(Bloomberg Opinion) -- The yield on the benchmark 10-year U.S. Treasury note averaged 0.79% from 2007 through last year after adjusting for inflation as measured by the consumer price index. It’s now minus 4.0%. If that’s not shocking enough, corporate bonds rated below investment grade, or junk, yield 4.57%, below the current 5.40% rate of inflation. Something’s got to give. To return to more normal conditions, ether nominal yields must rise or inflation must recede. Bet on the latter.

Since mortgage rates are closely linked to the bond market, enhanced yields would mean trouble for the highly-interest rate-sensitive housing sector. Declining mortgage rates led to a surge in refinancings that last year reached the highest since 2009. Also, the drop in 30-year fixed-rate mortgage rates from 4.45% in the second quarter of 2018 to 3.15% in the first quarter of this year more than offset the surge in house prices, helping to push the National Association of Realtors’ Housing Affordability Index up from 142 to 177.

The problem here is that higher interest rates would squeeze new borrowers and those with floating-rate loans, quickly making housing less affordable. Studies have shown that even a 1 percentage point increase in mortgage rates significantly reduces housing affordability, like in early 2013 and throughout 2017 and 2018.

Furthermore, a jump in rates would be curtains for many high-tech and other stocks whose current lofty valuations are dependent in part on ultra-low rates. The belief is that the equity price today is the discounted value of future profits, and $10 in earnings 10 years from now is worth $9.05 at present with a 1% discounting rate, but only $5.58 at a rate of 6%. Soaring stocks have positively affected the behavior of businesspeople and consumers much like roaring equities in the late 1920, so rising interest rates could have devastating effects not only on the stock market but also on the broader economy.

In contrast to the consensus, I continue to believe the current burst of inflation is transitory, the result of bottlenecks in reopening the economy and supply-chain disruptions spawned by the pandemic. Already, the prices of sensitive commodities are well off their peaks. Lumber is down 71% from its May 7 high. Copper, which goes into almost every manufactured good from machines to vehicles to plumbing fixtures and therefore is an excellent indicator of production, is off 10% from its May 11 top.

In addition, the recent burst of a wide range of prices has not sired inflationary expectations in which buyers anticipate higher goods prices by buying ahead, creating a self-feeding cycle of higher demand straining supply, resulting in even-higher prices. Consumers forced to stay home during the pandemic have largely satiated their demand for many goods, with real, inflation-adjusted spending dropping 0.4% in April from March and 2% in May, as measured by the Commerce Department. Spending on restaurants and other services has risen with the reopening of the economy, but the 0.4% real rise in May didn’t offset the weakness in goods outlays so total personal consumption expenditures were off 0.4% compared to April. Furthermore, services by definition are consumed as produced so hedge buying isn’t possible.

Consumers always overestimate inflation. According to the University of Michigan’s Survey of Consumers in July, they expected inflation five to 10 years from now to run just 2.9%, about the same as in 2014. The Federal Reserve Bank of St. Louis reports financial markets this month anticipate inflation to average 2.16% in the 2026-2031 years. Although up from 1.57% a year ago, it’s down from 3.0% expectations in 2012.

Significant and lasting inflation results from demand for goods and services meaningfully exceeding supply, hardly the case in today’s globalized world. Asian economies are robust producers but frugal spenders. The result is a deflationary saving glut. In China, consumer spending is only 42.5% of gross domestic product, compared with 67.6% in the U.S. And President Joe Biden seems less inclined to limit imports from China than was Donald Trump. Besides, manufacturing for export is moving from China to even-lower-cost countries such as Vietnam.

Rather than sell off in anticipation of rising rates of inflation, the recent rally in long-term Treasuries that has pushed yields lower heralds a weaker economy with less inflation. Treasury bonds started to rally 16 months on average ahead of the six recessions since 1980. Stock performance also led recessions, but the S&P 500 Index turned lower five months on average in anticipation.

I don’t expect a recession in the foreseeable future, but look for slower economic growth in future quarters. U.S. consumers show few signs of spending any more of their fiscal stimulus money then they must. They spent only 29% of their March 2020 checks and saved the rest to build assets and reduce debts, according to the Federal Reserve Bank of New York’s Survey of Consumer Expectations. They spent even less of the December 2020 round, or 26%, and just 25% of their March 2021 money.

Furthermore, consumer spending power is also falling. The recent burst of inflation reduced the real hourly earnings of production workers by 0.6% in June from May. Including the 0.6% decline in the work week, average real weekly earnings fell 1.2%, according to the Bureau of Labor Statistics.

On top of all that, new Covid-19 cases are rising in a number of states as many Americans remain unvaccinated and the highly-transmissible delta variant spreads. So renewed lockdowns are a threat.

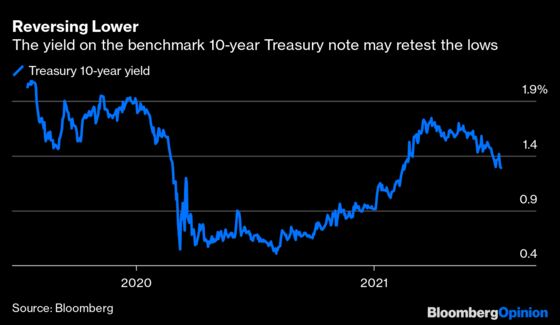

At the height of the 2020 pandemic, yields on 10-year Treasury notes fell to 0.51%, before rising to around 1.30% now. A return to those lower yields is a definite possibility.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

A. Gary Shilling is president of A. Gary Shilling & Co., a New Jersey consultancy, a Registered Investment Advisor and author of “The Age of Deleveraging: Investment Strategies for a Decade of Slow Growth and Deflation.” Some portfolios he manages invest in currencies and commodities.

©2021 Bloomberg L.P.