A Xerox Deal for HP Would Just Be a License to Print Money

(Bloomberg Opinion) -- In what universe can a tiring, $8.8 billion maker of photocopiers even think about acquiring a $27 billion, moderately sexier maker of printers and PCs?

This one, apparently. Xerox Holdings Corp. is contemplating a cash-and-stock bid for HP Inc., the Wall Street Journal reported on Tuesday. While the size of the discrepancy in market values makes a deal seem hard to digest, the capital requirements don’t exceed the realms of possibility. Xerox wouldn’t be buying an exciting new growth business. It would get HP’s cash flow and the ability to reduce costs, probably through significant job cuts.

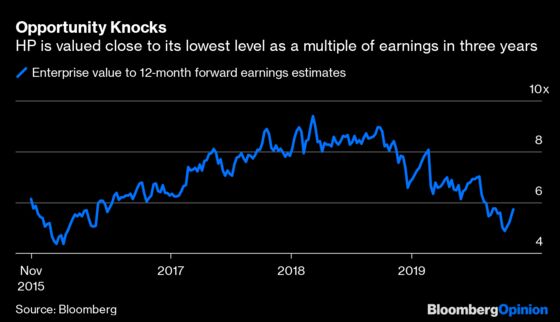

Xerox’s efforts to sell itself appear to have failed. But HP has endured a difficult year, with its stock declining 25% since an October 2018 peak. Its enterprise value is at the lowest level relative to estimated 12-month earnings since 2016. It’s vulnerable to an approach.

Its situation has been exacerbated by operational turbulence. Chief Executive Officer Dion Weisler stepped down at the start of the month for family reasons, announcing a new turnaround plan soon before he left, which successor Enrique Lores inherited. Take into account HP’s relatively low debt and continued ability to generate strong free cash flow, and a bid from Xerox appears entirely feasible.

The smaller company would, in a sense, be buying a license to print more money through HP’s cash flows. Remaining independent is only going to become more difficult, with global printer shipments set to decline by 2% annually through 2023, according to research firm Gartner. Teaming up would reduce costs and competition in the segments where they overlap; HP is generally stronger in the market for smaller printers, while Xerox holds the lead in larger ones. That could boost profitability even as revenue stagnates.

Were Xerox to offer a 30% premium to HP’s average share price over the past 12 months, then a bid in the region of $35 billion might be realistic. Yes, even with a stock component, the required debt pile would be a lot for Xerox to swallow — funding needs could hit $20 billion, according to Bloomberg Intelligence analyst Robert Schiffman. But the merged entity would need to realize savings representing less than 5% of the companies’ combined $9.3 billion annual operating costs to cover the cost of capital, based on 2022 earnings projections.

The Journal reported that Xerox, which is based in Norwalk, Connecticut, had received an informal funding commitment for the deal from a bank, which Bloomberg News identified as Citigroup, citing an unidentified person with knowledge of the matter. Xerox sees room for about $2 billion of annual cost savings from combining the two companies, the person said.

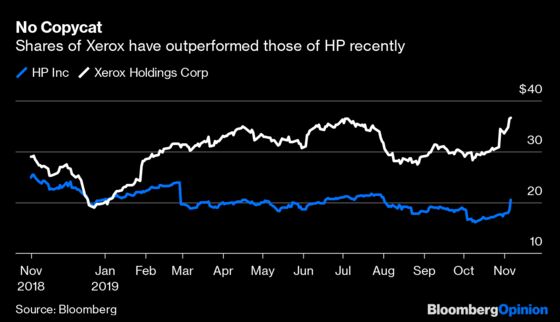

If a bid materializes, credit Xerox CEO John Visentin for thinking big. Since he was appointed last year with the backing of activist investor Carl Icahn, Xerox’s second-biggest shareholder, the stock has outperformed that of HP. News of the possible bid for HP came just hours after Xerox agreed to sell a stake in a lucrative 57-year-old joint venture with Japan’s Fujifilm Holdings Corp. for $2.3 billion.

Would it make sense for HP to do the inverse deal and acquire Xerox? Probably not entirely. It most likely already had the opportunity to do so and passed. But for Xerox, it could prove a canny piece of financial engineering.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.