Yield Seekers Turn to Infrastructure, Real Estate and More

(Bloomberg Opinion) -- European asset managers have spent the past decade watching the returns from fixed-income securities melt away. Famished for yield, they’re increasingly turning to private equity and debt, infrastructure, real estate and other so-called alternative investments. The risks are rising that too much money is chasing too few opportunities.

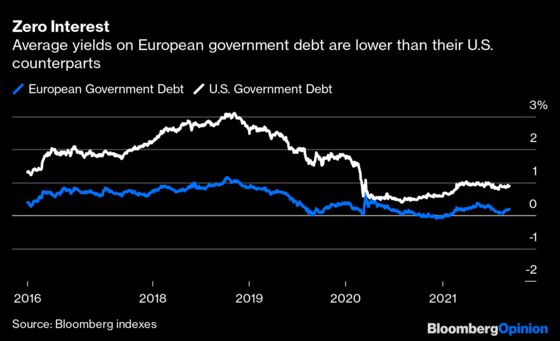

Apart from a brief spike higher as the pandemic shook the world economy in early 2020, the decline in global bond market interest rates has been relentless, with European yields dropping further than their U.S. counterparts. The region’s government debt effectively offers zero in aggregate, with so many benchmarks trading well into negative territory compared with the positive yields still available across the Treasury curve.

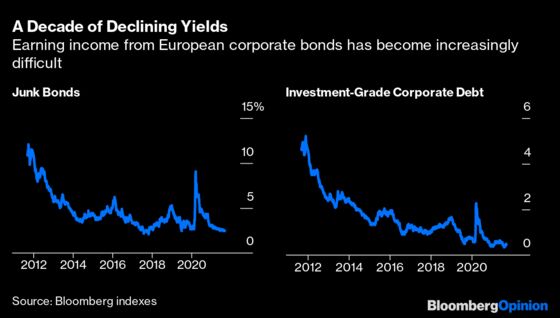

Even buying corporate bonds offers scant relief for European investors, with the income available on debt both above and below the investment-grade ratings threshold shrinking rapidly in recent years. European junk-rated debt yields an average of about 2.4%, for example, compared with 3.7% for sub-investment grade U.S. corporates.

Moreover, the longer the trend of ultra-low yields persists, the more income-starved asset managers become, especially as older, higher-paying debt gets repaid. In the U.K. market, for example, three gilts are scheduled to mature next year worth a combined total of almost 100 billion pounds ($138 billion).

Chris Iggo, chief investment officer at Axa Investment Managers with 866 billion euros ($1 trillion) of assets under management, reckons the weighted average interest rate on those securities is 2.27%. Even if they were all refinanced at current 30-year U.K. government borrowing costs of about 1%, that would reduce the annual income available to bondholders by almost 1.3 billion pounds. Shorter-dated replacements would come with even lower rates.

And with stock indexes across the region at or near record levels, public equity valuations look stretched, to say the least. The benchmark Stoxx Europe 600 index has climbed more than 60% from the low reached in March last year as the pandemic took hold.

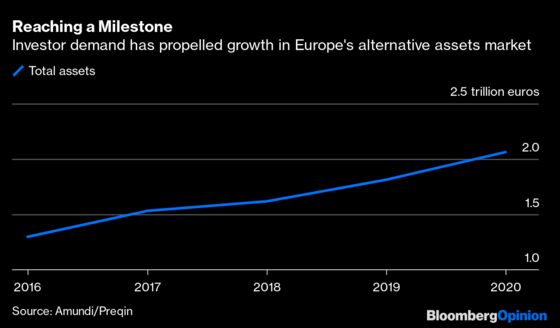

So the motivation for European asset managers increasing their allocations to alternative assets is clear. A report published this week by Amundi SA, Europe’s biggest asset manager overseeing 1.8 trillion euros, and research firm Preqin estimates that the market has enjoyed an annual compound growth rate of 10% in the past five years. That influx of assets has driven the total invested past 2 trillion euros in value. And the market “is on track to make 2021 a record year for fundraising,” the report says.

Private equity and venture capital account for the bulk of the market with 866 billion euros of assets, according to the report. And in the first six months of this year, PE and VC firms raised about 80 billion euros of fresh capital in Europe, contributing about half of the total raised by private capital funds in the region.

Investment in infrastructure, including renewable energy, telecoms, utilities and transport, continues to explode. Completed deals reached 89 billion euros by the middle of this year — easily on track to surpass last year’s total of 90 billion euros.

But that enthusiasm highlights the dangers of too much capital pursuing the same targets.

There is currently 130 billion euros of so-called dry powder, money set aside specifically for infrastructure deals that hasn’t yet been deployed, according to Amundi and Preqin. That’s equal to about half of the total currently deployed in the sector. With so much money seeking investment opportunities, competition is pushing up deal prices.

It’s little surprise that across the private equity universe in Europe, the average purchase price multiple increased to a record last year, according to S&P Global Inc. That will make it harder for transactions to generate outsized returns in the future.

Moreover, with government borrowing costs so low, the private sector faces competition for infrastructure deals from public funding, with nations willing to invest in long-term structural projects deemed to benefit their economies.

Against a low-yield bond backdrop and with equity markets looking frothy, it’s easy to see why fund managers are attracted by the diversification and allegedly higher returns offered by private markets. Dominique Carrel-Billiard, Amundi’s head of alternative assets, reckons the sector could deliver annual returns that are between 2% and 5% better than public markets in the coming decade.

But there are risks. As the pandemic trashed traffic volumes and hobbled energy usage, for example, infrastructure returns collapsed. The report estimates that the one-year internal rate of return for private infrastructure funds slumped to -0.1% by the end of last year, down from an estimated 9.2% return over 10 years.

Asset managers seeking to expand the range of assets they invest in need to tread carefully — and resist being swayed by the fear of missing out.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.