(Bloomberg Opinion) -- The European Union has successfully circled the wagons with its landmark agreement for 750 billion euros ($859 billion) of grants and loans for those countries requiring pandemic support. That’s excellent news for Italy, which has the biggest sovereign debt in Europe and needed to guarantee its ability to raise finance. In turn, that reinforces the whole euro project by propping up the bloc’s most problematic member.

Any worries that Italy might struggle to fund itself have been dispelled by the recovery fund’s mutually provided arsenal, from which Rome can access 82 billion euros of grants and 129 billion euros of super-cheap loans. The country also expects to secure 25 billion euros of loans from the EU's SURE (emergency unemployment support) program, according to analysts at NatWest Markets.

Prime Minister Giuseppe Conte said on Tuesday that drawing on further credit lines from the EU’s separate bailout fund, the European Stability Mechanism, is “not our objective.” The availability of the new pandemic grants means Italy can pick and choose its most beneficial route for financial support — a luxury it hasn’t experienced in recent times.

Investors in 10-year Italian government bonds have been anticipating this, with yields on this debt having more than halved since they hit a 2.42% peak in mid-March, during the dark early days of lockdown. They are fast approaching 1%. Given Europe’s unprecedented commitment to providing both fiscal and monetary support, there might be further improvement in store. No one wants to allow a sharp increase in the country’s borrowing costs. The record low yields of 80 basis points, last seen in September, are back in sight.

Bond investors are still desperate for any kind of yield, which makes the debt of Italy and Greece attractive, especially if volatility remains modest over the summer. As well as the new EU fund, the European Central Bank has its own 1.35 trillion-euro pandemic program steadily hoovering up bonds.

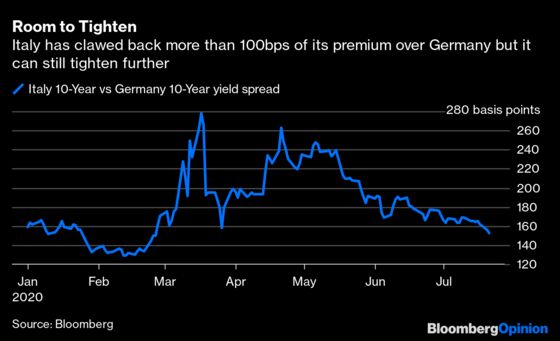

In relative terms, the difference between yields on Italian 10-year bonds and those of their German equivalents has narrowed to its tightest range since late February. This could tighten even further to the 100 basis-point difference last seen in late 2015.

Rome is already nearly three-quarters of the way through its planned bond issuance of 320 billion euros this year. It will persist with this plan as the EU funds don’t kick in until 2021 and they’re spread out over several years. But, as I pointed out in April, its debt load is less terrifying than it first appears, and the nation can certainly keep its cash flow going with all of the assistance available.

Unless the pandemic makes a sudden and unwelcome return, this all bodes well for a relaxed summer. It’s all very different from 2018, when investors sold off Italian debt after the far-right League and the populist Five Star formed a governing coalition. Italian politics are as febrile as ever, but the backing of the country’s European peers no longer looks in doubt.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.