is conjecture; until the pandemic is over, the Fed shouldn’t let up on its lending programs. But it would be useful to have a concrete plan for how to clear out the corporate deadwood once the coronavirus is no longer a threat.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2020 Bloomberg L.P.