What If the U.S. Treasury Stopped Selling 10-Year Notes?

(Bloomberg Opinion) -- Another day, another tantrum in the world’s biggest bond market.

The benchmark 10-year U.S. Treasury yield jumped as much as 11 basis points on Thursday to 1.75%, while the 30-year yield climbed 10 basis points to 2.51%. The fear is palpable among fixed-income investors that the Federal Reserve will truly allow inflation to exceed its 2% target for an extended period before raising interest rates and pumping the brakes on the economy. This isn’t a surprise to anyone who has been paying attention, but nonetheless the central bank’s projections this week hammered home the shift in its monetary-policy framework.

Meanwhile, the Fed showed no interest in some of the more elaborate ideas about how to tame longer-term Treasury yields, such as an “Operation Twist” type effort to reduce purchases of shorter-dated debt and buy more long bonds or outright yield-curve control. This was the right move: Clearly, bond traders across the world are still grappling with the central bank’s new reaction function. In five of the last 16 trading sessions, 10-year yields have increased by more than eight basis points. In the second half of 2020, such a move happened only four times. It’s too risky for the Fed to try to intervene in such volatile markets — failure to tame them would only make things worse.

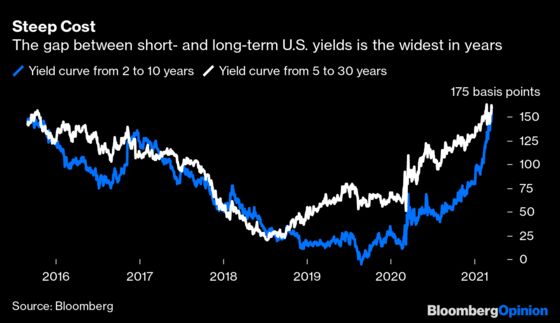

As it stands now, the yield curve from two to 10 years is the steepest since July 2015, at about 159 basis points, while the curve from five to 30 years is 161 basis points, just about the steepest since August 2014. While this is typically a sign that markets expect strong economic growth, it also means that the cost to borrow for decades is now significantly higher than it is to sell shorter-dated debt. That makes sense, given that the Fed has almost total control over front-end rates and reiterated that it’s in no hurry to raise them.

So if investors are fretting about higher long-term yields, and it’s cheaper to borrow with short-dated debt, why doesn’t Treasury Secretary Janet Yellen just stop selling 10-year notes altogether? It would, in effect, be the Treasury Department’s own version of Operation Twist. And it would surely get the attention of bond traders who appear hellbent on raising a ruckus over Fed Chair Jerome Powell’s refusal to give in to their tantrums.

Recent research supports such a move, even if it seems highly unlikely to happen in practice. Martin Ellison from the University of Oxford and Andrew Scott from the London Business School published a report last year that tracked British government bonds dating all the way back to 1694 and found “a substantial cost advantage in favor of issuing short bonds, even when considering some of the operational risks implied by cash flows and gross redemptions.” Matthew C. Klein at Barron’s wrote about this study when it was published, concluding that the only reason it makes sense for Treasury officials to sell long bonds is if they expect much higher and sustained inflation than bond traders. It’s not clear that’s the case.

If that’s not convincing, none other than Milton Friedman has floated a similar notion. In a 1948 paper titled “A Monetary and Fiscal Framework for Economic Stability,” he discussed a proposal in which “government expenditures would be financed entirely by either tax revenues or the creation of money, that is, the issue of non-interest-bearing securities. Government would not issue interest-bearing securities to the public.” This sounds a lot like what Stephanie Kelton would write some 70 years later in her book on Modern Monetary Theory:

“U.S. Treasuries are just interest-bearing dollars. To buy some of those interest-bearing dollars from the government, you first need the government’s currency. We might call the former ‘yellow dollars’ and the latter ‘green dollars’ … what we call government borrowing is nothing more than Uncle Sam allowing people to transform green dollars into interest-bearing yellow dollars.”

It’s not quite such a simple calculation for the Treasury, however. David Beckworth, a senior research fellow at the Mercatus Center of George Mason University and former Treasury Department economist, points to the highly influential Treasury Borrowing Advisory Committee as a reason it would be difficult to move to a short-term only borrowing structure. The group includes executives from Goldman Sachs Group Inc., BlackRock Inc. and Pacific Investment Management Co., among other large banks and money managers. “TBAC says we want this level of maturity,” Beckworth says, “and Treasury is sensitive to the market’s need.”

Certainly, any effort to shorten maturities or do away with long bonds entirely would receive pushback from liability-driven investors like pension funds and insurance companies. But remember, Treasury apparently didn’t find enough demand from these institutions for a 50-year maturity, which is why it settled for bringing back 20-year bonds instead. Besides, any move by the federal government to suspend 10-year or 30-year securities wouldn’t stop investment-grade companies from issuing such debt. State and local governments could also lock in lower borrowing costs with long-term taxable or tax-exempt bonds. It’s not as if all duration would disappear from the financial markets.

To be clear, I don’t expect Yellen’s Treasury would entertain doing away with long-term borrowing entirely. It’s simply too confusing for many people to think of the federal government as anything other than a business that should strive to lock in historically low long-term borrowing costs, even if in reality there’s no reason to think that the world’s largest economy and issuer of the global reserve currency couldn’t just roll over short-term debt time and again. At best, Treasury may consider scaling back its average maturity if yield curves continue to steepen as they have in recent months.

Rather, it’s a reminder that bond traders pushing the 10-year yield higher isn’t some sort of existential crisis. Yes, it’s a global borrowing benchmark and is used as a risk-free rate to value a range of financial assets. But it wouldn’t take all that much for Powell and Yellen to simply turn the entire yield curve into something resembling the overnight rate set by the Fed. With that kind of power, it’s little wonder that they tune out the day-to-day tantrums.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.