(Bloomberg Opinion) -- Most investors don’t typically get the opportunity to emulate the strategies of the world’s biggest asset managers. The recent announcement that the Norwegian sovereign wealth fund, the world’s biggest with $1.1 trillion, wants to increase its allocation to North American stocks should be a wake-up call for equity holders who ignore overseas shares — with investors from one nation in particular needing to pay attention.

The tendency for investors to allocate too much of their capital in their home markets is called domestic bias and is a well-known phenomenon. For U.K. investors who’ve stuck with indigenous equities in recent years, this proclivity has cost them dearly.

The U.K. investment industry manages about 8.5 trillion pounds ($11 trillion), more than three-quarters of which is on behalf of local customers, according to figures compiled by the Investment Association, a trade body. For the past five years, the geographical asset allocation of the group has barely budged, and domestic holdings have remained stuck at about 30%, compared with 23% in Europe and 22% or less in North America.

That ignores a significant shift in how important — or unimportant — U.K. stocks are to the global equity market. While British equities have remained the third-biggest geographical component of the MSCI World Index, their share has decreased dramatically, to less than 4.5% from about 7.5% in 2015. That’s even as the contributions of Japan and Switzerland, respectively the second- and fourth-biggest participants, have declined much more modestly.

The big winners have been U.S. stocks, driven by outsized gains in the values of the region’s biggest technology companies in recent years. Hence the Norwegian sovereign wealth fund’s announcement a few weeks ago that it’s been missing out by not having enough of its money in the U.S. market, and intends to shift 6.5% of its equity portfolio — more than $50 billion — to North American stocks.

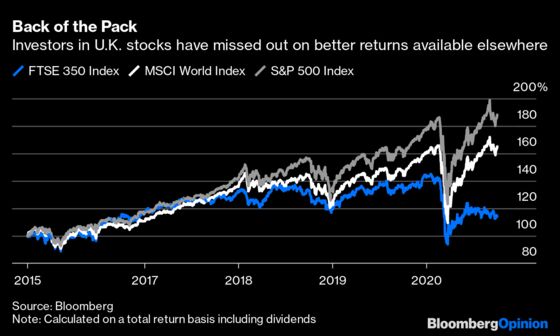

The returns available from U.K. stocks in recent years have also lagged those available elsewhere. Including dividends, the benchmark FTSE 350 index has delivered less than 15% since 2015, compared with more than 60% from the MSCI World Index and more than 80% from the S&P 500 index.

On an annualized basis, that works out at a bit more than 3% for the U.K. market since 2015, below the 13% a year that U.S. stocks have delivered or the 10.4% available from the global stock market index. Investing at home has been a costly bias for U.K. savers.

For U.K. retail investors able to select where to allocate their pension money, there’s a wide range of investment products available to gain exposure to overseas markets, mostly in the form of low-cost exchange-traded funds that seek to replicate benchmark indexes.

Of course, the trend of underperformance by U.K. equities might not continue. But the pandemic has hit the economy harder than that any other Group of Seven nation, which is bad news for British companies that make their money at home. And for firms reliant on overseas sales for profit, the prospect of the U.K. leaving the European Union without a trade deal threatens to make selling to Britain’s biggest export market that much more difficult.

Against that gloomy backdrop, a defensive investment strategy with an increased non-domestic weighting probably makes more sense than the status quo for U.K. investors.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.