(Bloomberg Opinion) -- As a rule in life, as soon as someone starts talking about “intangibles,” it’s time to be suspicious. A mediocre athlete who is worth his place on the team because of his intangible qualities should arouse skepticism. So should any company selling the intangible quality of their assets.

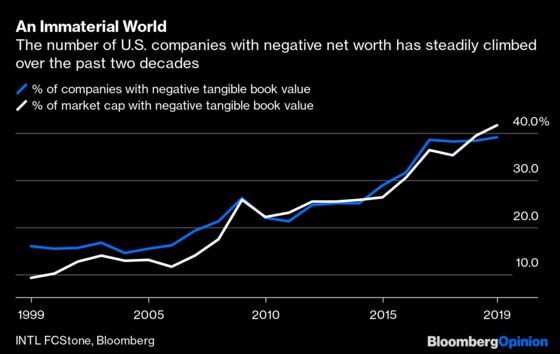

This is a serious problem because the stock market is increasingly populated by intangible companies. Some 40% of public stocks quoted in the U.S. have negative tangible book value, meaning that their tangible assets aren’t worth enough to repay all their debt. Two decades ago, this was only true of 15% of companies, according to Vincent Deluard of INTL FCStone Inc., who has carried out intensive research on the subject.

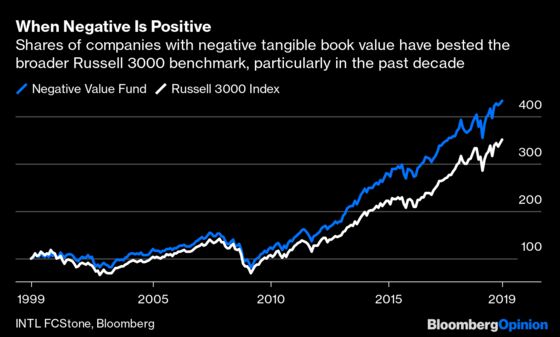

Such companies sound dreadful. In tangible, material terms their share certificates aren’t even worth the paper they are written on. And yet, incredibly, a “negative-value” fund, composed of the shares of companies with negative tangible book value, would have beaten the main U.S. stock market, represented by the Russell 3000 Index, by 24% over the last 20 years. That outperformance has almost all happened since the financial crisis — before that, the negative-value fund had roughly tracked the benchmark.

This seems nuts. Capitalists without capital are ruling capitalism. It also sounds very scary. The U.S. stock market has pleasantly surprised many people by going on a decade-long rally, but the success of the negative-value companies makes it sound as though that success is entirely built on sand. So what can explain this? Deluard offers two popular explanations:

- This is down to rapacious financial engineers and private equity investors who have taken over companies, sold their physical assets and leveraged them to the hilt. Rather than invest in new assets that make something, any new cash flows go toward buying up shares and levering up still further. The entire rally is a triumph of creative accounting.

- The phenomenon is a side effect of the de-materialization of capitalism. Material assets don’t matter as much as they used to do. To believe that, we don’t even need to succumb to airy excitement over the “sharing economy”; in the era of the internet, companies need far fewer physical assets to make a profit. And with rates spectacularly low for a decade, the economic “moat” once provided by factories, retail branch networks or other big physical investments is no longer impregnable. General Electric Co. provides perhaps the most famous and painful example.

To strengthen the notion that this is about the de-materialization of the economy, international comparisons show an east-west divide. In the U.K. and the euro zone, 30% of companies have negative net value, while in China, Japan and South Korea barely any companies do. Increasingly, Asia has become the factory for the world, populated with financially (and physically) sturdy companies, while the U.S. and to a lesser extent of Europe are becoming spirits in an immaterial world.

In practice, these two explanations are not mutually exclusive. Tangible assets are less important, particularly when it is so cheap to finance the purchase of competing financial assets; and it’s true that financial engineers have worked on maximizing earnings per share rather than broader measures of profit. That is clear from the growing discrepancy between the reported earnings of companies in the S&P 500 Index, which kept rising until very recently, and the profits drawn up by the National Income and Profit Account (NIPA) as part of calculating GDP, which have been stagnant for years.

There is perhaps one further explanation that needs to be mentioned:

- It reflects the rise of zombie companies. By these I mean companies that have been around for a long time and are no longer competitive, but can keep staggering forward, zombie-like, because it is so easy to obtain cheap financing.

The Bank of International Settlements is worried by the rise of zombie companies, which it has been charting for years. It defines a zombie broadly as a company whose interest coverage ratio (ICR) has been less than 1 (meaning that it doesn’t produce enough cash to pay its debt payments) for at least three consecutive years and if it is at least 10 years old. This excludes small companies and start-ups that are borrowing heavily to fund a plan for future growth. On this basis, some 12% of companies in the U.S. are now zombies. Less than 2% were in this state three decades ago.

This should be of concern because it suggests that capitalism’s process of creative destruction isn’t working. Zombie companies tend to be less productive than others, so their survival may well be a part of the explanation for the low productivity that has bedeviled the West since the financial crisis.

All of these factors, I believe, are at work in the rise of negative-value companies. In all cases, a return to higher interest rates would bring this group great difficulties. Zombies and companies hollowed out by private equity would face an existential crisis, while we would see how well the new immaterial giants could cope once money had a higher price.

That in turn might help to explain why last year’s moderate rise in interest rates by the Federal Reserve was greeted with a horror, and a market sell-off that prompted a U-turn (and this year’s rally). Investors evidently didn’t want to discover what would happen to negative-value companies once interest rates returned to normal.

Now, the hope must be that they can postpone that moment indefinitely. If that cannot happen, then the time will come when we will all learn a lot more about the true value of intangibles.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2019 Bloomberg L.P.