(Bloomberg Opinion) -- Some people who trade high-yield corporate debt bristle at the moniker “junk bonds.” It’s definitely a more loaded term than the credit-rating company lingo of “speculative grade” or “non-investment grade,” but it’s a useful shorthand that reminds potential buyers that the securities are not for the faint of heart.

Or, at least, junk bonds used to be considered risky. The way the market has skyrocketed this year, however, it’s worth wondering whether anyone sees the securities — particularly those rated double-B, just below investment grade — as speculative anymore.

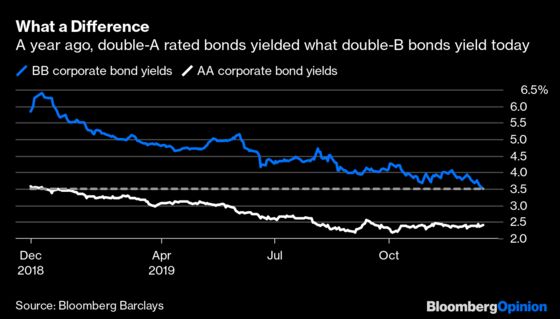

Double-B bonds yielded just 3.51% on Monday, the lowest on record and just 164 basis points more than U.S. Treasuries, Bloomberg Barclays data show. To put those figures further in perspective, just compare them with ultra-safe double-A corporate debt from companies such as Apple Inc., Berkshire Hathaway Inc., Exxon Mobil Corp. and Walmart Inc. Bonds from these kinds of companies had the same 164-basis-point spread to Treasuries at this time eight years ago. And just 13 months ago, the average double-A corporate bond yielded 3.58% — more than you can get now for securities rated nine steps lower.

Of course, a lot has changed since December 2018. Most notably, the Federal Reserve switched from raising interest rates to swiftly cutting them by 75 basis points to keep the economic expansion alive. During a year in which benchmark U.S. yields fell by 100 basis points, it’s hardly surprising that investors have opted to reach for extra returns by taking on more credit risk. Still, the way that double-B bonds have rallied with reckless abandon should make investors a bit nervous.

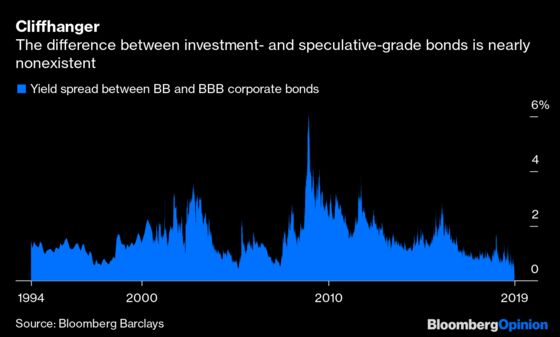

For example, remember that triple-B bond apocalypse that was supposedly right around the corner? You know, the $1 trillion powder keg? As I wrote last month, people are still worried about it, but the market doesn’t show any concern at all. Rather, the difference between double-B and triple-B bond yields is just 38 basis points, the smallest in at least 25 years. Effectively, there’s no “ratings cliff” between investment- and speculative-grade bonds.

Now, I’ve never been a big believer in the triple-B doomsday scenario. But it seems like enough of a risk that it’s worth at least something. The entire narrative revolves around the idea that a bunch of big triple-B companies will become “fallen angels” and get downgraded into the double-B ratings tier, which will cause a glut of high-yield securities, which will force the entire junk-bond market to reprice or else choke on the additional supply.

In an amusing turn of phrase, high-yield fund managers are calling double-B bonds “an up-in-quality trade.” That’s technically true relative to even lower-rated junk bonds, but taking a step back it’s clearly a case of tunnel vision. I don’t blame them, necessarily — they have a mandate to buy speculative-grade securities, and those rated double-B are from the strongest companies within those constraints. Twitter Inc. might be more financially sound than WeWork and Tesla Inc., but that’s not a particularly high hurdle. And yet, it’s enough for the social-media company to issue $700 million of double-B bonds this month at a yield of 3.875%, matching a record low in the high-yield market.

Few, if any, believe this junk-bond bonanza can last. Bloomberg News’s Gowri Gurumurthy reported that Wall Street analysts are forecasting gains of between 1% and 7.5% for U.S. high-yield bonds, down from the 13.5% gain so far this year. Others, like Mohamed El-Erian, are advocating that investors get out of riskier securities while the market is strong.

“What I fear is that this is the prelude to something which is not going to be very comfortable for those investing in the lowest-quality segments of the credit market,” El-Erian, chief economic adviser at Allianz SE and a Bloomberg Opinion columnist, said in a Bloomberg TV interview. “This is the best up-in-quality trade that exists. You don’t give up much yield, and you get a lot more balance-sheet resilience.”

Joe Davis, head of the investment strategy group at Vanguard Group Inc., put it like this: “For savvy investors, the tighter credit spreads become, the more guarded they have to be in their strategy,” he said. “When the next recession hits, the downturn in the financial markets could be worse than the economic effects.”

As always, the tricky part is calling the turn in credit markets. Davis said high-yield bondholders might sees gains of 4.5% to 5% in 2020, in part because there’s only a 25% chance of a recession in the next 12 months. That should be enough to prevent any sort of sustained outflows from junk-bond funds, which can often be what starts the vicious cycle of forced selling, followed by widespread losses and then further withdrawals. It’s common knowledge that chasing returns is not a sound investment strategy, but after a year like 2019, it’s understandably hard to resist the temptation.

The way El-Erian frames the investment decision presents the clearest path forward. The U.S. corporate-bond market is offering a golden opportunity to upgrade double-B bonds to triple-B for the record-low trade-off of 38 basis points. To upgrade to single-A, it’s just 91 basis points, and to double-A, it’s 113 basis points, both near the all-time lows set in June 2007. Every year is full of unknowns and potential pitfalls, and 2020 is no exception. Why not run with investment-grade debt until junk bonds actually pay something that better reflects their additional risk?

The existential question, it seems, is this: What makes a junk bond junk? The typical answer is its heightened credit risk, reflected in the additional yield investors demand to lend the company their money. But that spread has almost evaporated. Now, it could be argued that double-B debt is junk precisely for the opposite reason — because it offers little-to-nothing relative to securities from more creditworthy borrowers.

Don’t let high yield’s big year fool you: At the end of the day, junk bonds are still junk.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.