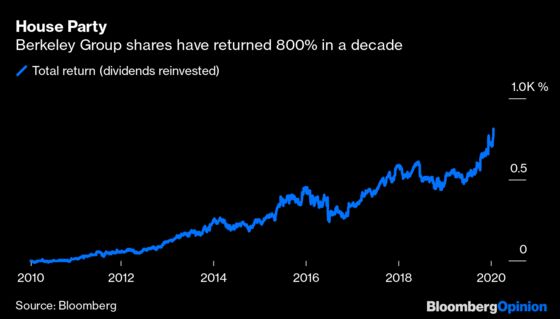

(Bloomberg Opinion) -- Britain’s Berkeley Group Holdings Plc knows all about timing the market right. The homebuilder acquired lots of London land pretty cheaply after the 2008 financial crisis, and made a mint selling apartments once Londoners felt flush again and house prices rose. With dividends reinvested the shares have returned more than 800% over the past decade.

So, when co-founder and chairman Tony Pidgley sold several million shares last year at a time when London house prices were looking decidedly wobbly, it wasn’t an encouraging sign for the market. In total Pidgley has made 216 million pounds ($283 million) from share sales since 2017, including 50 million pounds when Berkeley’s shares popped following Boris Johnson’s thumping U.K. election victory in December. He now owns just 1.3% of the company, according to Bloomberg data.

But perhaps Pidgley’s market timing wasn’t so impeccable after all. Berkeley shares surged another 5% to a record on Wednesday after the builder promised to hike shareholder payouts over the next two years. Had the chairman held onto all of the shares he sold in the past three years, they’d be worth about 300 million pounds today, meaning he’s missed out on 80 million pounds in paper gains.

Doubtless the very wealthy 72-year-old can live with that, but it begs the question of what shareholders know that Pidgley doesn’t. It’s striking that Berkeley’s share price has gained more than 40% over the past year even as it has warned that profits won’t be as impressive as in the past.

At the peak of its financial perfomance in 2018 Berkeley was generating an astonishing 42% return on equity (thanks to all that cheap land it purchased) but it expects this pretax return to normalize to 15% in coming years as it plows cash into developing new sites. In the six months to October 2019, pretax earnings fell almost one-third, as anticipated.

Hence those share price gains have come about principally because investors are now willing to pay more for a slice of its earnings: Berkeley’s stock trades on 16 times estimated earnings, far in excess of the 10 times multiple it has tended to trade at over the past five years, and a big premium to other U.K. homebuilders.

Some optimism is probably warranted. Berkeley has navigated the recent Brexit uncertainty pretty well and it can afford to be more generous to shareholders, having built a more than 1 billion pound net cash buffer. The company’s plans to boost housing output by 50% in the next six years seems reasonable in view of the shortage of supply in south east England.

It’s possible too that the Johnson government’s stable parliamentary majority will boost confidence in the housing market; from a property owners’ point of view that’s a happier outcome than having his hard-left rival Jeremy Corbyn in power.

However, there’s still no clarity about Britain’s future trading relationship with the European Union, nor London’s future prospects as a financial center. At these heady levels, it’s not surprising Pidgley took some money off the table.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2020 Bloomberg L.P.