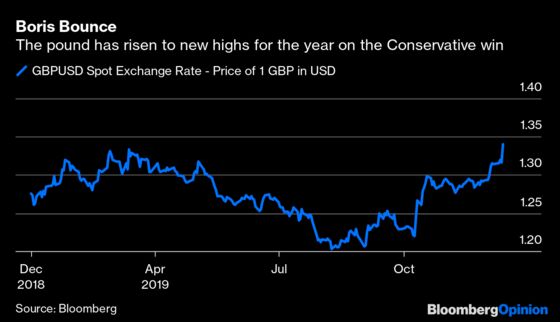

(Bloomberg Opinion) -- Sterling has punched up to new highs for the year on the back of a comprehensive election victory for Boris Johnson’s Conservative Party.

With the parliamentary handbrake on Johnson’s Brexit deal now released — and the trouncing of Jeremy Corbyn’s high-taxing, business-baiting Labour Party delivered with great force — we should see sustained pound gains. Nevertheless, as I outlined earlier this week, quite a lot of this was already priced in because of the Tories’ convincing lead in the polls, so don't expect an immediate return to pre-referendum highs of 2016. The British economy is struggling, whoever is in charge, and growth in the next few quarters will be very modest.

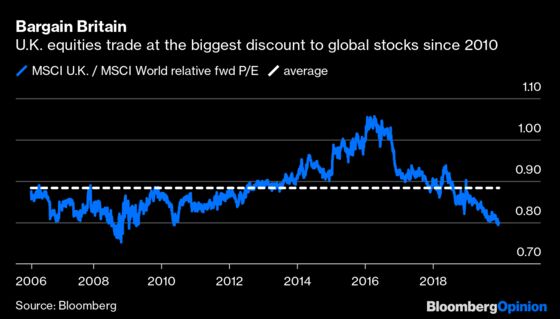

The biggest immediate beneficiaries are investors in U.K. equities, which have plenty of ground to catch up having lagged far behind European and U.S. indexes this year. British banks and house-builders have been particularly unloved (unless you’re a short-seller), explaining their bounce on Friday morning. And with the threat of Corbyn’s nationalization program gone, the utilities are suddenly happier places too.

As with the pound, though, it’s important not to get carried away about the FTSE 100 and the FTSE 250. The economy is a problem, and Johnson still has to conclude a painfully difficult trade deal with the European Union, Britain’s biggest trading partner. President Donald Trump’s resolution of the first phase of the U.S.-China trade deal was also a big factor in Friday morning’s share spike.

U.K. government bonds (known as Gilts) are suffering from the rapid shift back to equities and away from safe havens. Yet their rise on Friday is pretty much in line with German Bunds, showing again that much of this is to do with the U.S. trade breakthrough (if that’s indeed what it is). Expect gilt yields to head higher next year as more supply is certainly coming to finance a hefty fiscal splurge by Johnson; even if his plans pale by comparison to Corbyn’s slightly unhinged Labour manifesto.

With the Tories now counting on support from blue-collar voters in Labour’s former industrial heartlands, the days of austerity are over — with all of the implications that has for gilts.

The trickiest thing for the markets to call is what happens to short-term interest rates. Bank of England Governor Mark Carney is due to stand down at the end of January, at exactly the same as the U.K. will formally quit the EU. While his replacement will be announced soon, the central bank’s monetary policy committee will no doubt want to buy as much time as possible before tinkering with the 0.75% base rate.

The MPC will want to see exactly what is in the new government's first budget. With a big stimulus coming, they’ll probably do all that they can to avoid a rate cut in the meantime.

As I predicted in June, Johnson’s rise has been unmistakably good news for sterling assets, which should now benefit from renewed overseas demand and a slow return in domestic confidence as long as the Brexit trade talks don’t become another drawn-out disaster. Equally, the health of the global economy is just as important if a Boris and Brexit bounce is to be sustained.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.