(Bloomberg Opinion) -- Xerox Holdings Corp. is best known for inventing the modern photocopier. When it comes to the company’s $33 billion attempt to acquire HP Inc., Chief Executive Officer John Visentin needs to do more than simply copy and repeat the same terms.

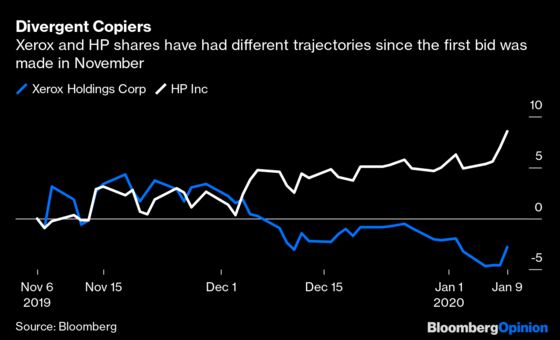

It has been almost two months since larger rival HP rejected Xerox’s initial bid. Since then, little in the substance of the offer has changed. Xerox has assuaged some of HP’s concerns about financing by obtaining bridge loan commitments for the cash part of the bid. But the fundamental offer remains the same: $17 in cash and 0.137 of a Xerox share for each HP share, for a total value of about $22 a share.

Xerox is trying other methods to push a deal through. It has solicited support from HP’s shareholders. Carl Icahn, the activist who’s Xerox’s biggest investor and helped appoint the current board, has taken a stake in HP to build momentum. And, perhaps most significant, the possibility of a proxy fight is looming in which the Xerox camp would submit a slate of directors who are more likely to favor the existing deal terms to replace the current HP board.

The problem with that approach comes down to one factor: time. HP announced a restructuring program in October that will cut as much as 16% of its workforce. The longer a proxy battle endures, the longer HP has to carry out its turnaround plan. If it proves successful, its share price might recover, strengthening the Palo Alto, California-based company’s negotiating position.

So far, HP has refused to engage in formal discussions. Xerox’s priority must be to change that. The first rule of negotiating is usually to create a deal that both parties feel good about. Were Visentin to sweeten the offer and value HP closer to $35 billion, it would give his counterpart at HP, Enrique Lores, reason to come to the negotiating table. After all, his most recent rejection of the Xerox approach focused solely on the price.

How such an increase would be funded is the tricky part. More cash might increase debt beyond investment-grade levels. And even a small bump in the equity component would result in HP shareholders owning the majority of the new entity: Offering 0.18 Xerox share each and the same amount of cash would value HP at $35 billion but give its shareholders 55% ownership. Some version of the latter option seems more viable. HP is by far the bigger company and has previously discussed an acquisition of Xerox.

HP could still decide to buy back stock. Repurchasing 20% of its shares at $23 each would generate just as much short-term value for investors and cost less than $7 billion; HP has plenty of capacity to raise the debt to fund such a move. But Lores has not yet invoked that option, suggesting that he perceives some strategic value in a tie-up. That might give Visentin reason for hope. But to realize it, he needs to dig a little deeper.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2020 Bloomberg L.P.