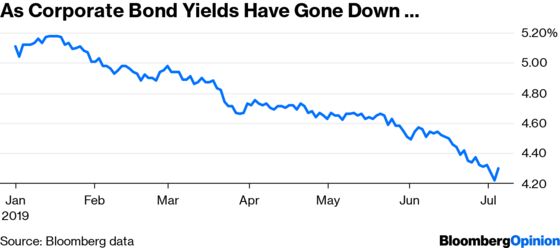

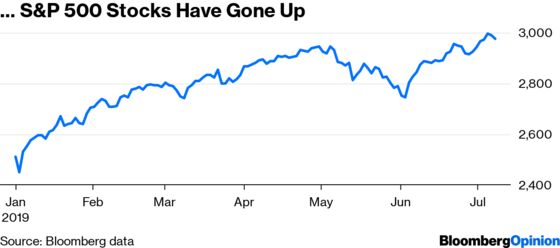

(Bloomberg Opinion) -- Corporate credit markets have bad news for stock investors. Low yields imply that it's going to be tough for stocks to rally much further from here.

Since equities made what was then an all-time high in January 2018, performance of the stock market has largely tracked the movement of investment-grade corporate bond yields. The rise in yields in 2018 acted as a headwind for stocks, with the S&P 500 posting its worst year since 2008. So far this year, the opposite has occurred, with Treasury yields plunging in response to a changed outlook from the Federal Reserve. Stocks have surged as that interest rate pressure has abated, with "low volatility" stocks like consumer staples and utilities doing particularly well. Their performance tends to be tied to interest rates.

The last couple of times corporate yields got this low preceded periods of stock market stagnation. One occurrence was in early February 2015, with yields falling in sympathy with the decline in oil prices. Equities finished the year essentially unchanged. Another instance was in July 2016, shortly after the Brexit vote. Equities drifted lower for the next four months, until just before the U.S. presidential election.

A big factor underlying this thesis is about the prospects for earnings growth. From the fourth quarter of 2014 through the second quarter of 2016 – a period more or less coinciding with the last couple of occurrences of low corporate yields – S&P 500 earnings growth was negative. And over the long run, equities tend to outperform corporate bonds because earnings have tended to grow over time. Without earnings growth, investors would probably prefer the security of bonds to the risk of stocks.

And the problem for today is that earnings growth, after a robust two and a half years, has slowed down significantly. S&P 500 earnings growth was in the low single digits in both the fourth quarter of 2018 and the first quarter of 2019. While earnings growth is projected to pick up significantly in the second half of the year, that seems at odds with broader concerns of slowing global growth and a need for the Federal Reserve to cut interest rates.

If earnings growth does pick up significantly in the second half of the year, then stock performance probably won't be affected by corporate bond yields. But there are plenty of reasons to suspect growth will not pick up. Any slowdown in GDP growth or ratcheting up of the trade war will probably be felt in corporate America's bottom line. Wage growth for employees, now in the low-to-mid 3% range, is about one full percentage point higher than it's been for most of this expansion, which should act as a headwind for profits. It's unclear how much corporations will be willing to take on additional debt to fund earnings growth via stock buybacks or M&A given some concerns about corporate leverage. Companies like Kraft Heinz have gotten bitten by taking on too much debt.

The kind of earnings growth we've gotten over the past few years was either one-off in nature or more difficult to repeat going forward. There was a cyclical upturn in global economic activity that ran from early 2016 through the middle of 2018 that fueled earnings growth. Passage of the Tax Cuts and Jobs Act in early 2018, which lowered corporate tax rates and allowed corporations to repatriate cash from overseas, was a one-off boost for profitability. With those two catalysts behind us, earnings growth may be modest at best, tracking overall economic growth, perhaps with workers getting a bigger share of the pie as the labor market continues to tighten.

And if earnings growth remains modest, stocks may struggle to do more than track the performance of corporate bonds. With yields near their lows of the cycle, that doesn't leave much juice for investors to squeeze.

To contact the editor responsible for this story: Philip Gray at philipgray@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2019 Bloomberg L.P.