Will Standard Life Aberdeen Be a Winner or a Zombie?

(Bloomberg Opinion) -- It’s showtime for Keith Skeoch. Almost three years since he and Martin Gilbert agreed to create Standard Life Aberdeen Plc, he’s now flying solo as chief executive officer of the U.K.’s biggest standalone asset manager. For the fund behemoth to be valued by investors and analysts at more than the sum of its parts, it needs to either consistently outperform its benchmarks, or unlock the value of its captive assets — or, better yet, both.

It won’t be easy. The storm engulfing the fund management industry has strengthened since Gilbert’s Aberdeen Asset Management and Skeoch’s Standard Life merged — and the difficulties of combining two different cultures have arguably deterred rivals from seeking similar tie-ups. Customers have withdrawn money in every single quarter since the merger was completed in August 2017, reducing assets under management to 577.5 billion pounds ($753 billion) at the mid-year point, from 670 billion pounds when the deal was completed .

While Skeoch insists that doing the deal was still the right move, the company he oversees is now worth about 7.7 billion pounds, down from 13 billion pounds at the time of the merger.

To be fair, the entire asset-management industry faces tough conditions. The relentless downward pressure on fees for managing other people’s money shows no signs of abating, while the need to invest in information technology has led to an expensive arms race. It’s so dire, according to PGIM CEO David Hunt, that as many as 80% of the industry’s players will become “zombie firms” as the disparity between winners and losers widens.

Standard Life Aberdeen’s shares have rallied 28% this year. But that lags the gains of more than 50% posted by France’s Amundi SA, Europe’s biggest fund manager with 1.6 trillion euros ($1.8 trillion) of assets, and the 33% from Germany’s DWS Group GmbH, which oversees about 750 billion euros.

With U.K. financial assets out of favor with investors for much of this year and domestic investors pulling money out of the stock market, the U.K. firm has fared worse than its competitors in Europe. But its lack of an exchange-traded funds business — DWS ranks second in Europe for ETFs, while Amundi lies fifth — has left Standard Life Aberdeen dependent on active management at a time when customers are shifting more and more money into low-cost passive investment products.

It’s probably too late to build a passive business, while Skeoch’s view that the margins on those products are too low to be attractive makes buying a rival’s unit unlikely. So the firm remains a non-player in originating business in a market that Bloomberg Intelligence estimates has grown by more than 30% this year, reaching 884 billion euros in assets.

Nevertheless, analysts see value in Standard Life Aberdeen, with nine saying its shares are worth buying, nine rating it a hold, with a single sell recommendation.

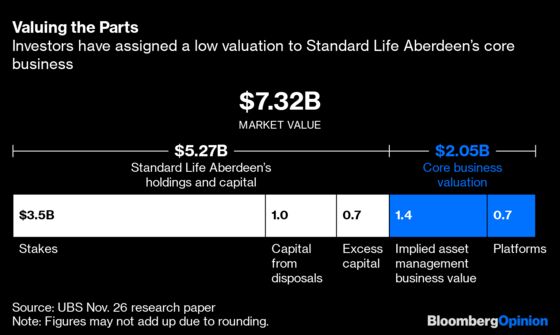

For one thing, it has an unusually large number of stakes in other companies, certainly compared with its asset manager peers. It owns about 20% of Phoenix Group Holdings Plc after selling its insurance business in February 2018, as well as about 15% of HDFC Life Insurance Co. and 27% of HDFC Asset Management, both based in India. In total, those stakes are worth about 5 billion pounds.

Analysts at UBS AG reckon a useful way to value those shareholdings is by calculating how much cash they have the potential to generate, which gives a lower value but still suggests that investors are undervaluing Standard Life Aberdeen’s core competency.

The market capitalization numbers for Standard Life Aberdeen and the three companies it owns chunks of have moved a bit since UBS published that report last month. And, earlier this month, the company proposed raising as much as $380 million by reducing its stake in HDFC AM, as Skeoch makes good on his August promise to “unlock the value of the assets on the balance sheet.”

But the basic premise remains true: The market is assigning a minimal value to Standard Life Aberdeen’s core business.

The pace of asset sales has increased since the arrival of Douglas Flint, who’s been chairman since the start of this year. He was also instrumental in resolving the dual CEO structure: Gilbert told the Daily Mail that he decided to step down to avoid having Flint “tap me on the shoulder and say `come on, it’s time to go.’” He’ll quit the firm altogether next year.

There may be worse to come on the assets front for Skeoch. Analysts at Numis Securities Ltd. estimate that net outflows for this year will approach 80 billion pounds with a further 38 billion pounds set to depart next year, leaving assets under management at 515 billion pounds by the end of 2020 — a far cry from the $1 trillion club that Gilbert was so keen to join.

The key to retaining existing investor funds and luring more customers lies in generating outsize returns. On that front, the merger seems to have been a distraction. In 2018, only half of the firm’s funds were ahead of their benchmarks on a three-year basis. While that had improved to 65% by the middle of this year, just 53% outperformed on a one-year calculation, with 40% lagging their benchmarks over a five-year horizon.

Skeoch, an economist by training, lacks the razzmatazz that Gilbert brought to the party. But his main priority in the coming year will be to galvanize his sales force to stanch those outflows and his portfolio managers to focus on beating the markets — otherwise he, too, may start to fear a tap on the shoulder.

--With assistance from Elaine He.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.